Skip to content

Analysis

Millions of Canadians were bracing for a mortgage shock that never happened

Falling interest rates, savings and flexible terms have softened the blow even as higher monthly payments continue to squeeze household finances

About 60 per cent of Canadians renewing their mortgages in 2025 and 2026 are expected to face higher monthly payments. Most of these borrowers hold five-year, fixed-rate mortgages, per Bank of Canada data. Photo: The Canadian Press/Evan Buhler

Millions of Canadians were expected to face steep payment increases when renewing their mortgages this year. Instead, the impact has been more muted than many had feared. While economists say falling interest rates, rising household wealth and lender flexibility have helped soften the blow, even small increases could continue to strain household finances.

Bank of Canada data from July shows roughly 60 per cent of mortgage holders renewing in 2025 and 2026 are expected to see payments rise. About three-quarters of those borrowers hold five-year, fixed-rate mortgages. Much of the earlier anxiety around renewals focused on this group, which locked in ultra-low rates during the pandemic.

Talking Points

- Roughly 60 per cent of Canadians renewing mortgages in 2025 and 2026 are expected to see higher monthly payments, with about three-quarters of those borrowers holding five-year, fixed-rate mortgages, according to the latest Bank of Canada data from July

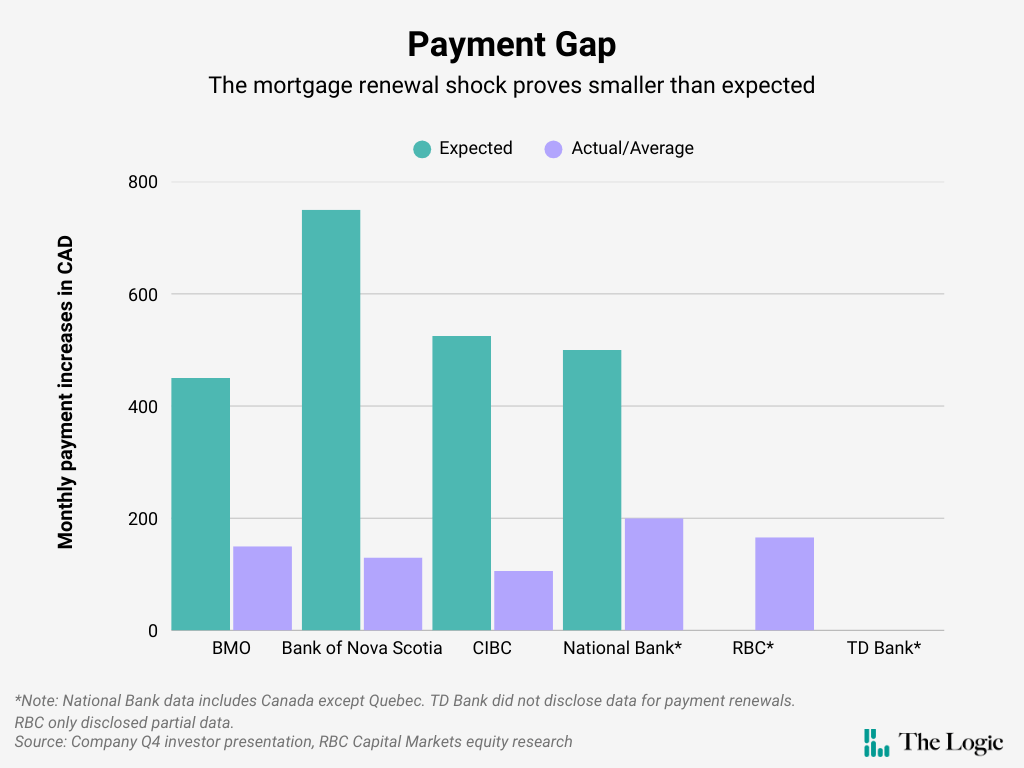

- Approximately $420 billion in mortgages are set to renew this year at lower monthly payment increases than once feared. Fourth-quarter reports from Royal Bank of Canada, CIBC, Scotiabank, Bank of Montreal and National Bank show increases closer to $106 to $200 a month, well below earlier projections

But Robert Kavcic, a senior economist at Bank of Montreal, said those warnings were driven by “excessive fear.” Five-year fixed-rate loans now account for only about 27 per cent of the mortgage market in 2025, according to BMO research.

