The meme-ification of the economy continues. The epic downturn caused by the COVID crisis wasn’t a recession, it was a “she-cession.” The disconnect between record low unemployment rates and the sour mood about the economy became the “vibecession.” Now, thanks to Alberta Central chief economist Charles St-Arnaud, we have a meme to explain why the bad vibes likely will persist.

Skip to content

Commentary

Carmichael: Forget the vibecession. Canada, welcome to the me-cession

As a collective we’re spending more, but as individuals we’re acting like we’re in a recession

A shopper in a No Frills grocery store in Toronto, in May 2024. Alberta Central chief economist Charles St-Arnaud says Canada is still in a “me-cession,” where collective spending is up but individuals are restricting their own purchases. Photo: The Canadian Press/Chris Young

The meme-ification of the economy continues. The epic downturn caused by the COVID crisis wasn’t a recession, it was a “she-cession.” The disconnect between record low unemployment rates and the sour mood about the economy became the “vibecession.” Now, thanks to Alberta Central chief economist Charles St-Arnaud, we have a meme to explain why the bad vibes likely will persist.

Canada has fallen into a “me-cession.”

St-Arnaud introduced the term last week in his mid-year economic outlook. He thinks Bank of Canada governor Tiff Macklem will successfully guide the economy to a soft landing, aided by a couple more interest-rate cuts before the end of the year.

But St-Arnaud doubts that Macklem’s achievement will result in a robust recovery. He predicts inflation-adjusted gross domestic product will increase 1.2 per cent this year, 1.1 per cent next year and two per cent in 2025. That pace is about half as fast as the Bank of Canada reckons the economy can grow before demand starts stoking inflation.

The lift is coming almost entirely from immigration, which continues to enlarge the pie, although not enough to ensure everyone gets a healthy serving. “Collectively, we are spending more and pushing economic activity higher, but individually, we are restricting purchases and behaving as if we are in a recession,” St-Arnaud wrote.

Related Articles

A good meme can help focus the mind. Defining the COVID crisis as a she-cession made it easier to grasp why traditional stimulus measures such as infrastructure spending would do little to reverse the effects of locking down services—and requiring mothers to work from home with children underfoot. The federal government focused on supporting households and extending lifelines to smaller employers, and the she-cession narrative cleared a path for Finance Minister Chrystia Freeland to introduce a national child-care program in the pandemic’s wake.

Maybe St-Arnaud’s meme, with its focus on spending at the individual level, will help policymakers and the public make sense of what’s happening in the economy, as the vibecession is starting to look shallow.

Recent evidence suggests the bad vibes were warranted, not just a hangover from surging inflation in 2021 and 2022. Statistics Canada reported last month that the share of income of the middle three quintiles of Statistics Canada’s income distribution—60 per cent of the total, so a significant majority of all households—actually declined in the first quarter, as interest payments grew faster than wage gains.

I was open to vibes as an explanation for the disconnect between strong macro numbers and weak sentiment data. Some of that openness was philosophical. The pandemic was a seismic event, and given the fallout from similar events (the influenza pandemic that spread around the world during the First World War, the Great Depression, the Great Recession), I think we’ve come out of COVID fairly well.

As all the polls suggest, mine was a minority view. Many households are materially worse off than before the pandemic, something the aggregate data obscured because those numbers were affected by the outsized increase in the population.

St-Arnaud estimates that individual consumers are spending about four per cent less per person on an inflation-adjusted basis than before the pandemic; however, because of all the new spenders, aggregate consumption is about six per cent higher. If not for the surge in population growth, St-Arnaud’s calculations suggest the economy would have contracted over the second half of 2023.

It took some time to begin to absorb how all those newcomers were affecting the economy. At first, they were helping fill a record number of job vacancies, replenishing a labour pool destined to shrink as boomers age out of the workforce. But it eventually became clear that we couldn’t easily accommodate so many new residents at once. Bank of Canada deputy governor Toni Gravelle showed in a December speech that “demographic demand” for housing has shot to the moon since 2022, while rates of new construction have barely changed.

