Michael Wekerle is looking forward to a break from the drama at WonderFi, even though he played a key role in it.

The way Wekerle tells it, he’s been busy trying to extract himself from a high-profile boardroom scuffle between two companies on whose boards he sits: WonderFi, the Toronto-based company that owns half of Canada’s registered crypto trading platforms, and Mogo, a Vancouver-based fintech that owns a 13 per cent stake in WonderFi.

“There was too much disagreement at the board level,” he said. “They need to be more focused on executing the plan.”

The flamboyant former “Dragons’ Den” star is best known for his TV gig, if not for his ownership of legendary Toronto nightclub the El Mocambo or his restaurant partnership with actor Mark Wahlberg, but he made his fortune in merchant banking. Difference Capital, a merchant bank he co-founded, merged with Mogo in a share swap in 2019; Wekerle became a Mogo director.

That transaction kicked off a series of events that, five years and one cycle of crypto boom and bust later, has led to a very public brawl featuring a cast of characters that includes Bay Street wild child Wekerle, one of his fellow former Dragons, one of Canadian tech’s most controversial executives and an activist Miami hedge fund that literally makes chaos its calling card.

Talking Points

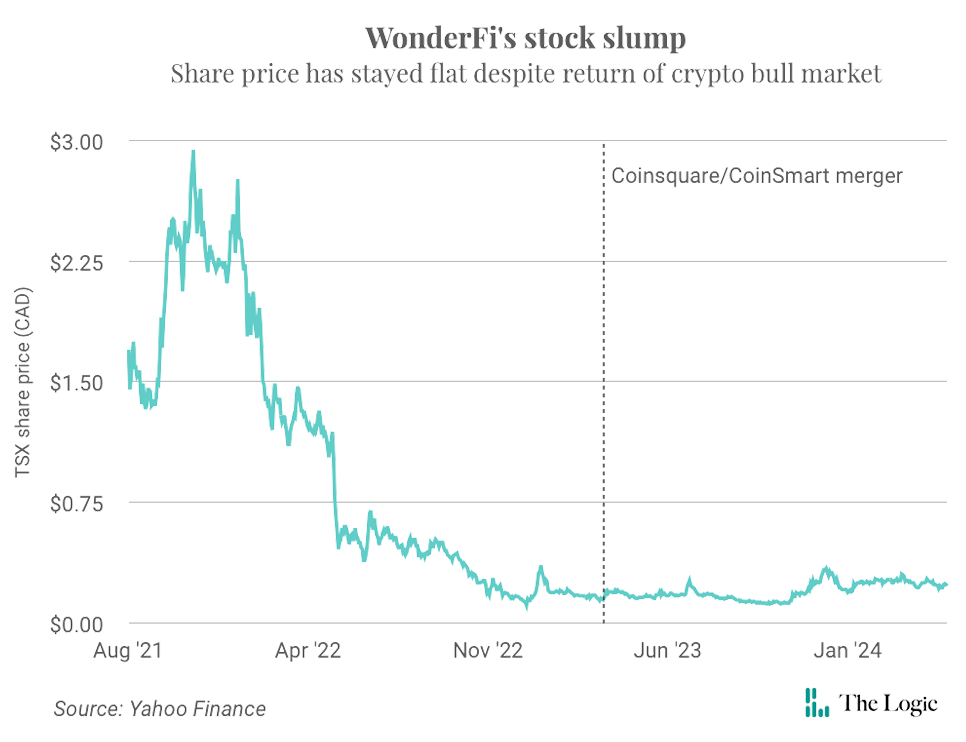

- Toronto-based crypto-trading company WonderFi is working to position itself as Canada’s safe, blue-chip choice for mainstream crypto investors. But it also has a propensity for high-profile drama, as evidenced by its recent boardroom brawl

- WonderFi’s annual meeting Friday will see a vote on a deal to settle the dispute between the company, its biggest shareholder and an activist hedge fund

Though a resolution appears imminent, the drama has cast a shadow over WonderFi’s efforts to position itself as Canada’s safe, blue chip choice for mainstream crypto investors. These big personalities must now work together to build a company that, to fulfill its ambitions, might just need to be a little more boring.