“I don’t want to downplay it; a lot of households are going to see mortgage payment increases,” Kavcic said in an interview. “But it’s not going to be a shock that creates a big wave of delinquencies or selling.”

The latest quarterly reports from Canada’s five largest banks show that more than $420 billion in mortgages are set to renew this year. For five of Canada’s six largest banks, monthly payment increases are closer to $106 to $200 a month, well below earlier projections.

A key reason, Kavcic said, has been falling interest rates, which fell to 2.25 per cent by the end of 2025 from 5 per cent in 2023. Borrowers who locked in ultra-low rates were also stress-tested for higher payments, he added.

Maria Solovieva, an economist at TD Bank, said that banks were also proactive, contacting borrowers ahead of renewals to explain options, encourage prepayments and extend repayment periods.

According to John Aiken, a senior analyst at Jefferies, this flexibility stems from the banking system’s oligopolistic nature, which—despite its drawbacks—provides stability and lets banks manage their customer base.

Related Articles

The renewal wave, which represents about 90 per cent of outstanding mortgages, has been manageable and has even supported banks’ net interest margins, RBC Capital Markets analyst Darko Mihelic wrote in a note to clients. With concerns about a renewal shock fading, the focus has shifted to competition between lenders, he wrote.

Similarly, Aiken said intensified competition could prompt banks to cut prices to attract customers. Which banks’ margins benefit, he said, will depend on who leads the cuts and how rivals respond. BMO and CIBC have historically moved first, while National Bank and RBC may be less inclined given their recent acquisitions, he said.

Asked about potential competition between lenders and the possibility of price cuts, CIBC spokesperson Tom Wallis said in an emailed statement that the bank’s “long-standing approach” is to contact clients before renewal so they understand all their options, noting the current rate environment is different and “it’s important that homeowners consider their total financial picture.”

Scotiabank and BMO referred questions to the Canadian Bankers Association (CBA), though BMO said it has taken a “proactive approach” by engaging customers early and offering education and support. CBA spokesperson Ethan Teclu said borrowers are “well served by a very competitive market underpinned by a prudent banking sector.” RBC, National Bank and TD Bank did not respond to requests for comment.

The bigger risk for lenders isn’t monthly payment increases but the Big Six’s limited diversification outside Canada, Aiken said. He said that CIBC and National Bank, despite their smaller housing market share, are more exposed because Canadian residential mortgages make up a larger portion of their overall revenues, adding that National’s exposure is partly offset by stronger housing conditions in Quebec.

When asked about the risks their concentrated portfolios could have on their revenues, National Bank and CIBC declined to comment.

Economists told The Logic many homeowners are entering this year’s renewals in a stronger position than five years ago, buoyed by income growth, rising home equity and market gains. Gains, however, are uneven, Solovieva warned, leaving younger households and non-owners more exposed.

“Overall, there is still financial wealth that is higher than the pre-pandemic [era],” Solovieva said. “So even those who are potentially renewing could make prepayments by tapping into this liquidity as well.”

But for many Canadians, financial strain is emerging elsewhere. The national 90-day plus non-mortgage delinquency rate rose to 1.63 per cent, up 14 per cent year over year, according to Equifax’s third-quarter market pulse report.

“Mortgage payment shock is still contributing to rising missed payments on credit cards, personal loans and even on mortgages themselves,” wrote Rebecca Oakes, vice-president of advanced analytics at Equifax Canada.

