The Bank of Canada was slow to recognize it was losing its grip on inflation, so governor Tiff Macklem has done the right thing by initiating a post-mortem of its COVID-era stimulus measures. The exercise should win back some credibility, and help settle the debate over the extent to which stimulative monetary policy made the past couple of years so difficult.

Skip to content

Commentary

Carmichael: Inflation isn’t everything—even to Tiff Macklem

The governor gets a message from the labour market

Tiff Macklem at a news conference in Ottawa in May 2024. With the inflation threat receding, the Bank of Canada is taking a closer look at the labour market. Photo: The Canadian Press/Justin Tang

The Bank of Canada was slow to recognize it was losing its grip on inflation, so governor Tiff Macklem has done the right thing by initiating a post-mortem of its COVID-era stimulus measures. The exercise should win back some credibility, and help settle the debate over the extent to which stimulative monetary policy made the past couple of years so difficult.

Macklem’s efforts to get inflation back down will be graded more favourably. He took a risk and got aggressive, raising the benchmark interest rate a full percentage point at one policy meeting in July 2022—startling for a central bank that prefers to adjust borrowing costs a quarter point at a time. The target peaked at five per cent in July 2023, a jarring increase considering that 16 months earlier the rate was almost zero.

The strategy won Macklem little praise. Lana Payne, the head of Unifor, the country’s largest private sector union, accused him of waging a “class war” against workers. Some economists assumed the rate shock would cause a recession, as that’s what was required to end Canada’s last bout with high inflation in early 1980s.

Related Articles

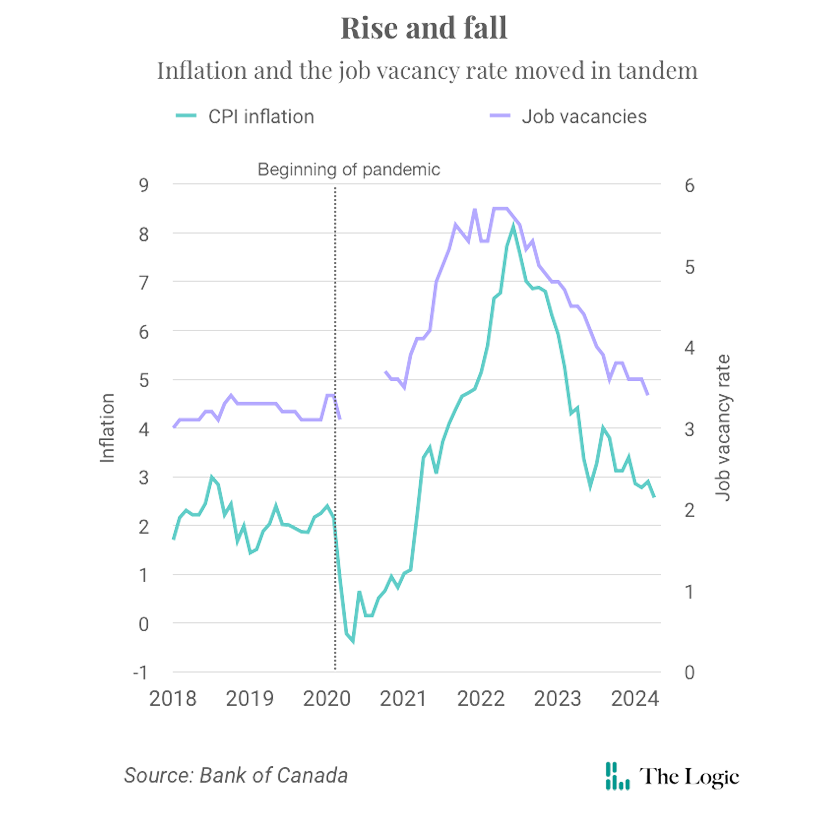

But it’s looking good now. Macklem bet employers would eliminate an unusually large number of unfilled positions before they resorted to mass layoffs, and so far he’s been right. The jobless rate was 6.2 per cent in May—higher than it’s been in a while, but still low by historical standards. Meanwhile, job vacancies have fallen to about 650,000 from a record of roughly 984,000 in the second quarter of 2022, according to Statistics Canada.

“This is the soft-landing scenario,” Macklem said in a speech this week. “It has always been a narrow path, and we have yet to fully stick the landing. But we continue to think that we don’t need a large rise in the unemployment rate to get inflation back to the two per cent target.”

Payne’s attacks displayed a misunderstanding of how the central bank figures labour market conditions into its decisions.

A desire to orchestrate a rapid recovery from the COVID crisis—and avoid a repeat of the protracted period of weakness that followed the Great Recession—likely contributed to the Bank of Canada’s decision to stay on an emergency footing for longer than was necessary. The central bank toyed with waiting until July to cut interest rates, but ultimately decided to err on the side of growth and go for it.

The U.S. Federal Reserve and the Reserve Bank of New Zealand have dual mandates that oblige them to set interest rates to achieve both price stability and maximum employment.

It’s different in Canada. The central bank’s marching orders from Prime Minister Justin Trudeau’s government are more nuanced. The primary objective is to keep inflation—as measured by year-over-year increases in the consumer price index—at around two per cent, the midpoint of a target range of one per cent to three per cent. When the Bank of Canada is confident inflation is subdued, it has instructions to probe the boundaries of full employment, or the highest level of employment the economy can sustain without stoking price pressures.

With inflation back in the central bank’s comfort zone, Macklem can devote extra attention to job creation.

There’s a link between hiring and inflation, so policymakers insist they are always attentive to what’s happening in the labour market. The governor’s latest speech was an update on how the central bank thinks about the unofficial part of its mandate. Along with humble-bragging about the soft landing, Macklem added nuance to how he and his deputies think about wage growth, and why the jobless rate could be masking weakness.

Wages are a sensitive issue for central banks: on an individual level, a pay raise is unambiguously good; at an aggregate level, a rate of growth that exceeds productivity is inherently inflationary, according to Bank of Canada’s best math. One argument against cutting interest rates is that wage growth still is around five per cent—and productivity is declining.

It might not be quite as simple as that. Macklem called wage growth a lagging indicator, so as long as that pressure keeps receding, the Bank of Canada appears ready to continue cutting rates. He also emphasized that composition matters: pay increases in productive industries are less of a worry than outsized gains in unproductive ones.

One innovation that gets too little attention is the way the Bank of Canada studies the labour market. Central banks once based their assessments primarily on the unemployment rate. Since 2021, the Bank of Canada has used a dashboard of indicators that provides a much more granular picture.

When inflation was surging to eight per cent, the dashboard was an afterthought: there was no doubt about whether interest rates needed to be higher or lower. But now that the decisions are less obvious, the dashboard is back in play.

Macklem observed that the unemployment rate of newcomers was 11.7 per cent in May, and that youth unemployment was 12.7 per cent.

“These workers are feeling the effects of slower growth more than others, and we need to recognize this,” Macklem said. “This matters for monetary policy because it indicates there is some slack in the labour market. That suggests the economy has room to grow and add more jobs without creating new inflationary pressures.”

All things equal, that suggests the Bank of Canada will cut interest rates again in July.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Justin Tang

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Commentary

Carmichael: The hard work of breaking down internal trade barriers is starting to pay off

Briefing

Cadillac Gold raises $385M in IPO

U.S. hits 60 countries, including Canada, with forced labour tariffs

U.S. Congress members propose an ‘AI kill switch’

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.