During testimony at the Senate banking committee earlier this year, Bank of Canada governor Tiff Macklem was asked whether the central bank, home to the country’s greatest concentration of economists, made time for psychology.

Skip to content

Commentary

Negative self-talk masks the real issues with Canada’s economy

Maybe the vibecession narrative was too glib. That doesn’t mean it was altogether wrong.

Soaring food prices are a real source of frustration among Canadians, causing financial anxieties for households. Photo: The Canadian Press/Frank Gunn

During testimony at the Senate banking committee earlier this year, Bank of Canada governor Tiff Macklem was asked whether the central bank, home to the country’s greatest concentration of economists, made time for psychology.

Elizabeth Marshall, a Conservative senator from Newfoundland and Labrador, observed that sometimes the Bank of Canada is “robust” in its messaging, while other times it’s “muted.” She wanted to know how the Bank of Canada decides when to hit us over the head with a message, rather than simply nudge us in a particular direction.

The query brought laughter, including from Macklem. “We’re not psychologists, but I can assure you we don’t wing it,” the governor said.

Marshall’s question might be less frivolous than you think. If there were more psychologists at the Bank of Canada and the Finance Department, policymakers might have found a way to close the gap between lousy sentiment data and solid-to-strong hard data. The disconnect matters because narratives become reality. We’re not in a recession, but our glum mood could create one.

Related Articles

“Canada needs a sentiment check, otherwise it risks talking itself into decline,” Rebekah Young, head of inclusion and resilience economics at Scotiabank, wrote earlier this year. “Without a shift to a more constructive conversation about Canada’s future, this could be as good as it gets.”

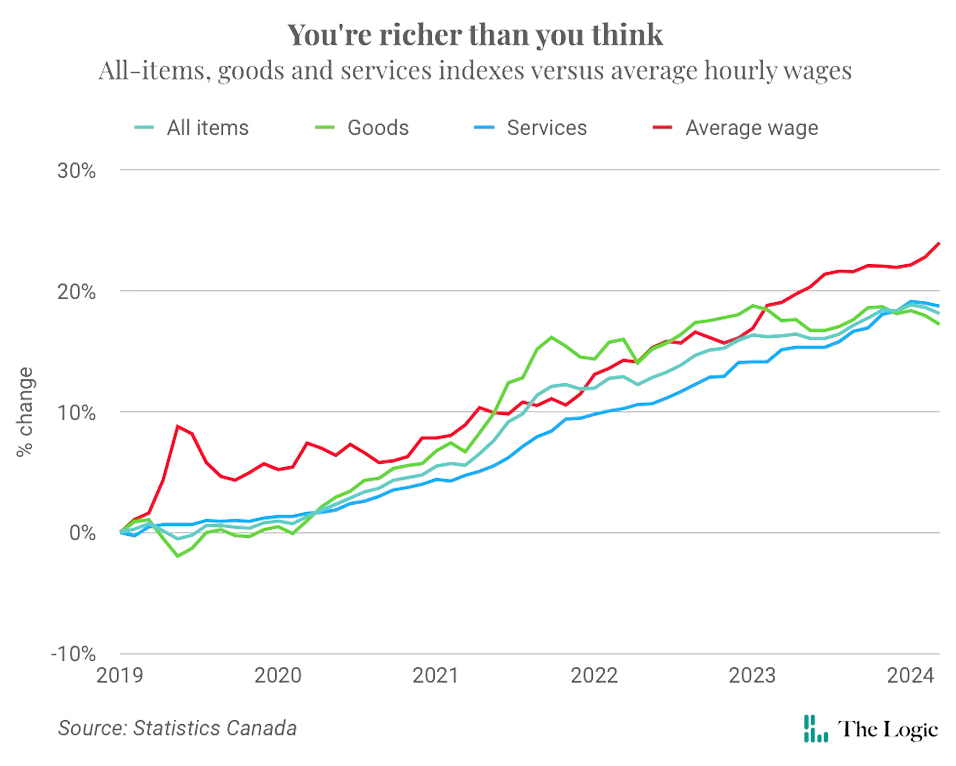

Inflation is the easiest way to frame what’s going on. Economists and governments look at the data and see a recovery from the COVID crisis. Most prices remain significantly higher than they were at the end of 2019, but average hourly wages have increased by an even greater amount. If that’s your dashboard, then the conclusion is that the economic machine is running fine.