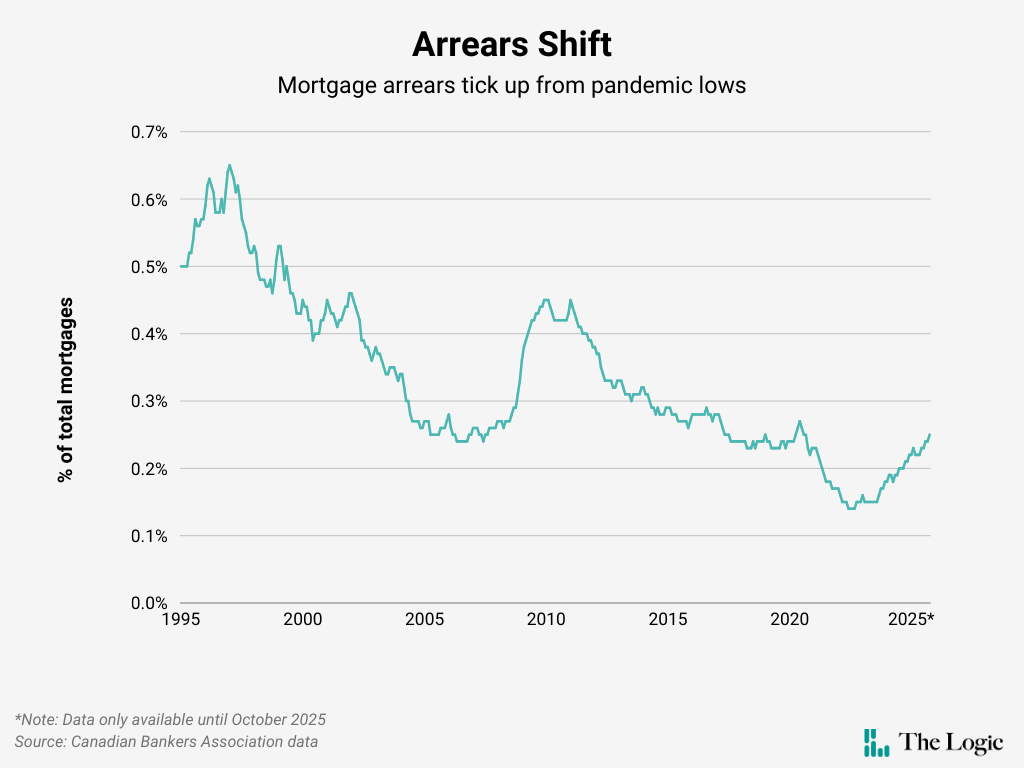

Mortgage arrears—the share of loans overdue by three months or more—remain low by historical standards. But data from the CBA show the rate rose to 0.25 per cent in October, returning to pandemic-era levels.

Higher monthly mortgage payments are also rippling through the economy and diverting money away from areas such as consumer goods, restaurants and travel, Kavcic said.

While acknowledging that many households are facing higher costs, the Office of the Superintendent of Financial Institutions’ spokesperson Cory Harding said in a statement that “Canada’s financial system is well positioned to navigate this period of elevated but stable debt servicing.”

Looking ahead, experts do not expect lower monthly mortgage payments to defer credit risk or trigger another renewal cliff. As long as borrowers remain employed and have home equity, the mortgage situation should stay stable, Kavcic said.

“We did see quite a significant slowdown in spending. We don’t think that this particular acceleration will lead to a sizable impact on the economy,” said Solovieva. She expects renewals to pick up modestly in the first half of 2026, before returning to more typical levels.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Evan Buhler

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Special Report

Meet Canada’s leading innovators from the Class of 2026

Briefing

Ksi Lisims LNG signs ‘first-of-its-kind’ deal to supply Germany’s state-owned Uniper

Brookfield and NextEra to build a US$100B data-centre campus in Kentucky

Extropic gets US$75M from U.S. government for more efficient chips

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.