As Shopify closes in on another record year for revenue, one part of the e-commerce giant’s business in particular is emerging as a big new source of growth: lending money.

Through Shopify Capital, the Ottawa-founded firm has been providing its merchants with quick access to cash in ever-greater totals, forging further into an arena otherwise served by legacy banks and fintechs.

Talking Points

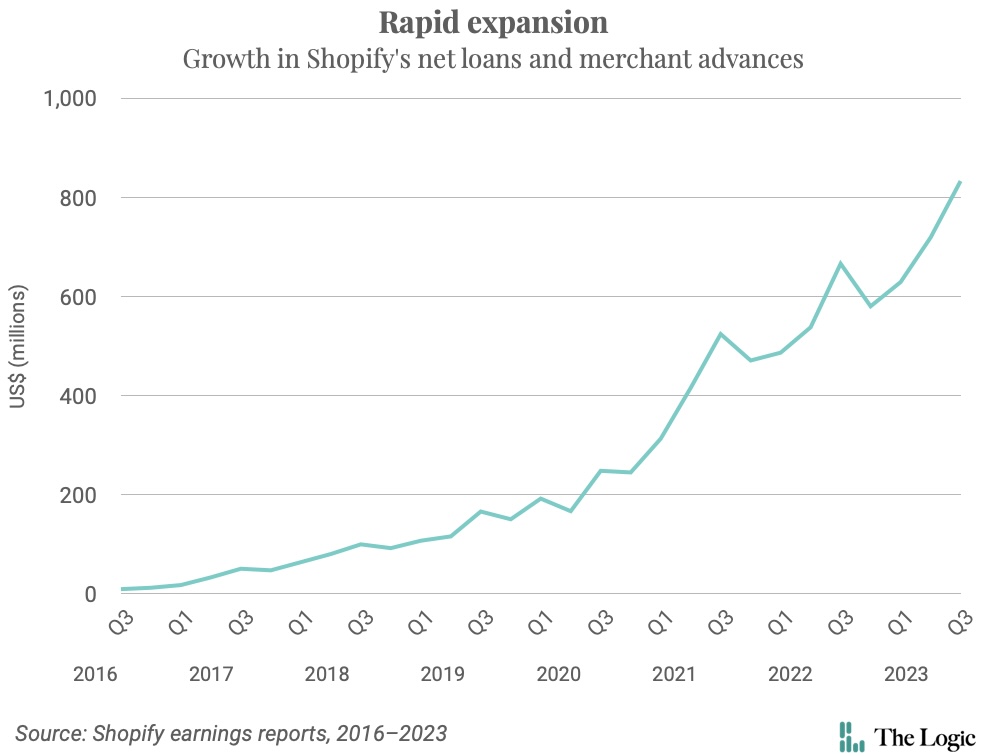

- Launched in 2016, Shopify Capital has since extended more than US$5.1 billion in loans and cash advances to merchants in the U.S., Canada, Australia and the U.K.

- E-commerce entrepreneurs who may struggle to secure traditional financing have been drawn to the service, which offers easier access to cash with repayment tied to a store’s daily sales, and Shopify believes it is uniquely positioned to make good bets on who to offer capital thanks to its plethora of data

Shopify Capital has extended more than US$5.1 billion in cash advances and loans to entrepreneurs that use its e-commerce platform. It reported US$833 million outstanding on its balance sheet in its most recent quarter—a more than 9,000 per cent increase since the program started in 2016.

The heightened pace of lending reflects Shopify’s strategy of leveraging its insight into merchants’ businesses to serve more and more of their needs. So far, the program has served their mutual self-interest. Sellers who need extra cushion in today’s tougher economic environment, or who struggle to secure financing from traditional sources, get much-needed credit. Meanwhile, Shopify’s trove of data helps it make good bets on whom to lend to, and how much, boosting its bottom line as its clients grow their shops.

“They’re kind of best positioned to be able to offer merchants this kind of funding at arguably a lower risk profile,” said Ken Wong, managing director and senior analyst at the brokerage and investment bank Oppenheimer.

Though the firm doesn’t break out how much revenue it earns from Shopify Capital, Wong believes it’s become the second-biggest driver of its merchant solutions segment, which accounts for 72 per cent of Shopify’s overall revenue.

Shopify Capital started as a pilot program before becoming a permanent fixture that at first only offered cash advances to U.S. merchants. It expanded the service to the U.K. and Canada in early 2020, and to Australia in 2022. In 2020, Shopify first made loans available, which merchants in the U.S. and Australia are now eligible to receive.