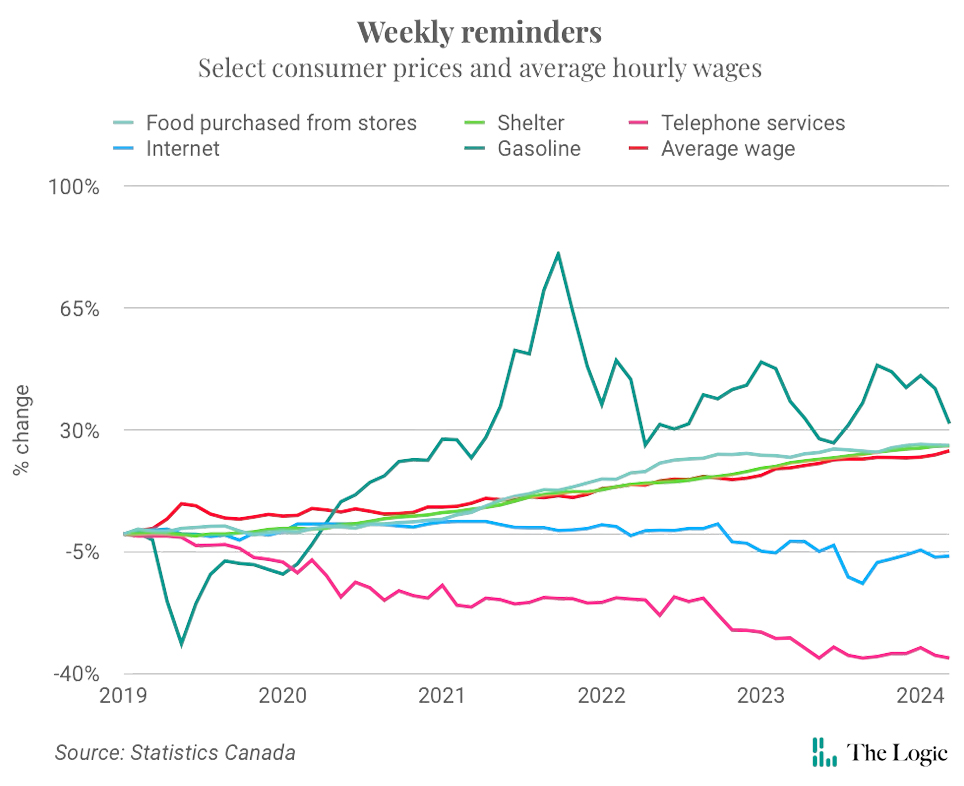

But most households are running dashboards that match what they see every day. The Logic commissioned Abacus Data to conduct a poll on the root causes of households’ financial anxiety a couple of weeks ago. Three-quarters of respondents expressed angst over the price of food, and 45 per cent lamented the price of fuel and other sources of energy.

The results echo something that economists broadly understand—that perceptions of prices and inflation are based on what we buy most frequently, not an aggregate of the hundreds of items that millions of consumers are purchasing at any given time. Put those numbers on a chart and the world looks different. Average hourly wage growth has been extraordinary since the COVID-19 pandemic, but not extraordinary enough to match the increase in the price level of food and energy.

