Listen Now

0:00

Canada’s biggest banks are making a multi-layered bet on the AI and data-centre boom, with billions of dollars in holdings of U.S.-listed data-centre companies. Yet despite the sector’s rapid growth and global lenders’ increased use of risk-transfer structures to hedge their exposure, lawyers say the Big Six’s role in financing comparable projects at home remains largely opaque.

Talking Points

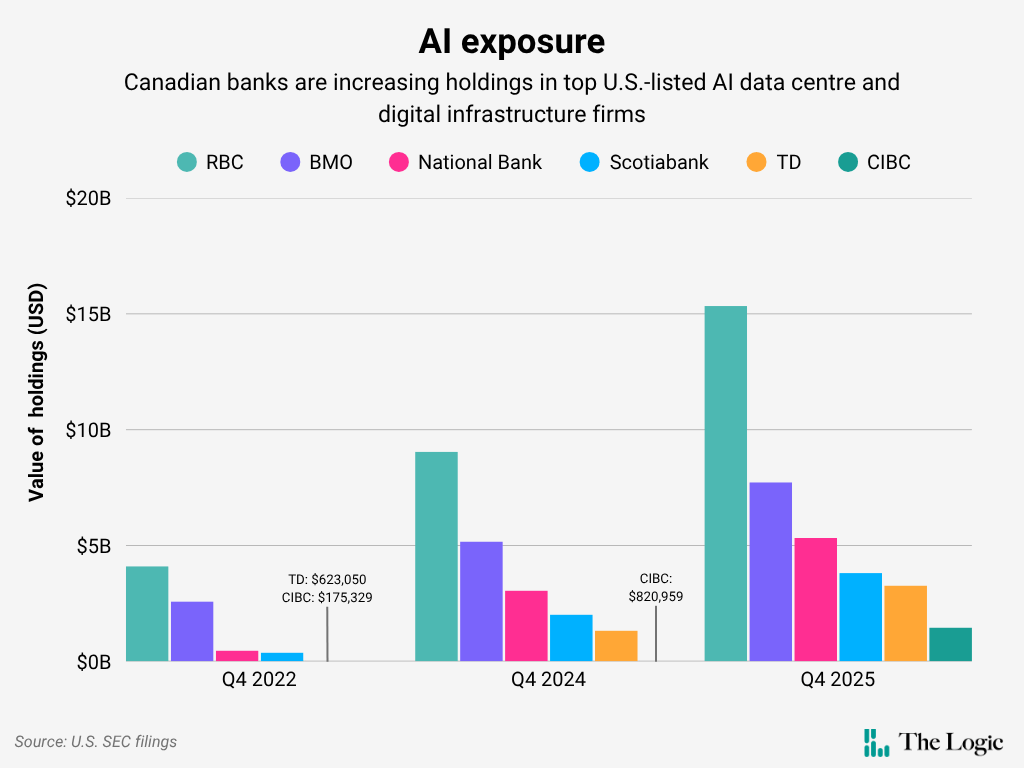

- Canada’s Big Six banks disclosed at least US$37 billion in holdings of U.S.-listed data-centre and digital infrastructure companies, up from US$7.5 billion at the end of 2022

- At the same time, some global banks are reportedly turning to private deals and risk-transfer structures to manage their exposure to the AI boom

