Canadian venture capitalists are bracing for the unknown in 2024. After two years of what felt like unrelenting black swan events—from COVID-19 to Russia’s war in Ukraine, to Silicon Valley Bank’s collapse—they’ve learned that predicting the market is a fool’s errand. “Everything we’ve learned over the last few years is: expect the unexpected,” said Michael Yang, head of venture capital at OMERS Ventures.

Skip to content

Special Report

VC Outlook 2024: What 6 Canadian venture capital investors expect from the year ahead

‘More and more companies are winding down and going out of business, and we should expect that to increase into ‘24’

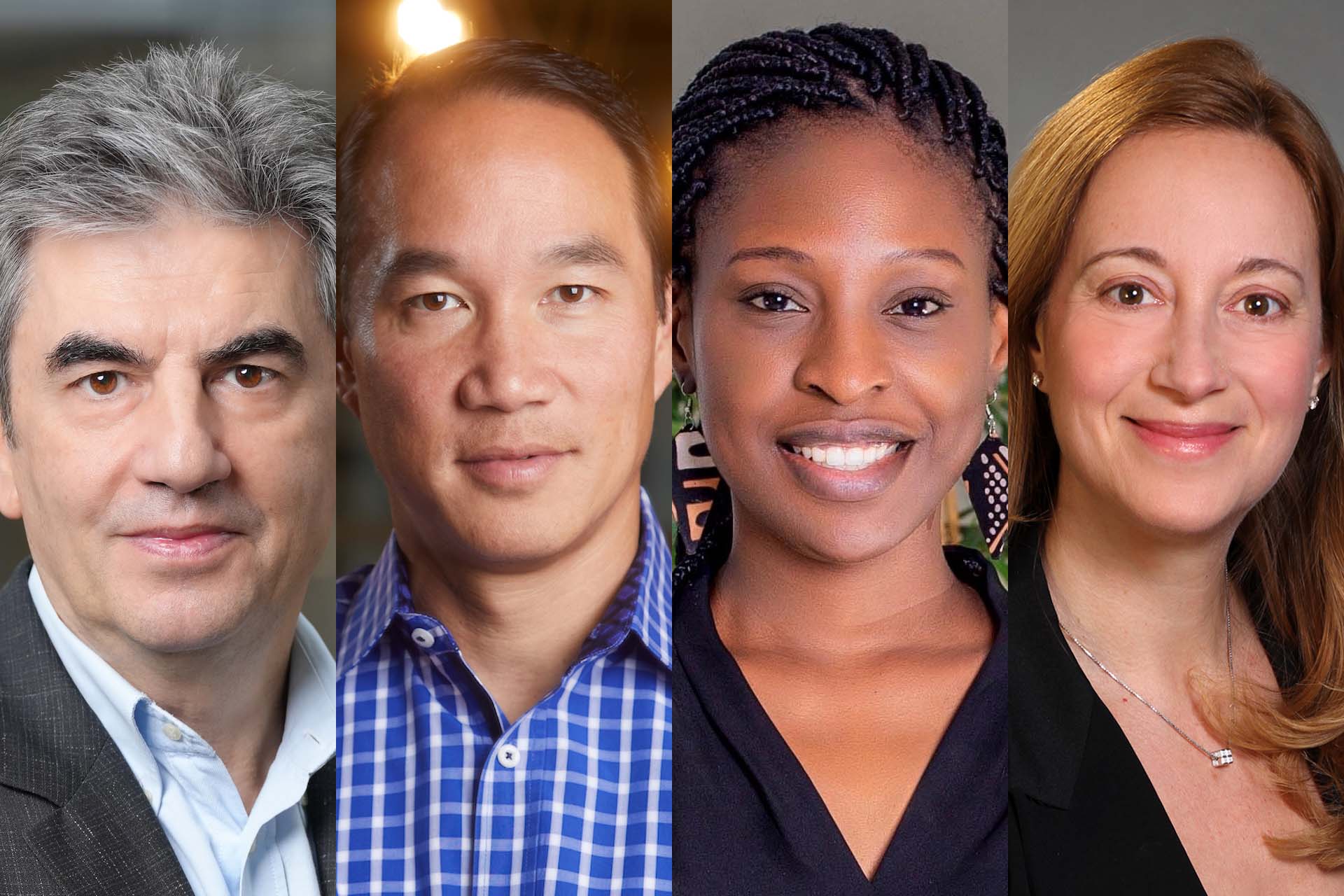

From left to right: Emil Savov, managing director of the MaRS Investment Accelerator Fund; Michael Yang, head of venture capital at OMERS Ventures; Lise Birikundavyi, managing partner at BKR Capital; and Senia Rapisarda, managing director at HarbourVest. Photo: Handouts

Canadian venture capitalists are bracing for the unknown in 2024. After two years of what felt like unrelenting black swan events—from COVID-19 to Russia’s war in Ukraine, to Silicon Valley Bank’s collapse—they’ve learned that predicting the market is a fool’s errand. “Everything we’ve learned over the last few years is: expect the unexpected,” said Michael Yang, head of venture capital at OMERS Ventures.

A major unknown hanging over the venture capital market is where interest rates will go. While economists expect U.S. and Canadian central banks to start lowering rates in 2024, it’s hard to predict how quickly they’ll do so, or whether consumer confidence and investor liquidity—two key factors on the VC market—will bounce back. “The entire environment leads people to be more cautious because it’s unpredictable,” said Kim Furlong, CEO of the Canadian Venture Capital & Private Equity Association.

Talking Points

- Investors in Canada’s venture capital ecosystem say startups should expect another challenging fundraising year

- While deal volumes may increase as startups that delayed fundraising return to the market, investors are only interested in capital efficient companies with a clear path to profitability

The Logic spoke with six investors across Canada’s VC landscape about what next year could look like—from hot sectors, to exit strategies and why the next cohort of startups will be an investor’s dream. With the caveat that anything can happen, here’s what to expect in 2024:

