Talent Quarterly is The Logic’s regular series on employment trends.

Concerns about Canada’s aging population are, well, old. Researchers have been warning about our steadily greying workforce as far back as 1986, and it’s remained the flashing red beacon of the economy for decades.

The consequences of that aging process are only now beginning to bite. While rising retirement levels have helped keep Canada’s labour market tight—including in the fourth quarter—they also pose major long-term risks that could complicate everything from the growing skills gap to Canada’s ability to reach its net-zero targets.

Talking Point

- Canada’s high rates of retirement in recent years will bring longer-term challenges to the labour force, including pressure on wages and talent shortages in critical industries like cleantech that could complicate the country’s ability to reach net-zero targets

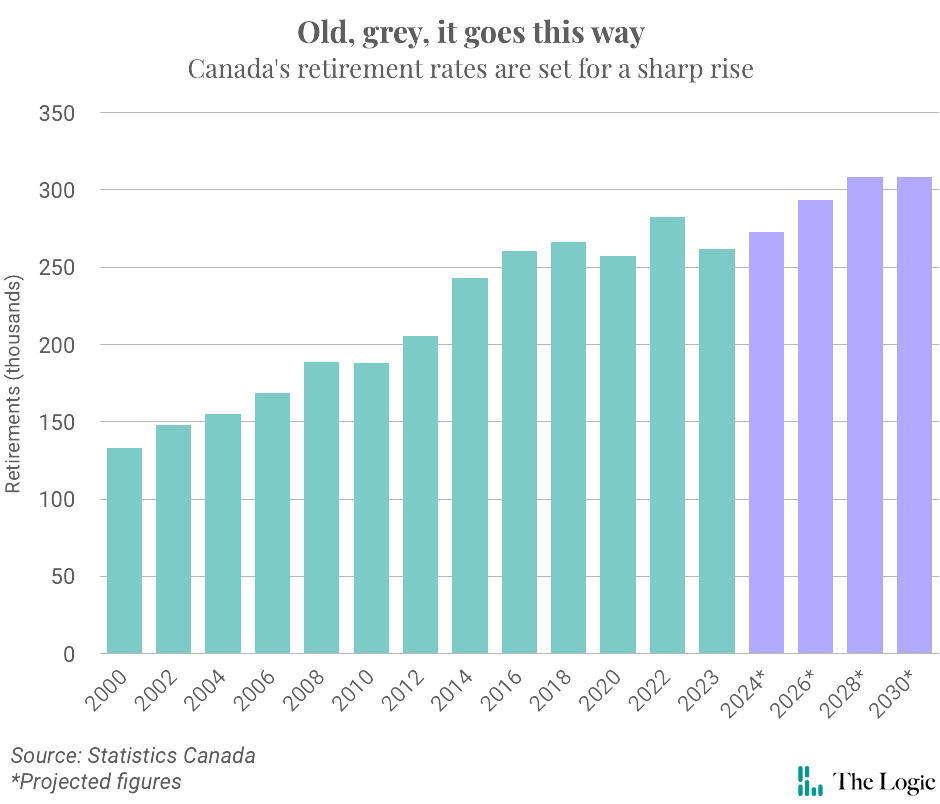

In 2023, around 262,000 people retired, according to Statistics Canada (see chart below). That’s 1.3 per cent of Canada’s total workforce that, should the general trend continue, would need to be replaced every year. Experts say high retirement levels are in part responsible for keeping wages elevated and employment rates steady, even as the economy shows signs of cooling off. (From October to the end of December, employment remained little changed at around 62 per cent.) But the real impact from the next wave of retirees could come further down the road.

Green targets, green workforce

Tricia Williams, a researcher at the Future Skills Centre, said retirees across countless industries have been taking their expertise with them, leaving major skills shortages in their wake. Retirement levels peaked in 2022 and came down slightly in 2023, but have remained elevated for the last seven years aside from a brief pandemic lull.

“Across the board it’s a huge challenge,” Williams said. “We’re starting to really see the retirements and the movement of the boomer generation more firmly into the retirement era.”

Among those industries struggling with higher rates of retirement, she said, is the renewable energy sector and labourers in the electrical-utility space. The wind and solar sector in particular faces a “huge wave” of retirements in the next five to 10 years.

By the numbers:

64.6%: The labour force participation rate—or, the percentage of the country’s population that is in the workforce—in 2033, according to the Conference Board of Canada’s estimates. Participation rates will bottom out in 2033 as more people retire and as population growth outpaces labour force growth.