At the heart of the recent drama is Adam Arviv, CEO of hedge fund Kaos Capital and a longtime professional contact of Wekerle’s. Arviv’s fund has offices in Toronto and the Bahamas; its previous activist targets include cannabis company Hexo. Wekerle said he initially put Arviv in touch with WonderFi’s management about an equity financing proposal. WonderFi turned it down. However, in March, Kaos—which on its own only held about one per cent of the crypto company’s shares—teamed up with Mogo, WonderFi’s biggest shareholder, to call for an overhaul of WonderFi’s board.

“The current Board has overseen extremely poor performance as compared to other public securities in the global crypto space during the strongest bull run in history for crypto currencies,” said the release in which Kaos announced its activist campaign. Kaos accused WonderFi’s “weak” board and management of letting the stock price languish “far below its true intrinsic value.”

Despite a rebound in crypto prices, record trading volumes and a swing to profitability, WonderFi’s stock had dropped about 10 per cent between the end of 2023 and March 26, the day before Kaos announced its activist campaign. As Kaos pointed out, Delaware-incorporated competitor Coinbase returned 53 per cent over the same period, while the price of Bitcoin increased 64 per cent.

Kaos and Mogo decided that wasn’t good enough. In Kaos’s release, Arviv urged WonderFi’s board “to participate in an orderly transition, given that change is inevitable.”

The press releases have flown back and forth for months since, with Kaos calling WonderFi’s board “entrenched and disorganized” and WonderFi accusing Kaos of having “a fundamental misunderstanding of WonderFi’s business.” WonderFi singled out Wekerle, saying he acted as a conduit for what it alleged was an attempt by Mogo to gain control of the company without paying shareholders a premium. Wekerle says that isn’t true.

Drama and big personalities have been a through line for WonderFi throughout its brief existence.

When a turbulent attempt at a merger between rivals Coinsquare and CoinSmart failed last summer, WonderFi swooped in and acquired them both, a bold move that rolled up some of the country’s best-known crypto brands—and, crucially, companies that held coveted regulatory licences—into a domestic crypto giant.

The name “WonderFi” is itself a nod to “Mr. Wonderful,” the nickname of celebrity investor Kevin O’Leary, whom Wekerle replaced on “Dragons Den” in 2014 when O’Leary left to star in the show’s U.S. counterpart, “Shark Tank.” O’Leary invested in the company in a 2021 financing round, before it went public through a reverse takeover, and has since served as a face of the company.

“The era of the crypto cowboy is over. We don’t want any crypto cowboys.” — Kevin O’Leary

In a 2022 interview with The Logic, O’Leary said he saw a lot of potential in WonderFi’s strategy of rolling up trading platforms in a country that’s relatively crypto-friendly. “This industry is so ripe for consolidation, because everybody’s figured out customer acquisition is not easy,” he said. “I’m very excited.”

Meanwhile, the committee that worked out how to combine the WonderFi, Coinsquare and CoinSmart teams was led by Noel Biderman. He is the former CEO of the Toronto-based company that owns Ashley Madison, a website for married people seeking affairs. Biderman stepped down as CEO of that company after an infamous 2015 hack of Ashley Madison, which revealed Biderman had overseen the proliferation of bot profiles purporting to be real women, repeated elaborate schemes to deceive media covering the company and the posting of a fake “trusted security award” on the site. The saga is the subject of both a 2023 Hulu documentary and one Netflix released last week.

Last month, amid the fight with Kaos and Mogo, WonderFi appointed Biderman, along with Jaime Leverton, the former CEO of Canadian Bitcoin miner Hut 8, to its board.

“It’s behind us”: Jamie Leverton, one of WonderFi’s newest board members, says she doesn’t think the boardroom turmoil will hurt the company’s brand with customers or regulators. Photo: Christopher Katsarov Luna for The Logic

WonderFi CEO and board member Dean Skurka declined a request for an interview about the conflict over the company’s direction. WonderFi instead offered Leverton as its spokesperson, who said that while she was unable to comment on board deliberations, she does not believe the turmoil will hurt WonderFi’s brand as it works to build trust with customers and regulators. “I think it’s behind us,” she said.