Artificial intelligence was a glaring outlier in an otherwise slow year for VC funding. As of Dec. 14, Canadian companies in the sector raised close to US$1.5 billion of the roughly US$8.5 billion—or about 17 per cent—in total venture capital dollars invested this year, according to PitchBook data.

Investors likely won’t lose interest in 2024. “It’s becoming obvious that it’s a vital area for almost every aspect of business,” said Emil Savov, managing director of the MaRS Investment Accelerator Fund.

Part of AI’s appeal to investors is it can make businesses more efficient at a time when companies are desperate to cut costs, said Christopher Gillam, vice-president of operations and strategy at BDC Capital.

Furlong said the CVCA is watching closely for forthcoming AI legislation, which will set rules for making and using “high-impact” AI applications. Furlong has urged the government to ensure those rules don’t disincentivize AI companies from doing business in Canada. “We understand that there’s risk,” she said, “We just want [regulations] to be interoperable—whatever’s happening in the U.S. is equal to what’s happening in Canada.”

Related Articles

Savov said to expect more scrutiny, however, of companies’ AI promises. Simply building a tool on top of open-sourced technology available to anybody isn’t enough, he said. “If you’re a developer, you better have something that adds value and some intellectual property.”

Other sectors to watch

Government stimulus for cleantech in the U.S. and Canada could coax more investors into the space, which many generalist investors have avoided until recently because companies in the sector tend to require lots of money and come with big risks.

Cybersecurity is another area investors are eyeing in 2024, as the surge in cyberattacks creates a market opportunity for companies trying to address the problem.

And while Furlong said life sciences is a “curveball,” she and other investors predict the sector could be hot in 2024, buoyed by deals like Denmark-based Novo Nordisk’s US$1.1 billion acquisition by Montreal’s Inversago Pharma. “There’s been some good exits this year, so [investors] may stay the course,” said Furlong.

