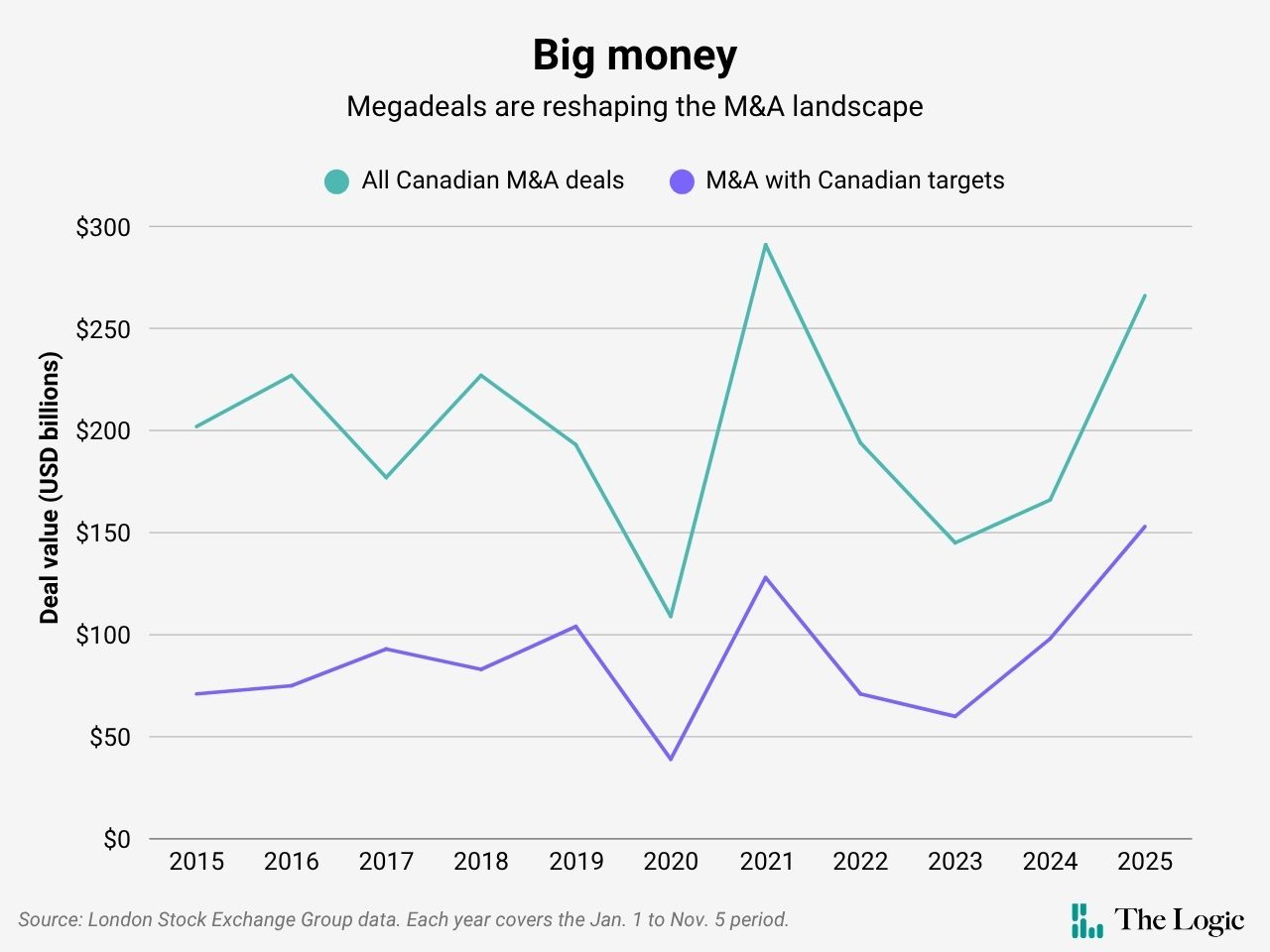

M&A activity in Canada is bouncing back after a sluggish start to the year. Mergers and acquisitions rose about 60 per cent to US$266 billion in the first 10 months compared to the same period last year, driven by a wave of large transactions and renewed investor confidence.

