Listen Now

0:00

Canada’s major financial institutions are defending their private credit exposure, as sentiment sours around U.S. firms like Blue Owl amid intensified scrutiny from regulators and skeptics.

Canadian pension funds and life insurers, by one estimate, hold over $180 billion in private credit—an industry that offers loans to small businesses, bypassing banks and public markets. It’s showing no signs of slowing down. Yet retail investors are pulling money out of U.S. private credit funds like Blue Owl, Carlyle and KKR, as competition from AI companies hammers the valuations of software companies, which are heavy users of private credit.

Talking Points

- Canada is a small part of the overall private credit market, and Canadian financial institutions say they’re making safe bets on the industry

- Still, skeptics are watching the growing private credit exposure in Canada as U.S. investors start to pull money from the market

Canada’s exposure is small compared to the US$3 trillion global market, so the current market turmoil isn’t existential, but it’s also not a “non-event,” said Stephen Johnston, director at Omnigence Asset Management.

Johnston said pensions and insurers are being “unreasonably optimistic” in assuming their private credit investments are not sitting on losses, adding that stress might first show up in “bigger write-offs” and potentially “material” losses.

“If discounts on book values keep going up,” said Johnston, “it’s saying something very fundamental about the state of the U.S. economy, and that will have consequences for the United States [and] for Canada.”

Related Articles

However, he noted that Canada’s private lending is focused on multi-tenant real estate rather than struggling software companies. Canadian private credit managers oversee between $20 to $30 billion, compared with the U.S. market of US$1.5 trillion, CIBC estimated in November.

The Canadian market remains concentrated among institutional players, making it difficult for alternative lenders to “break in,” Johnston said. Canadian investors, he added, have also generally been more conservative than their U.S. counterparts when it comes to riskier forms of lending.

Canadian regulators are alert to the underlying troubles in the sector. In its annual risk report released last week, the Office of the Superintendent of Financial Institutions named exposure to private credit and other non-bank financial firms as one of the top risks to the Canadian financial system, though superintendent Peter Routledge has previously expressed confidence in its resilience. “A risk can be material and growing without being system‑threatening,” spokesperson Cory Harding said in an email.

Bank of Canada governor Tiff Macklem, meanwhile, said in March that “the issue is not private credit itself. It’s how private credit will behave under stress.”

Global spillover from a U.S. crisis is likely limited, but investors exposed to U.S. financial instruments—like private-equity owned insurance companies or U.S. high-yield and small-cap funds—may see pockets of stress, said Tianchen Peng, global macro strategist at Oxford Economics.

“We think there’s indeed a bubble in the private credit market,” said Peng. “It is just too much money chasing a too-limited opportunity set.”

“A risk can be material and growing without being system‑threatening.”