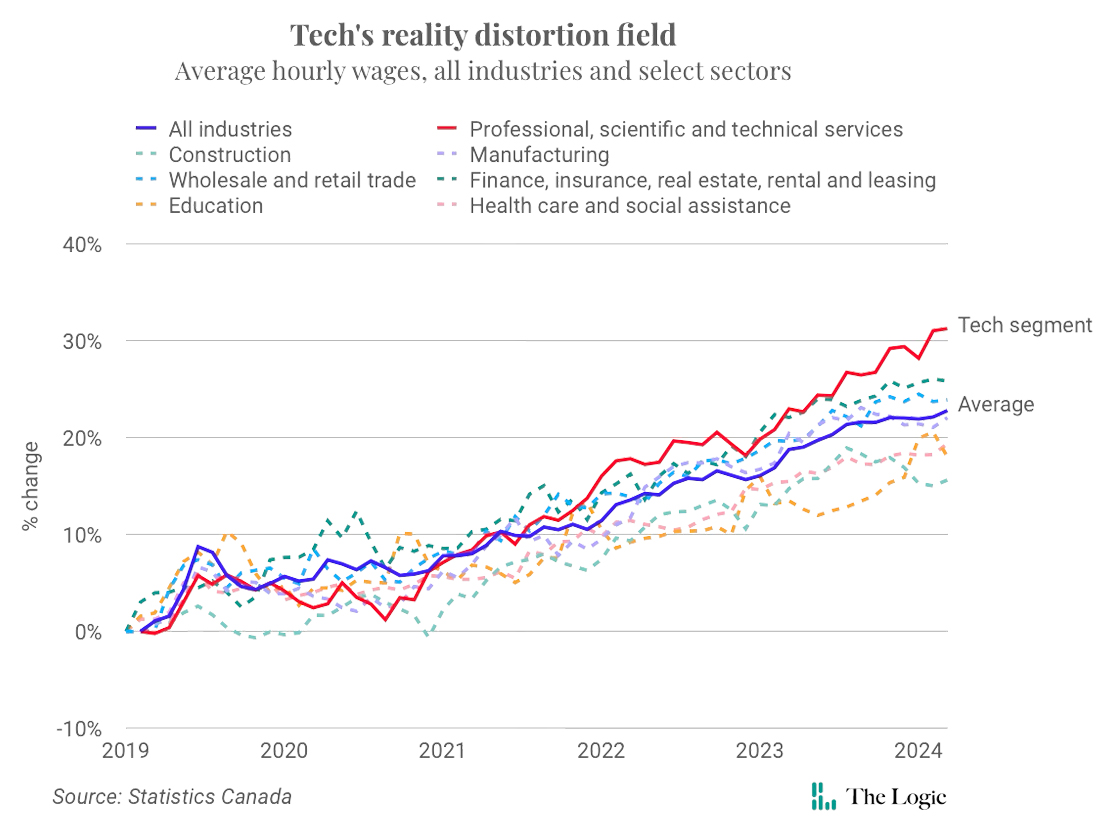

The average wage also obfuscates what life is like for a lot of people. Outsized pay packets at technology companies exaggerate the extent to which higher salaries have offset higher prices. Some 1.5 million people are captured by Statistics Canada’s “professional, scientific and technical services” category, where the average hourly wage has increased more than 32 per cent since the end of 2019. About 2.7 million people work in retail and wholesale, where wages have increased about 24 per cent over the same period.

That’s why the “vibecession” meme isn’t aging well. If you spent your time staring at the first chart, you might think that it would be only a matter of time before sentiment aligned with an economy that looked good on paper. But as Alberta Central economist Charles St-Arnaud showed earlier this year, the surge in immigration was floating aggregate employment and overall economic growth. Individual households were actually cutting their spending. There was more information in those sentiment surveys than many realized.

Concluding the vibecession narrative was too glib doesn’t mean it was altogether wrong. Young’s strength as an analyst is her ability to hold contradictory thoughts at the same time. She’s been trying to convince people to resist doomerism and instead focus on what she sees as serious cracks in the foundation.

Over the summer, she pieced together publicly available data to show that most households—including younger ones—were much wealthier than they were in 2019 because of increases in the value of real estates, savings and disposable income. This week, she published a follow-up report based on Statistics Canada’s Survey of Financial Security for 2023, the first such release since 2019.

Among other things, the new data show that median net worth of all households had increased by a third, and that the pace of inflation-adjusted wealth accumulation was eight per cent—double the pace of the previous two decades. Lower-income households are also significantly wealthier, suggesting gains are no longer concentrated at the top.

The median net worth of households led by someone 35 or younger had tripled, suggesting that many millennials and members of the generation Z cohort are doing better than we’ve been led to think. About 44 per cent of that group owned their primary residence, a gain of almost nine percentage points from 2019. Fifteen per cent of younger renters had a net worth greater than $150,000, compared with five per cent before the pandemic, thanks to investments in real estate and financial assets.

“The picture is remarkable,” Young wrote.

Remarkable, but imperfect. Renters, overall, are disconcertingly poorer than homeowners. The value of employer-sponsored pension plans declined for the first time since Statistics Canada began publishing the survey, something Young called a “serious” red flag.

These could be the real sources of financial stress, manifested in frustration of food prices and notions that younger people are struggling to get ahead. Psychology offers explanations. The pandemic was a traumatic experience that continues to affect mental health. Inequality stokes resentment and irrational assessments of our own success. Cognitive biases cause us to emphasize the negative and recoil in the face of uncertainty.

Maybe it shouldn’t be a surprise that policymakers have struggled to convince us that all is well. They lack the tools to get a proper handle on the vibes. They ought to work on that.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Frank Gunn

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Subscriber Survey

Most of you think AI will change your job, but not replace you

Briefing

TC Energy says North American natural gas demand is growing much faster than previously expected

Mississauga imposes data centre pause, as Toronto councillors scrutinize local projects

A third of Canadian workers are using generative AI, but not for everything

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.