Skip to content

News

Canadian M&A surges as megadeals provide cover for volume decline

Deal value is up 60 per cent so far as deal makers take advantage of falling interest rates, even as number of transactions slip

Toronto’s financial district photographed during the day. Photo: Cole Burston/Getty Images

M&A activity in Canada is bouncing back after a sluggish start to the year. Mergers and acquisitions rose about 60 per cent to US$266 billion in the first 10 months compared to the same period last year, driven by a wave of large transactions and renewed investor confidence.

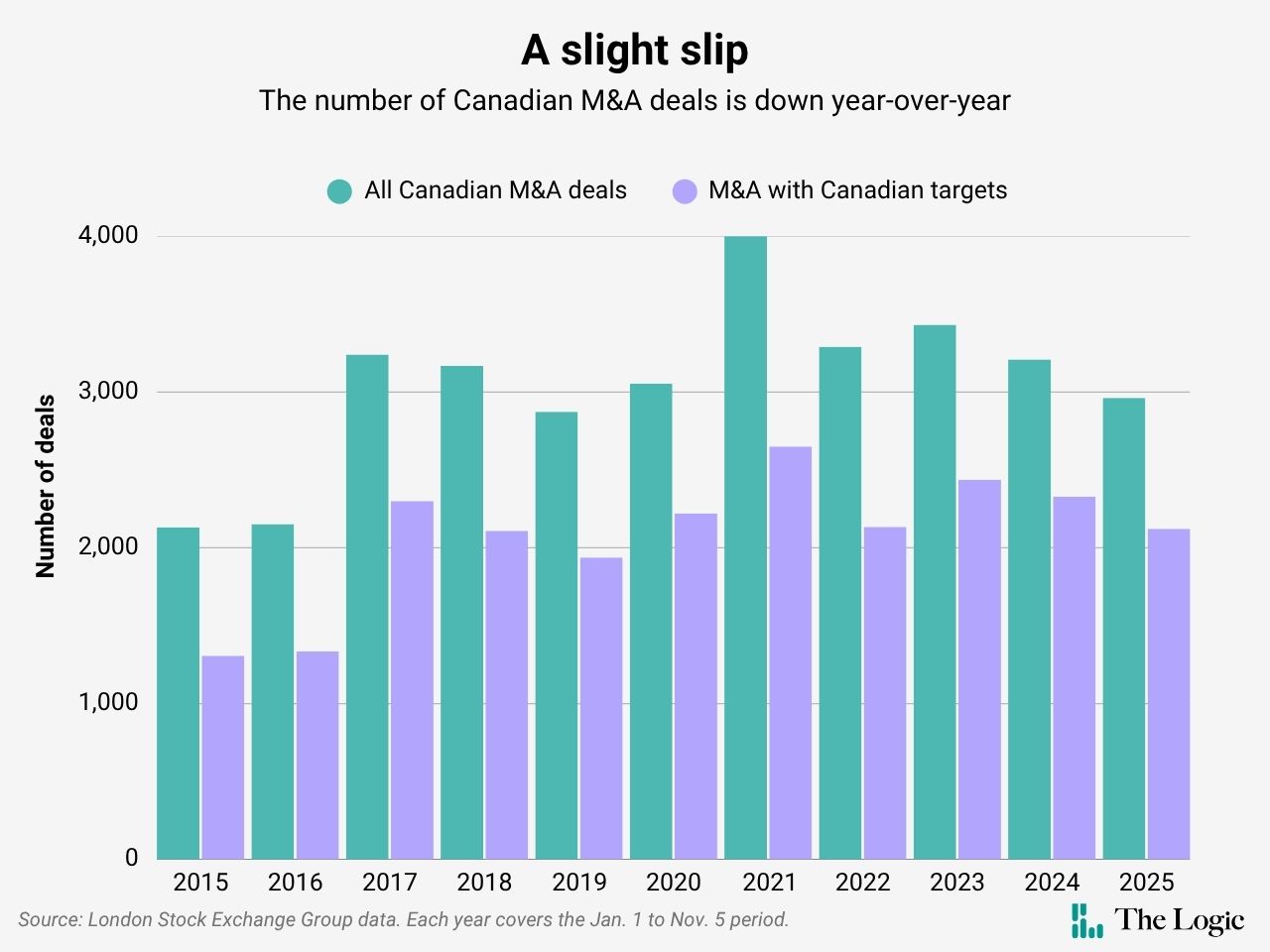

At the same time, overall deal volume dropped 7.7 per cent with only 2,962 deals recorded compared to last year’s 3,209, according to data from the London Stock Exchange Group (LSEG). The third quarter saw US$52 billion in announced deals, making it the strongest quarter since the market’s peak in early 2021.