16,000: The number of health-care and social-assistance workers Canada added in the month of December 2023, according to Statistics Canada. The growing sector added 124,000 jobs in the 12 months ended December as the aging population strains Canada’s health-care systems.

1.2 million: The increase in Canada’s population in 2023 alone, a 3.2 per cent rise from 2022. High immigration levels will help cover some of the losses from retirements, one expert says, but more re-skilling is needed to fill the gap.

That could put more strain on Canada’s costly efforts to build out its electrical grid to match rising demand, with provinces like B.C. and Quebec outlining major plans to bulk up their emissions-free capacity.

“In order to meet our net-zero targets, we have enormous labour requirements,” she said.

So far, Canada has managed to fill a lot of those skilled positions by juicing immigration levels, Williams said. Last year, the country’s population grew at the fastest rate on record, mostly due to immigration. But that is only part of the remedy. Crucially, companies and public organizations need to ramp up efforts to retrain workers, which continue to lag demand despite the rollout of various new programs.

“We’re finding that employers are not investing as much in Canadian employees at a time when we really need to be thinking about upskilling and making sure that the workforce has the right skills,” she said.

“Immigration alone is not going to solve the gap.”

Silver lining in the pay book

While an aging workforce is sure to put added pressure on companies and managers, there’s a bright spot for workers themselves: wages. Worker pay is already high, and is likely to remain so for years to come, according to a recent long-term study of labour market trends by the Conference Board of Canada.

People on the move:

- BlackBerry promoted John Giamatteo to CEO, replacing longtime chief executive John Chen.

- GM Canada head Marissa West was promoted to senior vice-president and president of the automaker’s North America division. Kristian Aquilina replaced her as GM Canada’s president and managing director.

- Winnipeg-based SkipTheDishes appointed Paul Burns, previously managing director of Twitter Canada, as CEO.

- Ether Capital’s CEO Brian Mosoff stepped down on Jan. 1. Founder Som Seif is the interim CEO.

- B.C.-based crypto company BIGG Digital Assets announced that Dan Reitzik will serve as interim CEO. He replaced Mark Binns, who also stepped down from the board of directors.

- Ecobee’s founding CEO and president Stuart Lombard retired.

- Brookfield appointed former Worldpay payments head Ron Kalifa as vice-chair and head of financial infrastructure investments.

- The Bank of Canada appointed Nick Leswick as executive director of policy, effective Jan. 9.

- Brian O’Neil was appointed as chairperson of BDC’s board of directors.

- Fulcrum Capital Partners promoted James Morrison to partner.

- Investissement Québec appointed Element AI alum Sarah Larose as its new director for the battery sector.

- RBCx—RBC’s innovation and startup banking division—hired four former Silicon Valley Bank Canada staff to focus on early-stage startups and its life-sciences practice.

The Conference Board expects retirements will keep wages growing at an average 3.2 per cent between 2023 and 2030, outpacing annual inflation of 2.7 per cent. That will help workers slowly recover some of the pocketbook pain that they felt during the recent period of high inflation, but it could also backfire if wages rise too high and become unsustainable.

So far that hasn’t happened, said Pedro Antunes, chief economist at the Conference Board. Despite the rising cost of labour, a mixture of recent volatility, retirements and other factors are causing businesses to retain their workforces.

“They’ve had a really tough time hiring workers over the last three years, and they don’t want to let go of their workforce,” he said.

Work from home goes bust?

Higher wages and a stubbornly tight labour market both lead to greater competition for talented workers. That can put pressure on companies to offer more work-from-home options to the portion of employees with an “overwhelming” desire for flexible arrangements, Williams said.

It was therefore a bit surprising that Statistics Canada recently said that the percentage of people working mostly from home dropped to 20 per cent in November 2023, sinking well below an April 2020 peak of 40 per cent. The decline comes as major banks like RBC and TD, as well as Canadian tech firms like Dye & Durham, last year ordered workers to return to the office more.

Williams, for her part, said Future Skills Centre data suggests there’s been a more moderate fall in WFH arrangements. The centre found that the number of people working in either remote or hybrid arrangements increased in 2023 to 26 per cent, up slightly from 23 per cent in 2022. The figure peaked around 34 per cent mid-pandemic.

“We’re seeing a lot of stability, so we’re not necessarily seeing the drop-off,” she said.