Most of those with skin in the game have positioned themselves for the Bank of Canada to cut interest rates on Wednesday, market pricing suggests.

Those who only have their reputations to worry about are less convinced. Three-quarters of roughly 30 forecasters surveyed by Reuters said they expect a cut. The C.D. Howe Institute’s monetary policy council of Bay Street and academic economists called on the central bank to drop the benchmark rate by a quarter point to 4.75 per cent.

You don’t need a complicated model to make a reasonable prediction of where interest rates are headed. “What is really important to us is that Canadians understand what we’re doing, why we’re doing it and that they understand that we’re thinking about them and that we have their best interests at heart when we make a decision,” senior deputy governor Carolyn Rogers told the Senate banking committee in May.

The Bank of Canada has been clear about what it will need to see to cut interest rates: inflation’s break towards the two per cent target earlier this year must be sustained. It has said it would make that call based on what it sees happening with core inflation, the balance of supply and demand, wage growth and corporate price behaviour. Let’s go through the checklist.

Tighter core: The Bank of Canada’s primary job is to keep year-over-year increases in inflation at the midpoint of a target range of one per cent to three per cent. Policymakers target two per cent, but this isn’t physics—nothing will break if inflation settles at 2.2 per cent or 1.8 per cent. Headline inflation dropped inside the Bank of Canada’s comfort zone in January and was at 2.7 per cent in April.