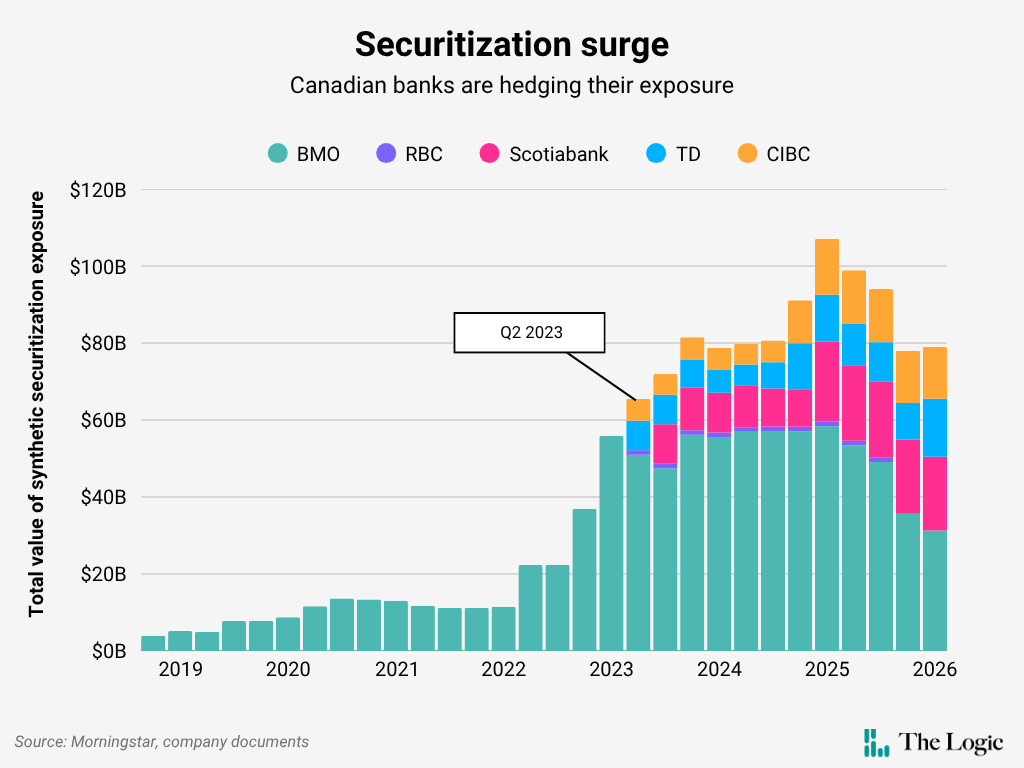

- Meanwhile, Canadian banks’ use of synthetic securitizations as a whole surged to nearly $79 billion in the first quarter from $11.4 billion in early 2022

The Big Six have disclosed at least US$37 billion in holdings of U.S.-listed data-centre and digital infrastructure firms across investment portfolios they managed at the end of last year’s fourth quarter, an analysis by The Logic shows. That’s five times more than the US$7.5 billion they held at the end of December 2022—coinciding with the quarter after ChatGPT’s rise accelerated the current wave of AI investment. The Logic analyzed the banks’ holdings in 15 of the top U.S.-listed companies in the AI data-centre and digital infrastructure sector, including CoreWeave, Digital Realty, Intel, Broadcom and Lam Research, among others.

RBC held the largest position, holding more than 76 million shares in the group of companies worth over US$15.3 billion, as of Dec. 31, the latest quarter for which data is available. Bank of Montreal followed with over 42 million shares in the group of companies The Logic reviewed, worth nearly US$8 billion. Meanwhile, CIBC’s holdings in the firms increased more than any of its peers since the fourth quarter of 2022, growing from mere US$175,000 to almost US$1.4 billion.

RBC’s head of AI, Bruce Ross, previously told The Logic that while the bank has the largest graphics processing unit (GPU) farm outside of the federal government, it’s keeping its options open when it comes to using more sovereign AI infrastructure. The bank’s holdings in the firms reviewed by The Logic rose 69 per cent year-on-year in the fourth quarter of 2025.

Shalabh Garg, an analyst at Veritas Investment Research, said these positions could reflect securities owned through the bank’s asset management business on behalf of clients—rather than direct investments made with the banks’ excess capital. Any direct exposure, he said, remains relatively small compared to their overall balance sheets and does not materially alter their risk profiles.

Related Articles

TD declined to comment on the holdings, while National Bank spokesperson Alexandre Guay said the holdings are not direct investments made by the lender, but rather “client positions or part of investment funds” managed through its investment arm. BMO, RBC, CIBC and Scotiabank did not respond to requests to comment.

The Big Six have been very vocal about their AI ambitions in recent years, but only through developing internal models and setting targets for how the technology will enhance core business segments. Yet they have said little publicly about their role in financing data-centre infrastructure in Canada, despite involvement in projects including QScale, Cologix and eStruxture.

BMO has been one of the few exceptions. During the bank’s investor day in March, capital markets head Alan Tannenbaum said the bank is financing and providing risk management solutions for the buildout of data centres, networks and power demand.

Beneath the surface, Canadian bank lending to data centres and AI-adjacent infrastructure has grown meaningfully over the past 18 months, said Stephen Johnston, a director at Omnigence Asset Management. Even so, “it remains a relatively small share of total assets at the individual institution level,” he added in an email. The loans are also generally illiquid, with only a small secondary market of institutional buyers, while most—especially construction and mid-tier operator loans—are typically held to maturity, he said.

While the U.S. remains the dominant data-centre market globally, Canada already hosts more than 300 facilities, clustered in major hubs such as Alberta, Ontario and Quebec. Ottawa has sought to accelerate the buildout, pledging $15 billion in 2024 with the expectation that private capital would finance the remainder. Institutional investors, including the Maple 8 pension funds, have also deployed billions of dollars into data-centre projects both domestically and abroad.

Jason Kroft, partner and head of structured finance and securitization group at Gowling WLG, said lending in the data-centre space remains largely “opaque,” noting that most deals are kept private unless the borrower is publicly listed. He identifies three main financing approaches to AI infrastructure in his research: project finance for new builds backed by long-term leases and cash flows; real estate finance for stabilized, multi-tenant facilities underwritten against asset value and performance; and securitization, where assets or leases are packaged into structured securities sold to investors rather than concentrated on banks’ balance sheets.

