Statistics Canada published a reminder this week that embarrassingly weak business investment is at the root of the productivity crisis.

One observation from the report: investment per worker in 2022 was roughly 20 per cent lower than 2014 levels. Little has changed since then. Inflation-adjusted spending on non-residential investment in early 2024 was 25 per cent below peak levels set a decade ago.

These numbers are difficult to comprehend. The planet is in the process of shifting to new energy sources, and artificial intelligence presents countless possibilities. You’d think it would be a glorious time for corporate leaders to put their MBAs to work. A growing number of companies appear unwilling or unable to push through Canada’s multiple layers of regulation, a perennial irritant that might have morphed into an acute problem.

It’s reasonable to question corporate Canada’s tolerance for risk.

Former Bank of Canada governor Stephen Poloz set aside a few pages of his 2022 book on how the world is changing to talk about hurdle rates. Generally speaking, companies—and their investors—must be reasonably confident that any capital outlay will generate a greater return than could otherwise be had by investing that money in government bonds, paying off debt or buying back shares.

“I still routinely hear that companies or their boards require the same minimum, risk-adjusted rate of return that they always have,” Poloz wrote. This matters, he continued, because repeatedly hesitating to bet on longer-term rewards “can lead a company to dither into irrelevance, as other companies—ones that understand that real interest rates are likely to remain low on average for the next 30 years—snap up those investments and outperform dithering firms.”

Poloz isn’t the only former Bank of Canada governor who thinks executives and investors might need to adjust their expectations to match the world in which we live. David Dodge, who led the central bank between 2001 and 2008 and is now an adviser at Bennett Jones, used the firm’s mid-year economic outlook to call on governments to make productivity their primary missions. They should use deficits to finance productivity-enhancing investments such as infrastructure and research, rather than programs that encourage consumption, he wrote.

Increased household savings would enlarge the pool of capital for longer-term projects. Notably, Dodge also called out companies, saying they could be “distributing a smaller share of the profits, retaining more for investment.”

Former Bank of Canada governor David Dodge in Ottawa in January 2007. Photo: The Canadian Press/Tom Hanson

All of this amounts to gentle nudging compared with Mark Carney’s “dead money” jibe from 2012—the former Goldman Sachs investment banker was still running the Bank of Canada when he chided corporate leaders for hoarding cash that he reckoned could be put to more productive use.

Taken together, the various displays of frustration with corporate Canada by the country’s three previous central bank governors suggest jawboning will have little effect on business investment.

One thing that might? A concerted effort by governments—not simply the federal government, everyone’s favourite target, but also those of the provinces and biggest cities—to do something about the regulatory thicket that appears to have become an actual impediment to business rather than a mere annoyance.