However, the roots of the recent dispute run deep, and have parallels with how WonderFi formed. Then and now, a flurry of press releases ended in a surprise deal. Then and now, the deal came with assurances everyone would be able to put the incident behind them and work together.

Mogo, the company WonderFi accused of trying to seize control via Wekerle and Kaos, was founded in 2003 by Dave Feller, who remains its CEO and board chair. It offers a wide range of fintech products, from personal loans to stock trading, and made some early moves to let its clients buy and sell crypto.

In 2021 it invested in Coinsquare. At the time, Coinsquare was trying hard to shed the stigma of its 2020 settlement with the Ontario Securities Commission over wash trading and reprisals against a whistleblower. To that end, it overhauled its executive team and started working toward registration with provincial securities regulators, who had begun cracking down on the sector.

Despite its bad press, Coinsquare was one of the country’s most popular domestic platforms, and the crypto market was in the early stages of a spectacular bull run. Between April and June 2021, Mogo built up a 34 per cent stake in Coinsquare, plus warrants to acquire additional shares that would give it majority control if exercised.

The following year, crypto’s fortunes reversed. The May 2022 collapse of the stablecoin Terra and related token Luna sparked a string of bankruptcies in the sector and kicked off a prolonged bear market. Struggling crypto-trading platforms with coveted regulatory licences became acquisition targets—WonderFi added rival Coinberry to its portfolio and Coinsquare announced plans to buy publicly listed competitor CoinSmart in a $29-million cash-and-stock deal in September of that year.

Mogo had previously touted its exposure to crypto, “the fastest-growing asset class.” But by October 2022, it was reassuring investors its main exposure to digital assets was only through its stake in Coinsquare. That month, Mogo let its warrants to acquire more shares of Coinsquare expire. About two weeks later, Mogo’s shares fell below US$1, the minimum price required to maintain its listing on Nasdaq Capital Markets.

From left: WonderFi CEO Dean Skurka, Coinsquare CEO Martin Piszel and CoinSmart CEO Justin Hartzman at the time of the companies’ surprise triple merger in April 2023. Photo: Bitbuy | Handout

In January, CoinSmart announced Coinsquare had called off the acquisition deal. Wekerle, a Mogo director, told The Logic it would not be accurate to say Mogo “scuttled” the deal, but the company “always had the opinion it was not the right transaction.”

A source familiar with the matter, whom The Logic agreed not to name because the discussions were confidential, confirmed that Mogo was a significant influence in the decision. Coinsquare directors were concerned about the financial disclosure requirements and liability that would come with acquiring a public company, the source said.

Three days later, BNN Bloomberg reported WonderFi and Coinsquare were in merger talks. CoinSmart responded by saying it would take Coinsquare to court. With tensions running high—and cash reserves running low as the bear market dragged on—the companies came to a surprise triple merger agreement in April 2023.

Through its investment in Coinsquare, Mogo became WonderFi’s biggest shareholder, its 13 per cent stake accounting for about 33 per cent of Mogo’s $59-million market capitalization. Like WonderFi, Mogo’s stock price has suffered a steep decline since 2021, losing 94 per cent of its value between April 21, when it peaked at $27.87, and the close of markets Thursday.

A few weeks ago, WonderFi, Kaos and Mogo reached a potential resolution to their dispute, announcing they had struck a deal that would see Mogo divest roughly a quarter of its WonderFi shares, and in which the parties agreed to a list of nine directors nominated for election at WonderFi’s annual meeting Friday. It includes just three incumbents, rather than the five WonderFi initially wanted, meaning the board will have six new members.

If shareholders endorse it, the agreement will give Kaos and Mogo a combined three out of nine board seats.

Kaos’s Arviv said he was happy with the outcome. Kaos’s two seats and Mogo’s one are fewer than the five they had initially sought to give them majority control, but still “a productive result.”

“I was put in the middle of two factions that were historically not agreeing.” — Michael Wekerle

“It’s a fresh start,” said Arviv. “The old guard is gone.”

Among those leaving the WonderFi board is Michael Wekerle. The decision not to put his name forward for re-election was his own, Wekerle said, because of his concerns about WonderFi’s “lack of direction.”