The two forms of credit work in similar fashion. Shopify pre-approves a merchant for up to US$5 million and sends an offer that typically includes three amounts for the vendor to choose from with separate repayment terms

For merchants who need cash on short notice, or who can’t meet the terms of traditional lenders, the service has been a lifeline. Kyle Goldstein has used Shopify for his Texas-based store Lone Star Casket, which sells coffins online, since he started it about four years ago. Shortly after he launched, Shopify sent notification that he qualified for a loan. The process was “super easy, like three clicks, and I think it was within 48 hours the money was in my bank account,” he said. He used his first loan, US$17,000, to purchase a delivery van and a second to weather a dry spell.

Goldstein had never formally applied for a business loan from a bank, because the process discouraged him. The requirements were stricter—he’d have to have been selling caskets for at least three years—and they wanted “pages and pages” of information, he said.

Banks also charge compound interest, while Shopify does not. Merchants agree to take out a principal amount and an interest sum is added to that up front. Shopify then takes a predetermined percentage of the merchant’s daily sales until they’ve repaid the total amount.

Shopify declined to say what interest rates it charges. But the platform is currently offering Goldstein a third loan. The highest of three options is a US$13,000 principal with US$1,690 in interest, or 13 per cent, and a daily sales remittance rate of 17 per cent to pay it off. If he accepts the lowest amount, US$7,800, he would pay US$624 in interest, suggesting an eight per cent rate. Shopify would take 10 per cent of his daily sales as repayment.

For some merchants, though, accessing the money is less of a challenge than managing cash flow as Shopify takes a cut of every sale as repayment. Martin Casas, who co-owns Apotheosis Comics & Lounge, a St. Louis store that also sells its wares online, said he thought his company got “a fair shake” with the interest on its three loans. But the amounts Shopify withdrew varied widely, he said: one day it might take US$25; the next US$600. Casas found it difficult to stay on top of the transactions and ensure he had enough funds for other bills or withdrawals.

Mark Poppen, owner of Funky Moose Records, an online store based in Prince Albert, Sask., has used Shopify Capital several times. His advice: ensure your profit margin is higher than that of the daily sales Shopify will take. He once selected a larger loan that commanded a higher daily sales cut. “That was a little bit tight on the profit margins,” he said.

Poppen, who describes himself as debt-averse, warned there’s such a thing as funds that are too easy to access. He turned to Shopify Capital after taking a similar offering from Clearco because Shopify’s process was simpler. Still, he hasn’t accepted every offer presented. “We didn’t really need the extra money,” he said, “and cash flow was good so we didn’t want to have an extra daily burden on expenses.”

For Shopify, as for merchants, there are hazards, though. Lending money to small business owners is risky, especially in a high-interest-rate environment, said Jonathan Aikman, an adjunct faculty member in finance at the Smith School of Business at Queen’s University. He pointed to a recent spike in insolvencies, and warned that more businesses will experience financial troubles—many more, in the event of a significant downturn.

Shopify mitigates some of that risk through the use of machine-learning algorithms that consider millions of internal data points in determining Capital offers. And tying repayment to sales reduces the likelihood of default by removing the pressure of rigid payment timelines on merchants, said company spokesperson Jackie Warren.

Shopify carries an insurance policy from Export Development Canada to protect it from risk associated with its merchant credit business, according to financial disclosures. It also partners with banks to serve as loan providers, said Warren. (Webbank is currently its partner in the U.S.)

Whether the company will keep growing its lending business in the event of an economic downturn is an open question. Wong expects loans to rise in tandem with the overall business, and for Shopify to extend the offering to more of the 23 countries where its payments service is available. (Warren said Shopify has no expansion details to share at this time.)

One of those countries is Finland, where Jordan Lockhart lives. Back in 2016, he ran his own Shopify-powered store out of New York, selling decorative leather table mats, and used a loan from the company to purchase more inventory. But Shopify’s capital service isn’t available in Tampere, Finland, where he now manages Kamerastore, a shop that sells used cameras. He finds it difficult to secure traditional financing because banks place low value on the store’s secondhand inventory, and without more money to purchase more stock, it’s hard to grow the business.

“If we could have Shopify Capital at the company I’m working at now,” he said, “I think we would be interested in, like, $50,000 to $100,000 a month.”