“All of the Canadian banks are active in construction or project financing. What are still early days is… that kind of capital market solutions involving issuing debt or intermediating debt to a range of participants,” Kroft said.

Kirk Emery, a partner at law firm Miller Thomson, said lenders generally consider a data-centre project bankable if it has an investment-grade tenant, a long-term lease, secured power supply and clear land rights. But because Canada trails the U.S. in its data-centre buildout, he said, banks are less familiar with how to underwrite such projects, often leading data-centre deals to be “kicked around” among real estate, project finance and other teams as lenders determine how to structure and assess them.

“Originators are pooling data-centre loans and selling tranches to asset managers and pension funds, which spreads risk but also makes it harder to trace where concentrations are actually building.”

What has changed recently is the emergence of a “second tier” of smaller AI infrastructure borrowers that lack the same credit quality, Johnston said, with financing increasingly relying on inherently speculative assumptions about future AI demand.

“The distribution chain is lengthening,” Johnston said. “Originators are pooling data-centre loans and selling tranches to asset managers and pension funds, which spreads risk but also makes it harder to trace where concentrations are actually building.”

That trend is also creating more opportunities for private credit firms, which are moving into areas where banks are more cautious, Johnston added.

Kroft’s research found that private credit funds are offering financing at 7 to 10 per cent—sometimes offering more flexible terms than the 5 to 7 per cent yields of securitized debt.

AI data centre and project financing deals reportedly surged to US$125 billion so far last year, up from US$15 billion over the same period in 2024, according to a November report from UBS, which expects increased issuance from the sector to play a pivotal role in credit markets this year. According to Morgan Stanley estimates in August, the sector faces a US$1.5 trillion global financing gap over the next three years.

Demand for data centres in Canada is expected to outstrip available domestic capital, Kroft said, with the sector requiring a mix of financing sources—including banks, private equity, private credit, government support and capital markets solutions—to close the gap.

As lending to the sector grows, banks globally are also increasingly exploring new ways to offload risk, including through significant risk transfer (SRT) transactions. These financial tools, which typically last three to five years, let banks transfer a loan portfolio’s credit risk to non-bank financial institutions (NBFIs), typically private credit funds or hedge funds. In turn, banks can reduce regulatory capital requirements, free up capacity for new lending and diversify risk without selling the underlying loans.

Initially popular in Europe, the SRT market has since expanded rapidly to other countries, including Canada. As of the first quarter of this year, the Big Five banks used synthetic securitizations to transfer or hedge risk on nearly $79 billion in wholesale loans, up from $65 billion in early 2023, according to a Morningstar analysis and company filings.

Josh Veenkamp, a Morningstar DBRS analyst and assistant vice-president of credit ratings, wrote in a research note that all SRTs completed in Canada through 2024 had been tied to commercial, rather than retail, loan portfolios. BMO has been using SRTs since 2018—reflecting its larger commercial loan book—while its peers began adopting the structures around the second quarter of 2023. National Bank has no SRT exposure at this time, according to Guay.

TD is reportedly exploring a plan to transfer $1 billion in data-centre loans, Bloomberg reported last month. Garg said Canadian banks tend to operate in loan syndicates, meaning that when one lender moves into a new area, others typically follow—some taking lead roles, while the rest participate in smaller positions.

For Johnston, the TD deal is notable because it suggests a Canadian bank sees enough concentration risk in its data centre exposure to warrant hedging. That raises questions about whether banks are truly offloading credit risk to improve their balance sheets, or simply redistributing it—only to pick up similar exposure again through investments in the same NBFIs. He added that if the broader thesis around AI profitability proves wrong, losses could hit multiple investors at the same time.

“If multiple banks are building data-centre books and multiple banks begin using SRTs to manage that exposure, the mezzanine risk [the danger of not being repaid by being second in line] is inevitably going to be held by a relatively small pool of specialist credit investors,” Johnston said.

In September, the Office of the Superintendent of Financial Institutions outlined the conditions for banks to obtain capital relief on SRTs, which depend on meeting its risk transfer requirements. It later added new requirements to the draft rules for next year, including notifying the regulator of all SRTs within 30 days. The final guidelines will be published in September and are expected to come into effect in late 2026 or early 2027.

Asked whether the regulator had concerns about the growing use of synthetic securitizations or broader risks emerging in the market, OSFI spokesperson Cory Harding said in an emailed statement that the regulator is monitoring the activity, including significant risk transfer transactions. He added that institutions could be required to reverse associated capital benefits if a transaction fails to meet securitization rules.

“None of this means the current situation is a crisis. Data centres are real assets serving real demand,” Johnston said. “But the speed of capital deployment, the lengthening of the distribution chain and the migration of credit risk to less-regulated participants are patterns that warrant serious attention.”