Some call it the “mortgage cliff.” You might also hear of it referred to as the “renewal shock.” Over the next three years, millions of mortgages will reset at higher rates. Many on Bay Street and Parliament Hill think it could go badly.

Skip to content

Commentary

Carmichael: Mortgage renewals causing widespread fear

Fixed rate mortgages are coming due, what will the impact be on Canadians?

Mt. Rundle rises behind homes being constructed in Canmore, Alta., in April 2023. Photo: The Canadian Press/Jeff McIntosh

Some call it the “mortgage cliff.” You might also hear of it referred to as the “renewal shock.” Over the next three years, millions of mortgages will reset at higher rates. Many on Bay Street and Parliament Hill think it could go badly.

“The macroeconomic math related to Canada’s looming wall of mortgage renewals should be terrifying for the Bank of Canada,” Dylan Smith, an economist at David Rosenberg’s advisory firm, wrote in November. It was another brick in the wall of worry over what will happen to the economy when the fixed-rate mortgages of five years ago, when the benchmark interest rate was close to zero, reset at rates based on the current five per cent.

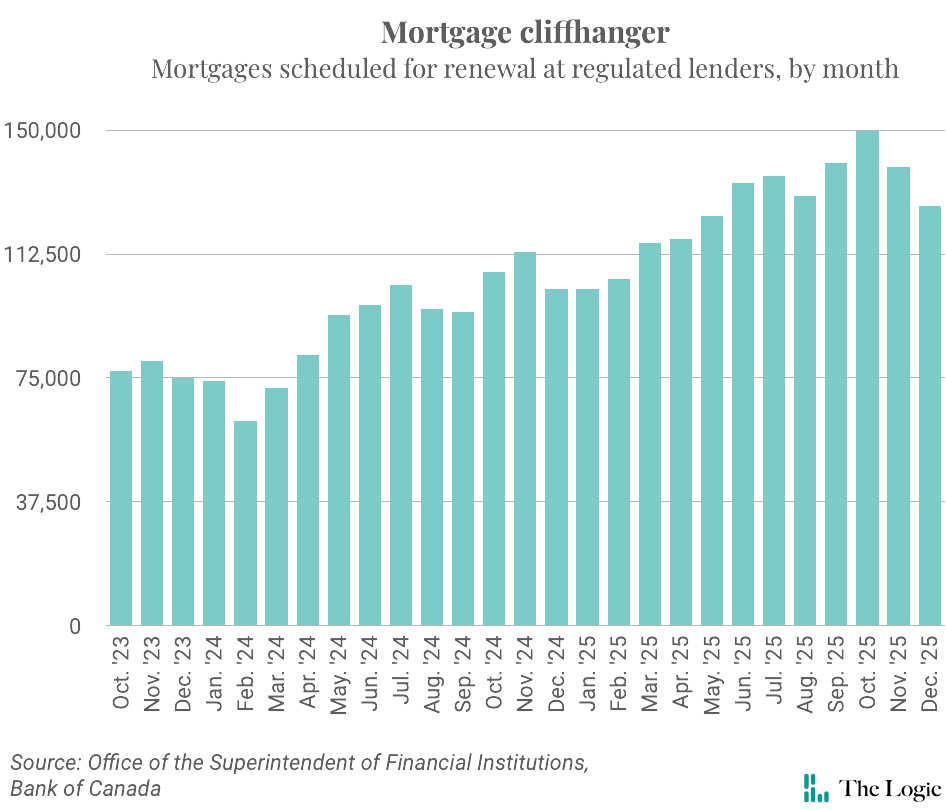

When Bank of Canada governor Tiff Macklem appeared at the House of Commons finance committee at the end of October, the first question he was asked, by Conservative finance critic Jasraj Singh Hallan, was whether he could provide a monthly breakdown of mortgages set for renewal through the end of 2025. “There’s a lot of anxiety around that,” Jordan Leichnitz, a former New Democratic Party adviser, said on the latest edition of the “Curse of Politics” podcast. “That feeling is going to move a lot of stuff for voters this year in Canada.”