The end of the bridge round

Inventors have been floating their portfolio companies with quiet inside rounds since the market took a turn in late 2022. The strategy was meant to give startups—many of which saw their pandemic-era valuations drop—enough cash to hold them over until investor interest and valuations returned.

But the market has had a slow recovery, and likely won’t return to 2021 activity levels anytime soon, several investors told The Logic. That means founders need to readjust expectations. “The time for triaging is done,” said Yang. “Either you believe the founder and the company are going to make it or you don’t.”

Many companies that delayed fundraising in hopes of better investment conditions have run the clock and will have no choice but to go back to the market to fundraise in 2024, said Senia Rapisarda, managing director at HarbourVest. That will create a glut of funding options for VCs. “We’re prepared for a ton of companies to come to the market next year,” said Yang. “A tsunami of more volume will hit and then the question is, within that volume, will the quality uptick?”

Investors—some of whom were burned by the pandemic hype cycle—are cautious going into 2024, however. Rapisarda said she’s focused on “quality” companies that are either profitable or close to it, and VCs are mindful not to overpay for deals, like they might have two years ago.

Sluggish fundraising for new venture funds

Relatively few Canadian companies have exited through initial public offerings or mergers and acquisitions over the past two years. That has left venture funds with little money to return to their limited partners (LPs), the investors that fund VCs, said Rapisarda. “In the Canadian market, LPs would have received less liquidity so far, and therefore are less inclined to invest in the next fund,” she said.

The meagre returns could make LPs reluctant to invest in funds they aren’t familiar with. Rapisarda predicted that “2024, for first-time funds and emerging managers, is going to be very difficult to fundraise,” and offered a bit of advice: “If you have a great idea, a great strategy, join forces with an existing fund.”

Investors could see some delayed liquidity through M&A or secondary transactions, in which VCs sell all or a portion of their stake in a startup to another investor. Many market-watchers had predicted a busy M&A market in 2023, but that didn’t quite happen.

Furlong said companies should now be coming to terms with what the market is willing to pay to purchase them, which could trigger an M&A surge in 2024.

More company failures

For startups that can’t raise new money and aren’t good M&A candidates, it could be time to close shop. “You’re going to see more company failures,” said Gillam. “If it ends up being a more protracted, middling environment, people won’t have the same enthusiasm to continue supporting second-tier companies.”

Yang sees plenty of scenarios in which companies who can’t raise money fail. He predicts the M&A market will stay slow, as prospective buyers conserve cash. “What other startup are you going to try to buy or merge with? They’re also burning money,” he said. “More and more companies are winding down and going out of business, and we should expect that to increase into ‘24.”

BKR Capital managing partner Lise Birikundavyi said her firm pared down the number of investments it was planning to make through its first fund, which it aims to finish deploying next year. But what investors have lost in deal quantity, she said, they’re making up in quality. “There’s this feeling that the market is getting cleaner,” she said. “As much as we like to have a very active market, there’s an aspect of it that has been refreshing, because we know that strong companies will prevail in this market.”

Rapisarda expects more business strategies that rely on less outside funding. Being “incredibly capital efficient with a clear path to profitability” is a must-have, she said. “If this is the last [funding] round, can the company make it?”

Yang, meanwhile, said startups that launch while capital is scarce have the right mentality for a scrupulous investment environment. “Vintage ‘24, and even some parts of the vintage ‘23, companies that started in these years, they are going to be great, “ he said, “because they just have the right mindset.”

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: Handouts

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

News

Carney says trade talks to heat up after Trump’s latest tariff threats

Briefing

Sleep Country plots U.S. expansion after winning bid to buy hundreds of Sleep Number stores

Horizon Aircraft sells 5 vertical takeoff planes to Australia’s V-Star, with more on order

Bombardier shares hit highest level in 24 years after deal with Saudi firm

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.