The most helpful thing I read this week might have been venture investor Chris Neumann’s post on the value of going for a walk.

“Work as many hours as you want to but make sure to find your recharge,” Neumann wrote in an essay timed to drop in the inboxes of his followers on the morning of Nov. 6. “Don’t be afraid to step back from your screen and go outside. Try a new restaurant. Take a walk in the woods. Talk to someone who isn’t in tech.”

Narrowly, Neumann’s post was about work-life balance. But he also anticipated that the outcome of a historic election would create waves of fear and loathing, no matter the result. If The Logic’s pre-election subscriber survey is a guide, the reaction of Canadian decision makers to Donald Trump’s victory was mostly fear. More than 80 per cent of respondents said Vice-President Kamala Harris would be better for Canada.

Instead, more than 73 million Americans opted to return “Tariff Man” to the White House, along with Republican majorities in both houses of Congress. That means we’re at the mercy of a personality cult that has a loose commitment to democratic norms, and to the U.S.’s role as protector of the postwar economic order and bulwark against the spread of autocracy. “The world economy always needs a hegemon,” economic historian Brad DeLong wrote in his 2022 book Slouching Towards Utopia. The world may no longer have one.

Let’s not panic. Historians such as DeLong show us what could happen. That doesn’t mean whatever they conjure from the past is destiny. We still get a say.

Neumann’s advice is important because Canada’s leaders went down a rabbit hole the first time Trump was elected. Prime Minister Justin Trudeau’s everyone-to-the-barricades approach to the NAFTA renegotiation consumed most of Ottawa’s attention for the better part of two years, depleting human and political capital that could otherwise have been used for other purposes.

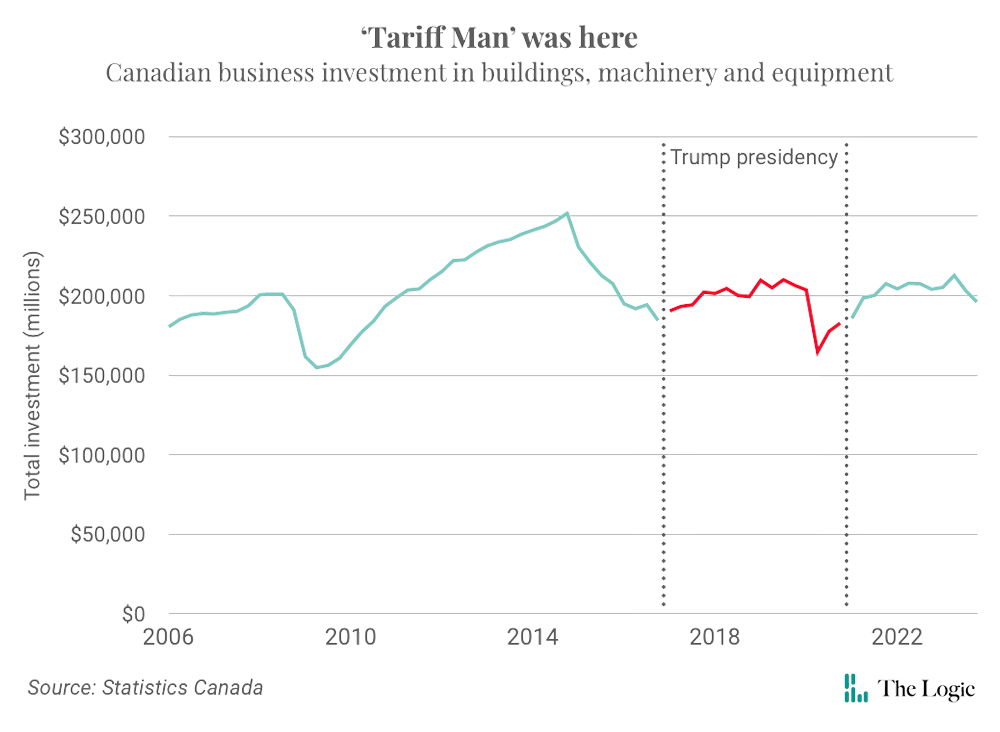

Executives were no less rattled. Canadian business investment effectively stopped during the first part of the Trump presidency. The skittishness of CEOs and their boards exacerbated the effects of the collapse in oil prices in 2014 and 2015, and probably at least partially explains Canada’s post-pandemic productivity crisis. Investment in non-residential structures and machinery and equipment averaged roughly $208 billion per quarter in 2019, the most since Trump took the oath of office in 2017, but still lower than 2015.

Such a response to the second Trump presidency would be devastating.

Output per hour worked, perhaps the best marker of an economy’s ability to generate wealth, declined in every quarter but one between the third quarter of 2020 and the second quarter of this year, the most recent period for which Statistics Canada has released data. That means Canada’s ability to generate growth is severely compromised. Debt-fueled household consumption, housing and government spending have done most of the work under Trudeau, and all those engines are maxed out. If trade and investment don’t take over, the economy will struggle to regain momentum in the near term.

“There is certainly a dark side, but change is also a moment of opportunity,” Bank of Canada governor Tiff Macklem said on stage at The Logic Summit on Oct. 28. “My advice to Canadian companies is, be alive to those.”

A common mistake in forecasting is projecting forward past shocks without adjusting for changes in the interim. The Great Recession was bad, but it wasn’t devastating like the Great Depression of the early 1930s because central banks had become better at executing monetary policy. The COVID-19 recession was relatively short because one lesson from the Great Recession was that governments had been too conservative with fiscal stimulus.

Expect arbitrary tariffs and trade wars. But north-south commerce has a way of surviving conflict. Canada’s Paul Revere was a messenger called James Vosburgh, who raced north on June 25, 1812, to warn that Congress had declared war on Britain. Vosburgh wasn’t a Loyalist. He was dispatched by John Jacob Astor, one of the new republic’s richest men, who was tipped off about what was happening and wanted to protect his Canadian assets from confiscation. Vosburgh escaped being charged with treason because there was no law that forbade sharing commercial news.

The first Trump shock was brutal because Canada was asleep at the switch. Companies now regularly talk about political risk advisers. Trudeau sent Team Canada back into the field months ago in anticipation of the new North American trade agreement’s renewal in 2026. This week, he reassembled Finance Minister Chrystia Freeland’s special cabinet committee on Canada-U.S. relations. “It will operate in the way the COVID committee operated, bringing together ministers to address in a working fashion an urgent issue,” Freeland told reporters in Ottawa on Friday after the committee’s first meeting.

Freeland said she’d already met with the heads of the big banks and representatives of the steel and automobile industries, and was scheduled to talk to the leaders of the eight biggest pension funds. She’d also scheduled meetings with oil and gas companies and labour leaders.

The message: back to the barricades. Given the stakes, that’s the obvious play. One thought, though.

Michael Wilson, the Progressive Conservative finance minister and trade minister who helped negotiate the original Canada-U.S. trade agreement, wrote in his memoir that he was motivated by the idea that “strong economies tend to support strong democracies.”

Canada’s economy was weak when Brian Mulroney’s Progressive Conservatives won power in 1984. It had been battered by a recession, inflation and high interest rates. Much like today, economists worried about limp productivity and competitiveness.

Trade deals with the U.S., and eventually Mexico, helped turn things around by delivering a positive shock. That’s because they were new. Defending an arrangement that Canadian business has come to take for granted won’t have the same effect. Protecting Canada’s economy from Trump will require the kind of policy change that Mulroney and Wilson executed in the 1980s.

Reassembling Team Canada is necessary, but insufficient. The biggest threat to Canada’s economy is the productivity crisis. The answer to that problem will be found on this side of the border.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.