The record-setting surge of cross-border deal making in the first half of 2021 was largely fuelled by U.S. buyers snapping up Canadian firms. That momentum, however, was followed by a multi-year slowdown. This January was the weakest for U.S. acquisitions of Canadian companies in 22 years, as deal makers held back to see how U.S. President Donald Trump’s economic threats would play out.

Talking Points

- While the total value of Canadian M&A deals is up 60 per cent in the year to Nov. 5, the number of transactions has dipped by 7.7 per cent, as deal makers take advantage of lower interest rates, strong corporate earnings and the rise of private credit

- Foreign interest in Canadian assets has picked up, with the four largest deals this year coming from acquirers in the U.K., Austria, and the U.S.

With some tariff anxiety now easing, deal activity is picking back up. Marco Tomassetti, managing director of corporate finance at KPMG in Vancouver, said that this year’s rebound can be explained by a combination of falling interest rates, which are lowering the cost of capital, and inflation being under control—conditions that have driven strong sector performance.

“Even though there’s still some tariff uncertainty, people have kind of gotten around that,” Tomasseti said in an interview. He noted that while the Canadian IPO market remains slow, private lending has expanded in recent years, providing an alternative source of capital for deals.

Much of the M&A rebound has been shaped by a few megadeals, with foreign acquirers targeting Canadian companies. The top three drivers of this year’s surge include Anglo American’s proposed megamerger with Teck, Borouge Group International’s proposed acquisition of Nova Chemicals, and Sunoco’s takeover of Parkland, per LSEG data. Total deal value involving Canadian targets has risen almost 56 per cent to US$153 billion so far this year.

Jason Saltzman, a partner at Dentons Canada, said several recent auctions he has advised on have mainly attracted international bidders. “The weak Canadian dollar always makes things interesting for non-Canadians, because it just makes things a little bit cheaper,” he said.

Related Articles

However, the rise in foreign appetite comes amid intensifying regulatory scrutiny around mergers. Changes to the Competition Act and the Investment Canada Act have led to increased oversight of transactions in energy, infrastructure and other strategic sectors, said Saltzman. But blocking deals outright isn’t generally in Canada’s best interest, according to Amar Pandya, portfolio manager at PenderFund.

“I believe in fair and open markets,” Pandya said. “If you have willing sellers willing to transact and sell their business to an acquirer that’s willing to pay a premium, that’s generally speaking, a good thing.”

Daniel Nowlan, a managing director at National Bank, said the deals he’s seeing are more strategic. He noted a split in the market, with larger, more liquid companies trading at much higher multiples than small-cap firms. For smaller public companies, he said, it’s becoming increasingly difficult to attract investor attention and sustain valuations.

“The smaller companies have been trading for a while at lower multiples,” Nowlan said, adding that their institutional shareholder bases have thinned. “There’s been a recognition that the corner might not turn too quickly.”

According to LSEG data, the energy and materials sectors continue to dominate Canadian deal making this year. Energy and power has driven about US$86 billion in deals so far in 2025, almost double its level over the same period last year, and representing 32 per cent of all M&A value.

Tomassetti said renewed momentum in data centres and power generation are also fuelling M&A activity. He added that the valuation gap that had previously stalled pricing negotiations has also narrowed, making it easier for buyers and sellers to find common ground.

Smaller deals continued to dominate the M&A market so far in 2025. LSEG data shows that transactions under US$500 million made up more than 96 per cent of all deals. Meanwhile, deals above US$1 billion accounted for only 2 per cent of total deal transactions but contributed a striking 76 per cent of total deal value—the most large deals have contributed to total value in a decade.

Goldman Sachs was the top financial adviser, followed by RBC Capital Markets, and BMO Capital Markets, according to LSEG data.

Deal makers interviewed by The Logic were optimistic about next year’s M&A outlook, with Tomassetti viewing both tariffs and pandemic-era shocks as temporary “blips.” “I think the fundamental structure of the market is very strong and there’s lots of capital in the private equity asset class that is looking to make investments,” he said.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: Cole Burston/Getty Images

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Subscriber Survey

Most of you think AI will change your job, but not replace you

Briefing

TC Energy says North American natural gas demand is growing much faster than previously expected

Mississauga imposes data centre pause, as Toronto councillors scrutinize local projects

A third of Canadian workers are using generative AI, but not for everything

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.