Listen Now

0:00

Last month, I asked Minto Group chief executive Michael Waters what he found himself thinking about the most as the head of one of Canada’s bigger real estate companies. He needed several minutes to download all that was on his mind.

“I don’t think anyone would have built the Iran war into their business plan for 2026,” Waters began. Surging oil prices were blowing up Minto’s budget for anything made of plastic, asphalt or even shingles.

There was the threat of demand destruction. When living costs rise, disposable income shrinks in the short term. At the beginning of the year, it was reasonable to contemplate interest rate cuts. Not now. The spectre of cost-push inflation was causing long-term interest rates to rise, pulling mortgage rates along with them.

Related Articles

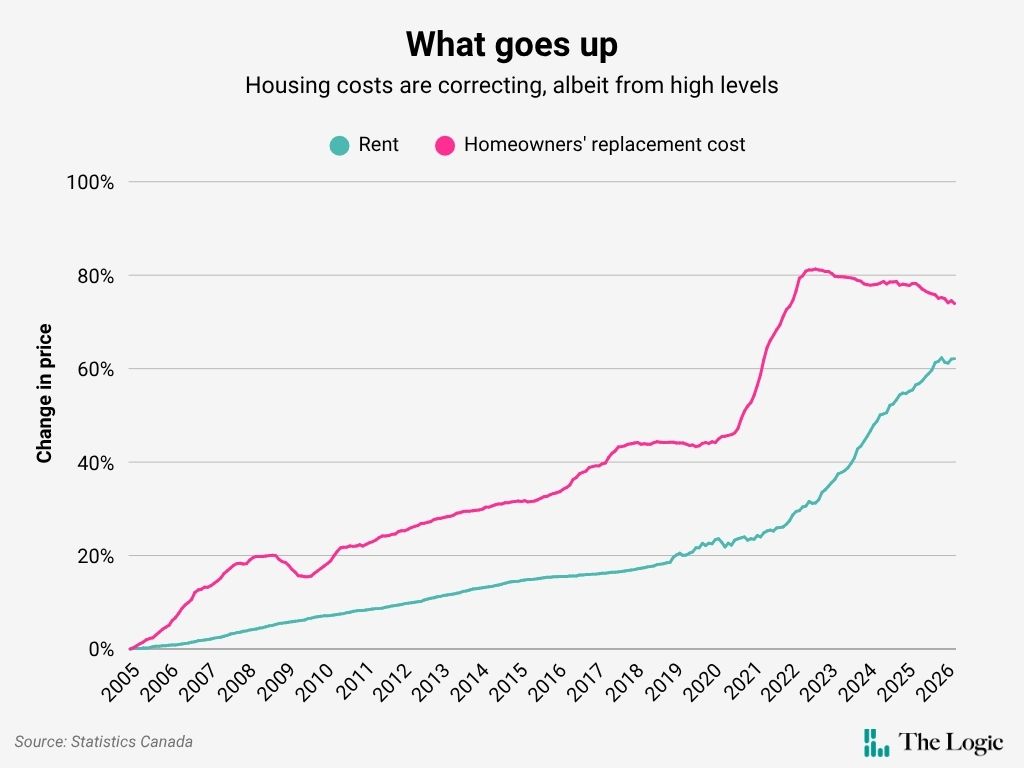

The future of the North American trade agreement was up in the air. That was weighing on consumer confidence. The Canadian population had declined for two quarters in a row. That’s bad for the rental market because immigrants tend to lease before they buy. Average asking rents had fallen for 18 months in a row, “a fairly significant run and we’re seeing a housing market that is quite soft,” Waters said.

It’s helpful to see things through the eyes of a developer because the real estate industry has become such an important player in Canada, economically and politically. The Bank of Canada foresees little help from housing in getting the country’s economy going again. Prime Minister Mark Carney promised to boost housing supply, but he can’t build the homes himself. That means companies such as Minto will have something to say about his political success.

Some industries are in real trouble because of what’s going on in the world. Trouble for the real estate sector was a profit margin of about 25 per cent last year, down from an average since 2010 of about 28 per cent, according to Statistics Canada data. But none of us likes to go in reverse, and fat profit margins have become the industry’s norm. The pace of new construction will be constrained until builders like the math—and the math currently is messy.

“The housing markets, actually, I would say are balanced, but as a sector we’re struggling a little bit,” Waters said. “That’s going to have an impact on the broader economy if we have job losses, etc.”

The news wasn’t all bad back in mid-April. The federal and Ontario governments had recently cut or reduced the HST on new homes. “Dramatic,” said Waters. “In one day, in Ottawa, we saw 50 sales, which would have been essentially a month of sales activity in that market for our business, compared to the prior two months.”

We talk about the housing crisis like it’s still 2021. That’s when low interest rates, work-from-anywhere internal migration and a spectacular increase in immigration caused home prices and rents to spike. A more adaptable housing market might have been able to absorb some of that shock. In Canada, supply barely moved. The market had become so distorted by subsidies, regulation and profit expectations that it no longer sent clear signals.

But it’s not 2021. Statistics Canada’s proxy for home prices plateaued in 2022 and has been drifting lower. The correction in rents is more recent, but it’s coming. As The Logic reported earlier this month, rental vacancy rates have accelerated across the country, so much so that some developers have begun to talk about a glut of rental properties in the near future. The optimal response to housing affordability at this stage might be patience.

Patience isn’t really a thing anymore, though, is it? Voters say they can’t afford shelter. Developers say they can’t provide more shelter because the market is frozen. So Carney and Ontario Premier Doug Ford did what Canadian politicians have been doing for decades and served up some new demand-side sops.

There’s been some good research lately that explains why a Dr. Feelgood approach to housing policy doesn’t improve affordability. Mathieu Laberge, chief economist at Canada Mortgage and Housing Corporation, published findings that show tax breaks and the like only lower prices if builders are similarly incentivized to increase supply.

That balance is way out of whack. The Canadian Tax Observatory and the Centre for the Study of Living Standards tallied federal tax breaks for housing and determined the government forgoes about $17 billion in revenue a year. Their paper took a hard look at the First Home Savings Account, a tax-sheltered vehicle for down payments, and concluded that the program mostly benefits wealthier and older households. The analysis also found a link between account withdrawals and higher home prices.

The federal government committed its original sin in 1972, when it introduced capital gains taxes but excluded principal residences from the levy. Policymakers wouldn’t have foreseen an item on Maslow’s hierarchy of needs becoming a speculative asset. During our interview, I stopped short when Waters said he suspected the next cycle of construction would be “end-user oriented.” It was an admission that the previous cycle wasn’t oriented toward building places where people might live the “dream of home ownership,” which lobby groups such as the Ontario Home Builders’ Association talk so much about.

For the better part of two decades, government policy was geared to stoke demand, as lower interest rates and higher immigration targets amplified tax incentives that favoured real estate. But instead of creating a generation of homeowners, that policy mix generated a class of investors who saw a portfolio of 600-square-foot condo units in Toronto as a better bet than the stock market. “Developers respond to economic stimuli,” Waters said. “Some of the buildings were 80-90 per cent investor.”

Now that the mania has passed, you can see market forces reasserting themselves. The overbuilding won’t be wasted. The glut in Toronto will continue to put downward pressure on rents. Waters said Minto is considering turning some of its excess supply into seniors housing, which would be a happy outcome of all of this. A market with lots of supply and lots of demand will find an equilibrium, if we let it.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.