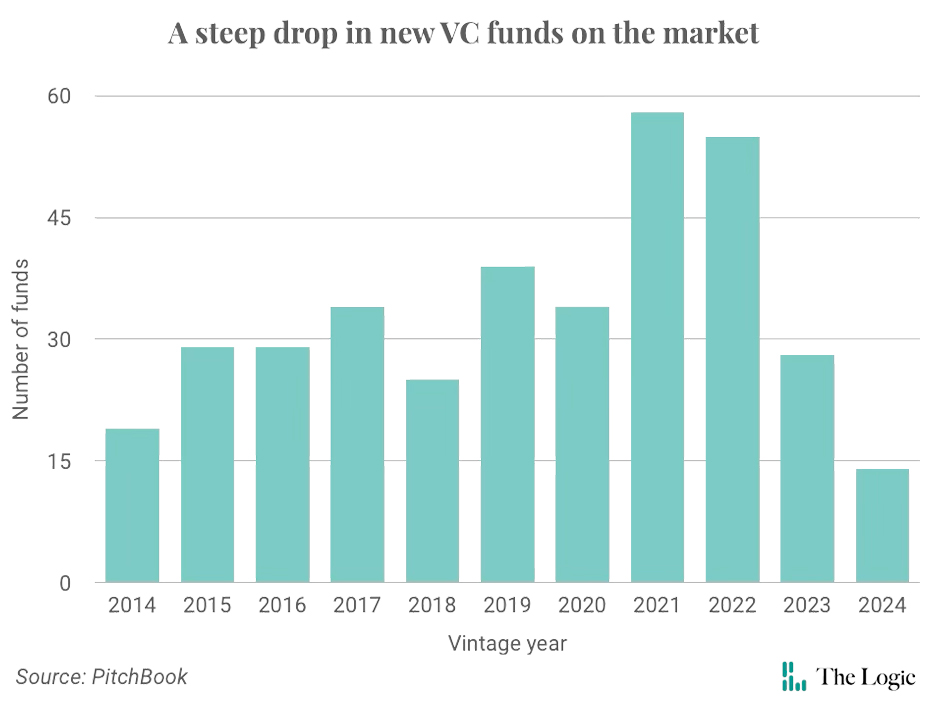

The number of new Canadian venture capital funds will hit a decade low in 2024, with just 14 funds having closed as of Dec. 18, according to PitchBook data. But lurking unseen in the data is a bigger problem: zombie funds.

These funds are run by firms that have quietly retreated from a difficult market. Unable to raise new financing but still managing old portfolios, the firms linger on the fringes, waiting for the right conditions to reemerge.

“People call them zombie funds because they’re like walking dead,” said Rick Nathan, managing director at Toronto-based Kensington Capital Partners, which invests in venture capital funds. “They don’t go out of business, they don’t go bankrupt, they just kind of survive,” Nathan said. Some funds may eventually have a big exit or two, giving them the fuel and credibility to go back out and raise another fund, he said. Others will ultimately perish.

Talking Points

- After years of weak venture capital returns, investors that back VC funds don’t have the cash they expected to reinvest into the market

- The lingering liquidity crunch could create a class of “zombie funds” that aren’t quite dead, but aren’t actively investing or raising new capital

Years of weak venture capital returns have created a liquidity crunch in the market, deterring the limited partners (LPs) that typically back VC funds from reinvesting in poor-performing firms. As VCs struggle to raise money, LPs say more firms are destined to go dark.

“There will be firms that either raise much smaller funds or don’t raise another fund, or just wait,” said Nathan. “The result being, a couple years from now, we will quite likely have fewer Canadian VC funds with available capital to invest than we’ve gotten used to in the last few years.”

A confluence of bad economic conditions over the past three years has threatened funds’ viability. The low-interest-rate era of 2020 and 2021 had emboldened investors to cut big cheques in startups at inflated valuations. When interest rates began rising in early 2022, valuations fell back to earth, leaving investors’ portfolio companies worth less than when they bought in. With values depressed, companies generally weren’t going public or being sold—erasing the main routes for generating money for their investors.

Now, after years of weak returns, LPs don’t have the liquidity they expected to reinvest into new venture funds.

PitchBook has called the lack of returns the gravest problem, among many, to have besieged the venture capital market in recent years. Cash back to U.S.-based LPs is the lowest it’s been since the financial crisis of 2007-2008, according to an October report from the intelligence firm. The average quarterly distributions had been in the single digits for eight straight quarters, down from the 16.8 per cent average over the previous decade.

Even for LPs that do have money to invest, years of bad returns have shaken their confidence in certain funds, said Nathan. While he said LPs are still meeting with VC fund managers as they try to raise money, investors want to see cash back before cutting cheques.

Senia Rapisarda, managing director at Harbourvest, a private equity firm that invests in venture funds, said emerging managers—typically VC investors with just one or two funds under their belt—may be most vulnerable. Those firms have fewer management fees coming in from LPs to support them through the funding drought. Rather than close shop entirely, though, she said they may opt to take a prolonged break. General partners of those firms may stop paying themselves and reduce their teams, she said, while managing their existing portfolio companies until the fundraising conditions improve.

Few Canadian VC firms have gone public about their own difficulties raising new funds. Toronto-based Information Venture Partners is an exception. The firm’s co-founders Dave Unsworth and Robert Antoniades announced in October that they abandoned efforts to raise a fourth fund, citing the market downturn and pressure to deliver quick returns. They’d continue investing, they said, in one-off companies if the opportunities arose.

Most firms that transition to zombie status will likely do so covertly, said Nathan. “They don’t want to be tagged as having tried and failed [to fundraise],” he said. “It’s way better to have just never tried.” That makes it hard to know just how many venture firms have gone off the market.

PitchBook data gives some indication of how quiet fundraising has become. The market peaked in 2021 with 58 new fully-closed funds in Canada, but has declined every year since.

PitchBook data also shows there are 48 Canadian VC funds that have started raising money since 2021 but have yet to hit their full fundraising targets.

Nathan said he’s less worried about those funds that have made an initial close—they have money committed and can start investing—particularly those that have raised more recently. “It’s a big achievement in this market,” he said.

LPs that spoke to The Logic emphasized that there’s still money available for good funds. Funds-of-funds—including those managed by Harbouvest and Kensginton—are flush with fresh capital from the federal government’s Venture Capital Catalyst Initiative. VC firms that have had solid returns, or new ones with compelling theses, stand to raise some of that money, said Beatrice Couture, a principal at Teralys Capital, which invests in VC funds as well as directly in startups.

Nathan said new entrants that have liquidity from other investments—including some corporate or institutional investors—may also help fill the void as other funds retreat. “It can be easier to invest in a brand new firm than to go back with a fund that you think has underperformed,” he said.

Rapisarda said slow fundraising periods aren’t unprecedented, nor are they permanent. “Venture is lumpy,” she said. There are signs that the VC market is already improving, she said, with investment dollars increasing over 2024. While exits have remained relatively slow, more investors are selling shares in their portfolio companies through secondary investment deals as an alternative way to generate liquidity.

The federal government, meanwhile, announced a string of new initiatives this month, including another round of VCCI funding, that would provide billions of public and private dollars to companies and funds.

The impact of those programs, if implemented—which is by no means guaranteed—is still years away and won’t save funds at imminent risk of turning to zombies. But falling interest rates and rising stock markets are creating conditions for an eventual recovery, investors said. “I’m seeing green shoots,” said Rapisarda. “I really hope many of these franchises that have good portfolios will stay put,” she said. “They’ve learned so much, the next time around, they will be able to ride out difficult times.”