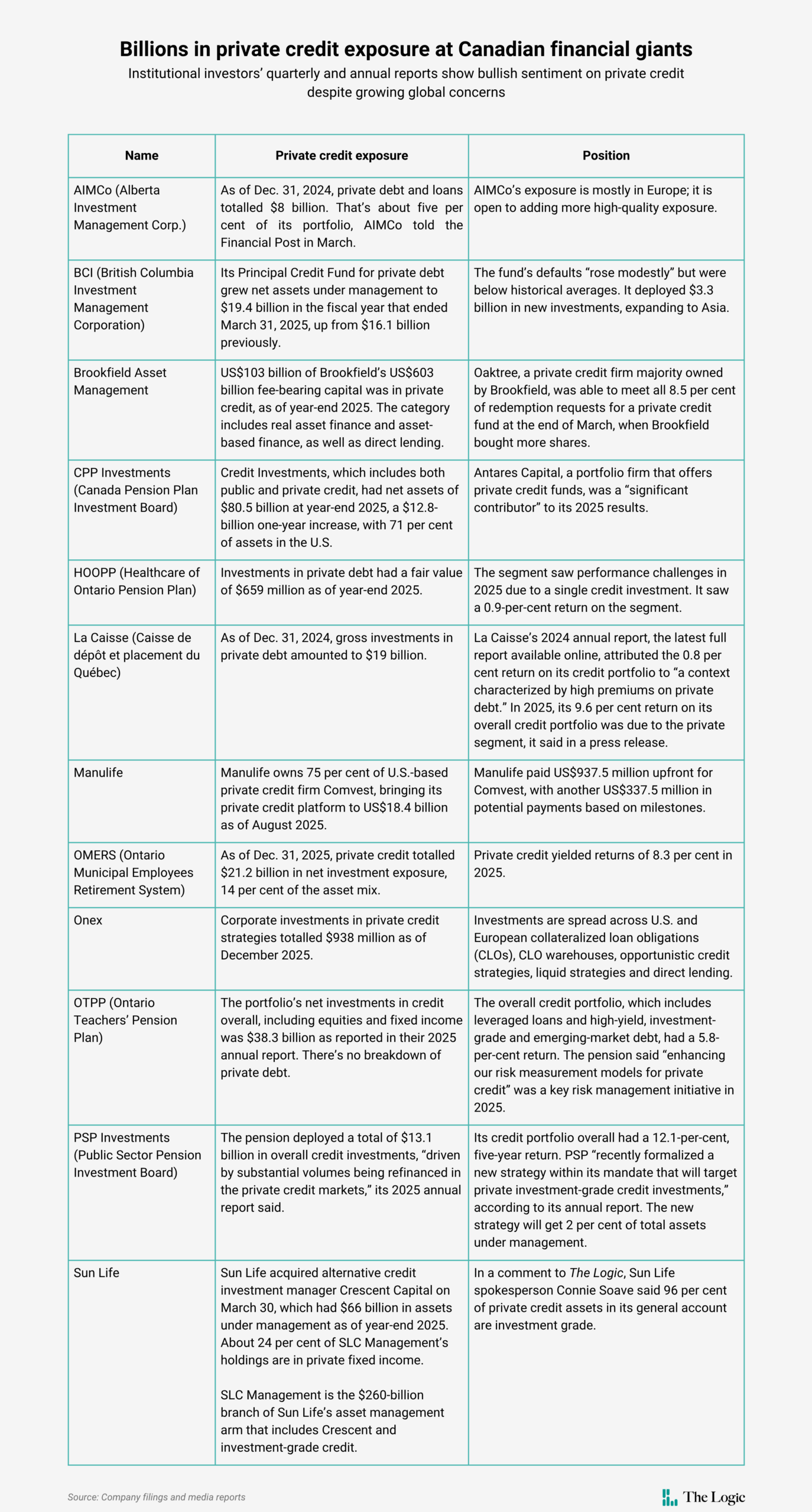

Canada’s major “Maple 8” pension funds held over $100 billion in private credit, the Global Risk Institute found last year. Canada Pension Plan Investment Board accounted for the largest share, with roughly $43 billion allocated, and plans to expand its credit portfolio to more than $115 billion by 2029. Meanwhile, Manulife and Sun Life each held over $40 billion. Canadian heavyweights like Brookfield, Manulife and AIMCo have since leaned further into the high-growth sector, which is often touted as a way to diversify from the volatility in bond and stock markets.

Canada didn’t experience the same private credit boom that followed tighter U.S. bank regulations after the 2008 financial crisis. Still, “the [private credit] alarm bells were going off in Canada before the U.S.,” said Liam O’Sullivan, principal and co-head of client and product solutions at asset management firm RPIA. He pointed to Bridging Finance’s collapse in 2021, redemption requests at Romspen in 2022 and, more recently, Toronto-based Cortland pausing redemptions due to an “overweight single-name concentration.”

Peng said the private credit industry is under pressure as those borrowers benefit less from U.S. economic growth, which is experiencing a K-shaped trend. There are signs of “shadow defaults,” where unpaid interest is rolled into principal, he said.

When asked about their approach to private credit and plans to diversify, spokespeople for seven of the Maple 8 declined to comment. La Caisse did not respond to a request for comment, though its head of liquid markets has previously said market anxiety around the asset class is “exaggerated.”

OMERS and BCI were reportedly among the buyers of a US$1.4 billion portfolio of Blue Owl loans in late February. O’Sullivan said the transaction “raised eyebrows,” as investors paid 99.7 cents on the dollar despite markdowns in private credit assets across the U.S. market, suggesting either strong confidence in the loans’ valuation, or considerations like preserving a relationship with the firm.

Still, Peng said, there’s a logic to patient capital like pension funds buying up long-term investments, adding that there’s data supporting a clear divergence between the sector’s winners and losers.

Canadian companies say they are poised to be winners. Colin Simpson, chief financial officer of Manulife, has defended its acquisition of private credit firm Comvest, saying the “rush for the door” in private credit poses “no real risk” given its lack of exposure to retail investors and sub- investment-grade loans.

Asset manager Onex does not see private credit as a systemic risk, TD Cowen analyst Graham Ryding wrote in a note, though management acknowledges the potential for “write-downs and underwhelming returns.” Brookfield Asset Management CEO Connor Teskey reassured analysts in a February earnings call that it saw only modest redemptions amid a “disciplined approach” to managing volatility.

Even so, sentiment is shifting. Morningstar recently cut Brookfield Asset Management’s fair value price estimate, with analyst Greggory Warren writing that “the negative perceptions” of rivals like Blue Owl could infect Brookfield, leading to increased redemptions and making fundraising more difficult. Brookfield represented about 13 per cent of the industry’s private credit fundraising efforts between 2020 and 2025, Warren estimated.

Manulife and Brookfield declined to comment on the record. Onex did not respond to a request for comment, nor did any of the spokespeople for Scotiabank, National Bank, BMO and TD. RBC didn’t respond to specific questions about their exposure. CIBC spokesperson Tom Wallis referred back to the Canadian Bankers Association’s previous statement that banks will continue to make “prudent decisions” with their clients, including non-bank financial institutions (NBFIs).

While Canadian banks have upped lending to NBFIs, analyst notes suggest they are assuring investors that much of their focus is on collateralized loan obligations (CLOs), which can create indirect exposure to the same borrowers financed by private credit funds. National Bank said it has no CLO exposure, while Scotiabank disclosed that CLOs account for about one per cent of total bank-level loans, TD Cowen analyst Mario Mendonca wrote in a note to clients. On average, private credit accounts for about 5 per cent of Canadian banks’ total consolidated loans as of the end of last year, according to RBC Capital Markets’ analyst Darko Mihelic.

Bank of Montreal chief risk officer Piyush Agrawal previously said some of the concerns around the asset class may be “overdone.” CIBC’s CEO Harry Culham recently told shareholders that the lender has stress-tested its private credit portfolio.

The U.S. private credit frenzy could prompt Canadian regulators and dealers to tighten risk ratings and reduce private debt offerings, O’Sullivan warned, potentially reducing the supply of credit to Canadian companies and weighing on economic growth.

Johnston said limited partners in Canada and abroad are likely to become more selective in evergreen alternative funds, as U.S. turmoil has exposed a mismatch between long-term assets and the promise of quick redemptions.

While he doesn’t see a clear channel for negative sentiment in private credit to spill over into Canada’s public equity markets, lending markets or the broader economy, Johnston said the impact is likely to show up in performance.

“After they properly provision for all these losses,” he said, “historic returns are going to not look very good.”