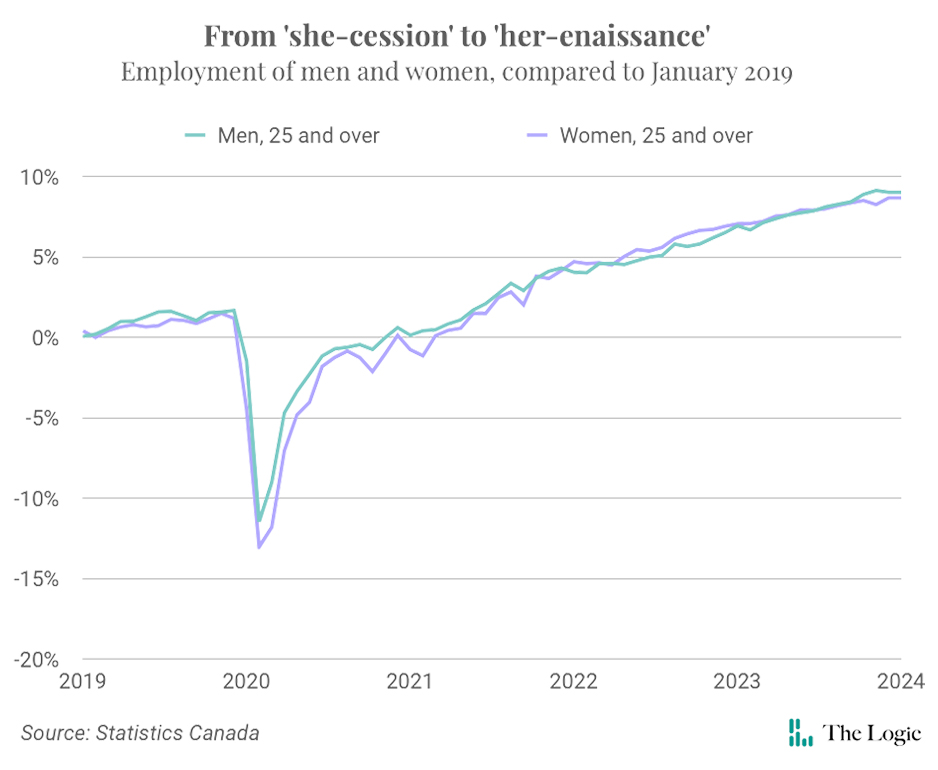

The she-cession turned out well—for a time, women were being hired at a faster rate than men, and employment for both groups is now about nine per cent higher than at the start of 2019. A me-cession could be more difficult to solve, if only because governments maxed out their credit cards during the pandemic.

Lower interest rates will help. The Bank of Canada has cut the benchmark rate at its last two meetings and Macklem indicated more cuts will be coming before the end of the year.

The other key is the labour market. So far, employers have responded to higher interest rates by taking down job postings rather than firing people. But vacancy rates are now below historic lows, and the jobless rate climbed to 6.4 per cent in June, the highest in more than two years. St-Arnaud estimates the jobless rate could drift to almost seven per cent by the end of the year, because the labour pool will continue to grow while hiring flatlines. The youth unemployment rate surged in June, a telltale sign of underlying weakness.

Prime Minister Justin Trudeau’s government opted to use its remaining fiscal room on a multibillion-dollar housing plan—it even raised capital gains taxes to allow for extra spending without blowing its deficit targets. All that money should get some projects moving, since the cash comes with strings attached, but it might not do much for the economy because the industry is already at its capacity to build, as housing starts are above trend.

That means employers will dictate the trajectory of the me-cession. It could be touch and go. The Bank of Canada’s latest business outlook survey was notably grim. It makes you wonder if by misreading the post-COVID vibes, Trudeau went after the wrong target.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Chris Young

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Subscriber Survey

Most of you think AI will change your job, but not replace you

Briefing

TC Energy says North American natural gas demand is growing much faster than previously expected

Mississauga imposes data centre pause, as Toronto councillors scrutinize local projects

A third of Canadian workers are using generative AI, but not for everything

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.