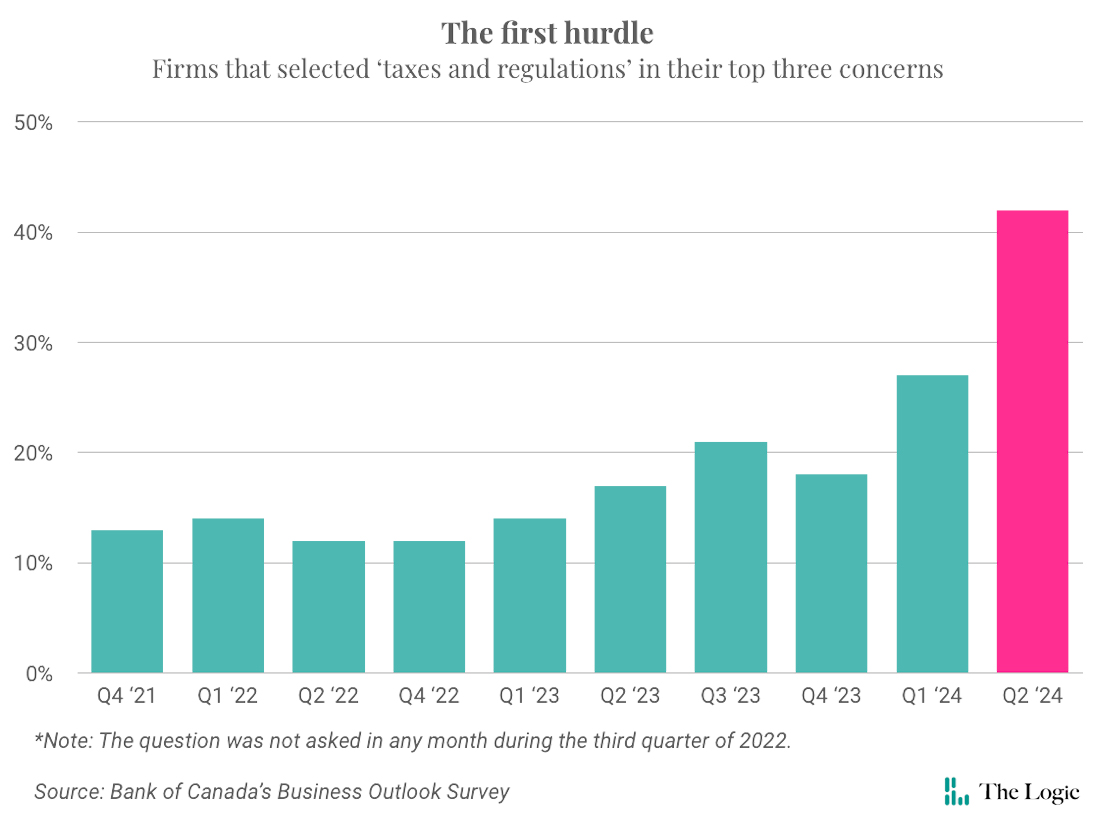

Business lobbyists have been grumbling about regulation for as long as central bankers have been questioning the bravery of Canadian CEOs. But there’s reason to think something has changed.

The Bank of Canada’s second-quarter business outlook survey showed that 42 per cent of respondents listed “taxes and regulations” as a primary concern, compared with 27 per cent in the first quarter and 17 per cent a year earlier.

That’s an unusually large and rapid shift in opinion. The only issues that ranked as larger concerns were “uncertainty” and “cost pressures,” but both of those were little changed from recent quarters.

In June, I interviewed Michael Waters, CEO of Minto Group, one of the country’s biggest real estate companies, and asked him if he’d consider lowering his hurdle rate. If anything, he said he’d likely increase it: the return he needs to deploy fresh capital is higher. “For me, as a developer, I do see a heightened level of risk,” said Waters.

Minto is getting a push from a significant tailwind: the extreme mismatch between demand and supply for homes. But the headwinds are equally strong. Higher-for-longer interest rates have raised the cost of capital, and construction costs and municipal development fees have grown much faster than the broader consumer price index.

Waters said his bankers insist on a “nice thick margin for error” as a cushion against the inherent unpredictability of the real estate business. “All those lenders, they’ve got regulators scrutinizing their loan books, and in turn it’s coming on us,” Waters said. “It’s actually served us well,” he continued. “There are developers failing. What could have been more significant collateral damage has not developed.”

There’s room to disagree with Waters over his assessment of the big banks, as the highly concentrated finance industry is an excellent example of something else Statistics Canada observed in its productivity report—that a lack of competition removes an important incentive to invest.

But there’s little to critique about what he has to say about regulation. The cost of capital is probably the biggest headwind facing developers, and higher interest rates are only one factor. Waters says the regulatory environment has become so uncertain that he can’t promise when land that Minto has banked will be zoned for development, when he’ll get a permit, or even how many storeys he’ll be allowed to build. Investors demand compensation for all that uncertainty. It’s often more than Minto is willing to accept.

Maybe companies should accept narrower margins and lower hurdle rates. It seems unlikely they will under current conditions. They’ve decided there are too many obstacles in the way.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.