“I think it was time for a clean slate,” Wekerle said. “I was put in the middle of two factions that were historically not agreeing on the same direction.”

Mogo offered little comment for this story. In response to emailed questions, Mogo CEO Feller sent a statement saying he is pleased with the agreement, thanks Wekerle for his contributions and respects his decision to stand aside.

It’s been just two months since WonderFi accused Mogo of attempting a coup, however, and tensions between the two companies linger. A source familiar with the negotiations that led to the agreement, whom The Logic agreed not to name so they could speak freely about confidential discussions, said the parties that didn’t back the activist campaign were determined to limit Mogo’s power over WonderFi, and see the single seat for Mogo and the requirement it offload some of its shares as a win.

Adam Arviv, CEO of Kaos Capital: “It’s a fresh start. The old guard is gone.” Photo: Handout

Kevin Dede, an analyst who covers WonderFi for New York City investment bank H.C. Wainwright, said he thinks it’s for the best that Mogo and Kaos didn’t get everything they wanted. “I don’t know what changes they would have implemented, or if they would have forced a merger [between WonderFi and Mogo],” he said.

Arviv declined to say what changes he’d like to make at WonderFi to improve its stock performance, but said he has “formulated a plan.” He predicted the company’s share price will be significantly higher in 12 months.

To make sure the company delivers, Arviv has chosen two personal friends to represent him on the board: Igor Gimelshtein, a former CFO of cannabis company MedReleaf, and Rob Godfrey, a businessman and son of former Postmedia and Toronto Blue Jays CEO Paul Godfrey. Arviv previously worked with Godfrey on the board of gaming company Bragg, where Arviv served as CEO, and in a previous activist campaign pushed to appoint Godfrey to the board of cannabis company Hexo.

If shareholders vote for the plan, as expected, there may at last be calm. However, WonderFi is now popping up in media coverage capitalizing on a surge in interest in Noel Biderman in the wake of the Netflix documentary about Ashley Madison—a boon for name recognition, but potentially detrimental to the safe, trusted brand the company is trying to build.

Biderman is nominated to continue serving on the board in one of the six seats not controlled by Kaos and Mogo. While Dede said Biderman’s history with WonderFi would make him a natural choice for a director absent his history with Ashley Madison, that past “certainly does call into question… moral behaviour,” he said. “It’s certainly interesting.”

Biderman declined to comment, but in an email his lawyer Ian Dumain said much of the information about his client’s activities as CEO of Ashley Madison’s parent company came from stolen documents and took place a decade ago.

Though he declined an interview, WonderFi CEO Skurka did send an emailed statement saying that Biderman “has been an invaluable strategic advisor to WonderFi, and we were very pleased when he agreed to serve as a member of our board of directors.”

Arviv said he didn’t have any concerns about Biderman’s past at Ashley Madison, saying he didn’t know a lot about the situation but believes “he shouldn’t have been held accountable for a breach.”

As for O’Leary, the company’s namesake, he said he isn’t concerned about Biderman either. He said the trouble Ashley Madison ended up in—with the U.S. Federal Trade Commission over its fake profiles, and with privacy regulators over the fake “trusted security award”—was unrelated to financial compliance, which O’Leary said has been his main concern with the crypto sector.

“The era of the crypto cowboy is over. We don’t want any crypto cowboys,” he said. “I don’t consider Noel a crypto cowboy.”

O’Leary—who said he’s not sure how big his stake in WonderFi is following its mergers with Coinsquare, CoinSmart and others—supports the proposed deal between WonderFi, Kaos and Mogo. He also said he believes WonderFi will ultimately succeed over its bigger international competitors because of its focus on compliance. Coinsquare, which was folded into WonderFi, was the first Canadian crypto platform to gain membership into the Canadian Investment Regulatory Organization, a hurdle only competitor Wealthsimple has cleared since.

“The shenanigans that occurred behind the scenes in the boardroom… that’s all irrelevant, as long as it comes out of the meat grinder remaining a compliant company,” O’Leary said. “If you’re not happy watching sausage being made, don’t own the shares.”