The whispers of dread echo beyond the committee rooms and opposition offices. The Financial Consumer Agency of Canada issued updated guidance on what it expects federally regulated banks to do for consumers who are experiencing “exceptional circumstances,” including the “current combined effects of high household indebtedness, the rapid increases in interest rates and the increased cost of living.”

Related Articles

Finance Minister Chrystia Freeland’s fall economic statement introduced the Canadian Mortgage Charter, which was actually more of a digest, since it has no legal heft. However, it did assemble in one place all the options that homeowners have available to them if they feel they can no longer keep up with mortgage payments.

“The charter is one of the most important things that we’re putting forward today,” Freeland said at a press conference before tabling her fiscal update on Nov. 21. “I really recognize that with interest rates having gone up very quickly, there are many, many Canadians who are concerned about their mortgages going up.”

Anyone familiar with the Great Recession will understand the concern over housing. Cheap debt (and a material amount of fraud) created a housing bubble in the United States, which popped when the Federal Reserve raised interest rates to subdue inflation. Demand slowed as consumers struggled to manage higher mortgage rates. Some of the world’s biggest banks collapsed because their pile of financial assets tied to mortgages was suddenly worthless. The global financial system froze, precipitating the biggest economic collapse since the Great Depression.

So it makes lots of sense to stay on top of what’s happening in the housing market. That includes putting excessive emphasis on a doomsday narrative that ends up taking on a life of its own. Mortgage resets represent a risk to economic growth because hundreds of thousands of households will have less money to spend on discretionary purchases. But it’s unclear whether the Bank of Canada or anyone else should be “terrified.” The people who issued most of that debt aren’t overly worried.

In fact, they don’t seem particularly worried at all.

“Consumers are … handling that payment shock quite well,” RBC chief executive Dave McKay said at the annual RBC Capital Markets Canadian Bank CEO conference on Jan. 9. The heads of TD Bank, BMO, Scotiabank and CIBC all made similar comments.

In fact, most resets on existing fixed-rate mortgages will occur in 2025 and 2026. McKay said 2024 will be a relatively “light” year at RBC, with about 14 per cent of the bank’s fixed-rate mortgages scheduled to reset this year, compared with 25 per cent in 2025 and over 30 per cent in 2026.

Scotiabank chief executive Scott Thomson shared a similar renewal profile: 11 per cent in 2024, 22 per cent in 2025 and 35 per cent in 2026. Like McKay, he expressed little concern about defaults, noting that clients with variable-rate mortgages have been finding ways to make it work. “We’ve actually seen our clients navigate through that issue pretty well,” Thomson said when asked about the renewals.

Note Thomson’s choice of verb: “navigate.” The chilling warnings about mortgage cliffs tend to assume that homeowners are powerless actors in a story from the Old Testament. That frame makes for a better parable, but that’s not what happens in real life. Debtors engage with their creditors to stay solvent. They update their savings strategies: Dodig said CIBC clients have more money in their bank accounts today than they did before the pandemic. They also secure raises, something that’s been relatively easy to do over the past couple of years: the average hourly wage was about 20 per cent higher at the end of 2023 compared with the same point in 2019.

Thomson said Scotiabank clients that renew at current rates end up paying between $400 and $500 more per month. CIBC’s Victor Dodig put the figure at $300 to $700. McKay said the figure was about $400 per month at RBC, representing an increase of about 25 per cent, which he said matches the increase in household income since 2019.

That’s real money for a lot of households and that’s one of the reasons the economy could slide into a recession this year. But as long as the labour market holds up, most mortgage holders will be able to adjust. And then by 2025, interest rates will have started to fall, assuming Macklem makes good on his guidance from the end of 2023.

Be wary of where we’re headed. But don’t be afraid.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Jeff McIntosh

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Analysis

These AI startups are making millions with tiny teams

Briefing

Supply-chain management vendor Kinaxis reports revenue jump and higher profit

Flush with cash, Suncor Energy boosts share buybacks—but doesn’t rule out production growth

Goodfood seeks creditor protection as it tries to sell itself

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.