Listen Now

0:00

Canada’s great fortune since Confederation is that it has faced serious danger only twice. Memories of the first occasion are beginning to fade. I knew Hitler’s U-boats were present in Canadian waters during the Second World War, but I had either forgotten or never learned that German submarines sank two warships and some 20 supply ships in the St. Lawrence River in 1942.

Memories of the second serious threat are being consciously blocked, judging by the lack of interest in doing a proper post-mortem of the COVID-19 pandemic, which killed nearly 61,000 Canadians.

Related Articles

Those world-changing events—the Second World War, which ended in 1945, and the COVID-19 pandemic, which ended in 2023—track Canada’s rise and fall as a nation that can take care of itself.

At the Canadian Museum of History in Gatineau, Que., there’s a small homage to the exploits of Canadian Car and Foundry Company, which built more than 2,000 warplanes on commission for the Canadian and British air forces and the U.S. Navy at a plant in present-day Thunder Bay, Ont. Contrast that with the Canada that confronted COVID-19. Justin Trudeau’s government discovered there were no Canadian factories capable of producing the mRNA vaccines that ultimately beat the virus. A royal commission on the pandemic would have much to consider, but one question surely would be how an advanced economy stumbled so badly.

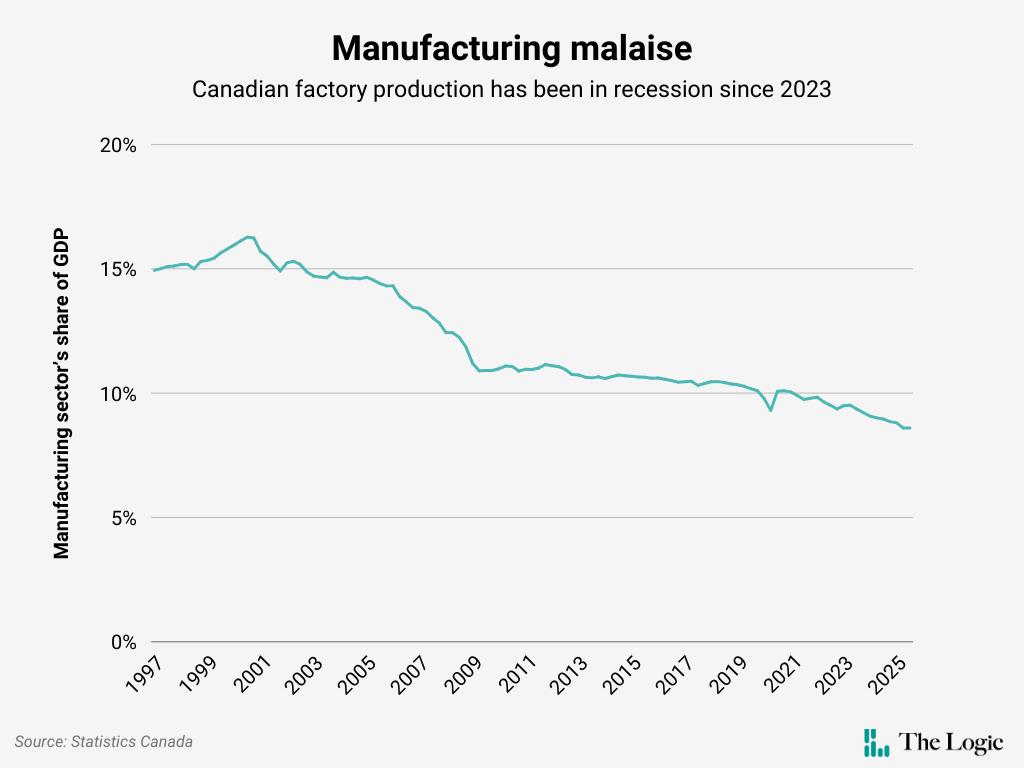

Canada’s inability to make cutting-edge drugs on command was an omen. National Bank chief economist Stéfane Marion has been documenting the “manufacturing recession,” observing in his most recent note on the subject that factory production’s share of gross domestic product has declined to 8.3 per cent, the lowest on record.

What happened? That’s a big question. The shift of North American automobile manufacturing to Mexico and the southern U.S. is part of the answer. But global forces only partially explain the erosion. Borrowing from Marion, it’s “indefensible” that a country with preferential access to 1.5 billion consumers through a network of trade agreements has failed to preserve its manufacturing base. A significant part of Canada’s problem is internal.

Constant uncertainty over the future of the North American trade agreement is an obvious headwind, but like globalization, it’s also an excuse. When you notice signs of erosion, you should reinforce your foundation to deter its long-term effects. Canadian policy in recent years has done the opposite. Marion blames “domestic policy failures,” including “excessive regulation” and the volatile politics around energy policy. Natural gas and electricity prices are critical industrial inputs, and the federal government and the provinces have been sending all kinds of mixed signals on how they intend to tax them.

The release of Prime Minister Mark Carney’s defence industrial strategy this week made me wonder if the root cause of Canada’s manufacturing decline is deeper than regulatory issues and tax policy. The biggest change over the eight decades between the Second World War and the COVID-19 pandemic was ideological. The industrial base that C.D. Howe harnessed to aid the war effort was largely a government creation. As decades passed, industrial policy fell out of fashion, superseded by an embrace of market economics. The hands-free approach to economy building lowered consumer prices, widened profit margins and created fiscal space for tax cuts. Most households became richer, an outcome that fit nicely with the end-of-history triumphalism that followed the collapse of the Soviet Union.

But the invisible hand is disconnected from society’s brain; it only knows efficiency, and is incapable of guiding traders towards outcomes that ensure resilience from external threats. To me, that’s the big lesson of the COVID-19 pandemic. If we want to be the kind of country that can take care of itself, then we have to be purposeful about it. Anyone who insists otherwise is trapped in a world view that has been undermined by everything we’ve seen happen since the world locked down in early 2020. Markets will provide a country with what it needs if that country can offer scale. That only applies to a handful of obvious places. Everyone else has to get creative, or exist at the mercy of others.

Dan Wasserman, an entrepreneur and reader who spent more than a decade helping clients navigate the U.S. government’s procurement system in Washington, D.C., wrote to tell me that he thinks the defence industrial strategy “could” work, assuming the men and women tasked with executing the strategy are up for it. Indeed, the involvement of three cabinet ministers and multiple departments and agencies suggest the risk of bureaucratic pitfalls will be high. Maybe the elevation in status of the new Defence Investment Agency will reduce some of that risk. It will come down to leadership, and an outfit led by an outsider hand-picked by the prime minister should be able to move the needle.

The other reason this time is different is the higher stakes. Industrial policy works when existential threats reduce the scope for politics and corruption to skew decision making. The reason Canada is buying icebreakers from Finland and shopping for submarines in South Korea is that each of those countries made conscious decisions to build industries that would make their economies more resilient.

It’s not as simple as buying Canadian, though. A recent assessment by the International Monetary Fund observed that to strengthen an economy, government spending on chosen companies must be supplemented by exports and a commitment to innovation. In other words, industrial policy fails when it dulls competition and becomes a substitute for making politically sensitive choices about tax and regulatory policy.

Even if the root cause of Canada’s manufacturing malaise is ideological, that doesn’t mean all the things on Marion’s list aren’t problems. Industrial policy gets the flywheel turning. Momentum will stop if there’s too much friction—and Canada’s economy features a lot of friction.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.