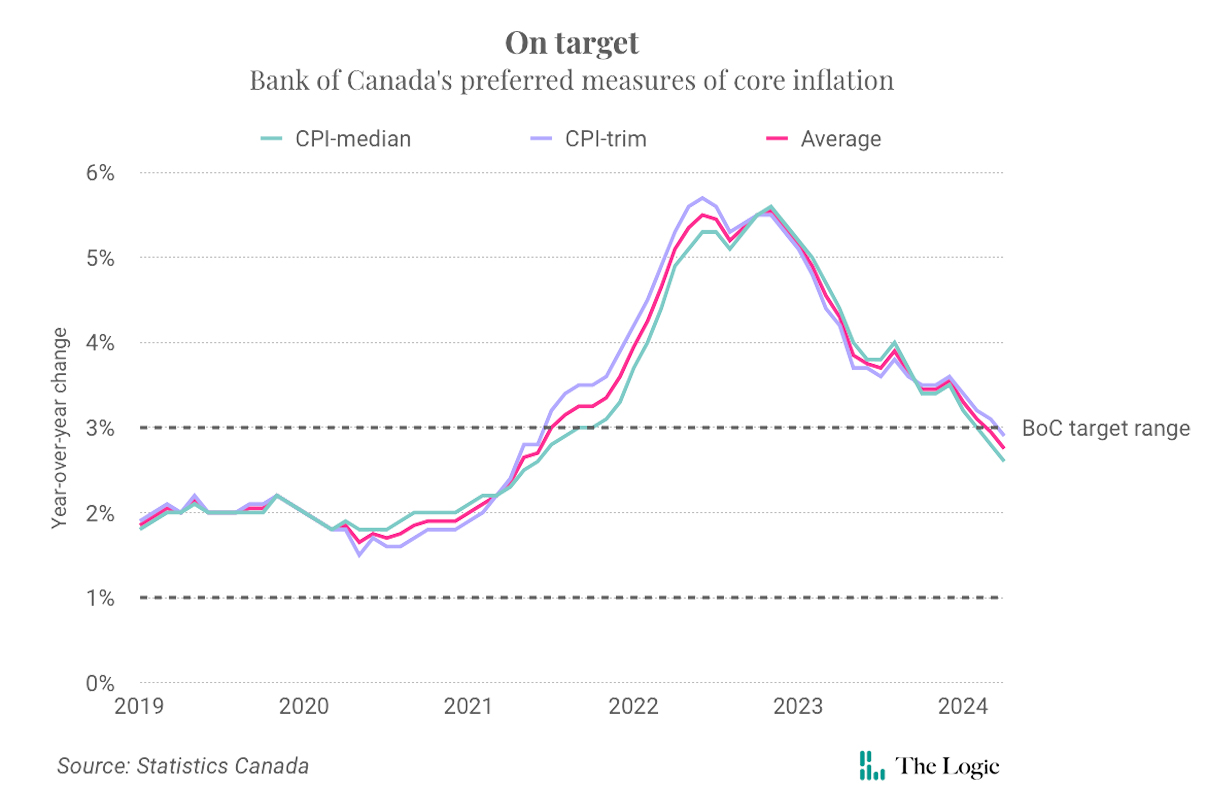

Lower energy prices accounted for much of the decline—just like they accounted for much of the initial surge. Volatile energy and food prices obscure the trend all the time. To get a truer read, central banks keep an eye on “core” measures that attempt to correct for volatility. The Bank of Canada’s two preferred gauges of core inflation averaged 3.3 per cent in January, 3.1 per cent in February, 2.95 per cent in March and 2.75 per cent in April.

The Bank of Canada used to measure core inflation by subtracting the eight most volatile items from the consumer price index and adjusting for changes in indirect taxes. That number dropped to 1.6 per cent in April from two per cent in March.

Conclusion: inflation is still a little high, but it’s clearly trending towards target.

Slowth: Statistics Canada reported on Friday that gross domestic product accelerated to an annual growth rate of 1.7 per cent in the first quarter. Some Bay Street analysts interpreted the tally as a sign of strength. Final domestic demand—which combines household consumption, government spending and private investment—surged to an annual rate of 2.9 per cent, the fastest since the start of 2022. The jump in business investment is positive. The economy is pushing through the headwinds of higher prices and higher interest rates.

But the economy is labouring. Revisions showed that the economy stagnated in the fourth quarter, and the rebound was considerably weaker than the Bank of Canada’s growth forecast of 2.8 per cent in the first quarter. What’s more, the central bank estimates output could grow 2.5 per cent this year without causing inflation, and the unemployment rate has climbed above six per cent for the first time since the winter of 2021.

Conclusion: suppliers would welcome more demand.

Business decisions: Corporate pricing behaviour might never go back to normal. The combination of data and technology allows companies to change prices far more quickly and precisely than they could in the past. The Bank of Canada reckons that dynamic pricing contributed to inflation by making it easier to protect profit margins amid surging input costs. The central bank also said in its latest quarterly report on the economy that it thinks pricing practices are “normalizing.” Higher prices eventually destroy demand. Fewer firms were planning unusually large or frequent price changes over the next 12 months, according to the Bank of Canada’s latest quarterly business outlook survey.

Wages might be the trickiest obstacle on the path to lower interest rates. Wage growth now exceeds inflation, helping households recover from the initial post-pandemic price shock. Yet higher wages contribute to inflation by raising the cost of supplying goods and services, and by increasing spending and therefore demand. Various indicators suggest pay is around four per cent higher than a year ago. That’s inconsistent with inflation of two per cent, yet down from rates of around five per cent not long ago.

Tiff Macklem, governor of the Bank of Canada, in Ottawa in May 2024. Photo: The Canadian Press/Justin Tang

The Canadian Federation of Independent Business’s latest monthly survey said smaller companies expected wages to rise 2.8 per cent over the next 12 months, down from 3.6 per cent in June 2022 but still faster than the historical average of 1.9 per cent.

Conclusion: corporate pricing and wages probably aren’t barriers to an initial rate cut, but they could offer resistance to additional cuts.

Bottom line: The arguments against cutting interest rates this week tend to be of the better-safe-than-sorry variety. Inflation dipped below three per cent in June 2023, then surged back to four per cent. In other words, don’t get fooled again.

One important difference is that the economy still had a lot of momentum a year ago. It has considerably less now: growth is below potential, the unemployment rate is drifting higher and the job vacancy rate is back at 2019 levels. Most importantly, core inflation is back around the two per cent target. The door is open for a rate cut. If governor Tiff Macklem opts against walking through, it will be because of an overabundance of caution.