When the Bank of Canada cut interest rates in March, all anyone wanted to talk about was tariffs. But there were other tremors. Stock markets were volatile. Fear gauges were way up. And most startling of all, there was serious talk in Washington about the U.S. deliberately defaulting on some of its debt, abusing the trust that holds the global financial system together.

Skip to content

Commentary

Carmichael: The Trump shock marks the end of global finance as we’ve known it

The world will adjust, but the commercial relationships that have created much of the world’s wealth are over

U.S. President Donald Trump holds an executive order in the Oval Office of the White House on Wednesday, April 9. Photo: The Canadian Press/Pool via AP

When the Bank of Canada cut interest rates in March, all anyone wanted to talk about was tariffs. But there were other tremors. Stock markets were volatile. Fear gauges were way up. And most startling of all, there was serious talk in Washington about the U.S. deliberately defaulting on some of its debt, abusing the trust that holds the global financial system together.

“We saw that particular musing,” Bank of Canada senior deputy governor Carolyn Rogers said. “Concerning.”

Financial stability will be a bigger topic next week when Rogers and governor Tiff Macklem gather journalists to discuss their latest interest rate decision. Donald Trump’s latest display of yo-yo economics has cracked the foundation of the platform on which bankers disperse capital, venture firms price funding rounds and retail investors chase meme stocks. The way global finance works is being reset in real time, and that will change everything.

“It’s not about the economy,” said Charles St-Arnaud, a former Bank of Canada economist who left Ottawa to work for various international banks and now watches the markets from his perch in Calgary as chief economist at Alberta Central. “It’s about geopolitics. It’s a complete change in how the U.S. wants to be part of the global ecosystem.”

Related Articles

The current ecosystem was created by an earlier rupture that echoes loudly today. In August 1971, then-president Richard Nixon announced that the U.S. would no longer exchange dollars for gold, unilaterally upending an arrangement that the U.S. itself had effectively forged to avoid the sort of instability that created the conditions for the Second World War.

It was a prelude to a tough decade for the global economy, but nations adjusted. Central banks mostly stopped trying to manage exchange rates. The U.S. dollar remained the de facto reserve currency, but with faith in the Federal Reserve replacing faith in gold as the anchor that held everything in place.

The dollar’s primacy is an expression of the world’s confidence in the U.S.’s unique ability to keep a highly globalized world from collapsing in on itself. The country’s immense demand for goods and services make it a market-maker for global commerce. Its legal system protects investment, and its political system protects against arbitrary power. Its military keeps the peace.

Maybe most important is the U.S.’s pledge to always make good on its debts. That makes Treasury bonds and notes the benchmark for almost every price in the world because investors believe they will be paid back. Treasuries are the world’s haven when things get scary, a happenstance of history and economic heft that has allowed the U.S. government to borrow—and spend—in ways that no other country can. Of all the things that make the U.S. economy exceptional, the Treasury market is arguably the most important one.

I wrote the previous paragraphs in the present tense out of habit. It’s no longer safe to assume any of that is true to the degree it was before Donald Trump’s chaotic return to the White House. Rogers’ note of concern a month ago showed people were starting to ask questions. Trump’s “Liberation Day” tariffs answered them by way of a Nixon-style shock that showed the U.S. could no longer be trusted to wield its exorbitant privilege.

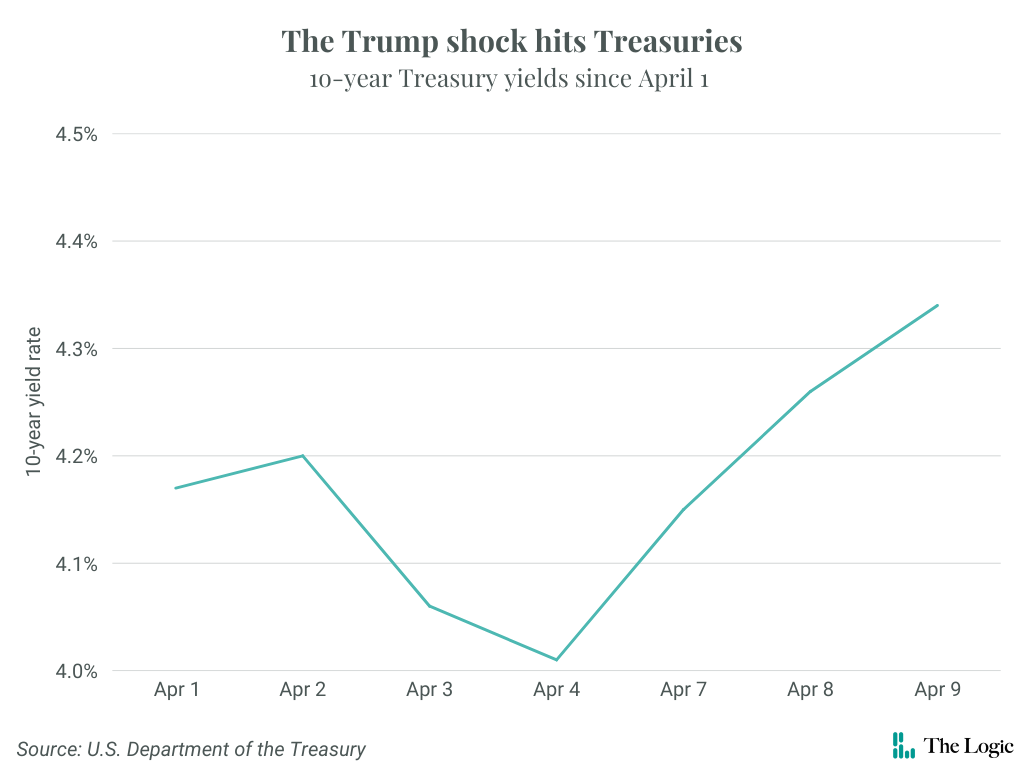

The tell that something bigger has happened was in the bond market. It wasn’t a haven during the most recent storm, at least not in the way it has been in the past.

Bond prices fell, causing interest rates to spike because the two have an inverse relationship. That’s not what’s supposed to happen at a time of crisis. Creditors insisted on a risk premium, as they do for any non-exceptional borrower. Many observed that the U.S. was trading like an emerging market. Markets looked fragile, like they did ahead of the financial crisis that caused the Great Recession, and during the COVID-19 pandemic. Instead of Treasuries, investors wanted cash.

“This could set off all kinds of vicious spirals, given government debts and deficits and dependence on foreign purchasers,” tweeted Harvard economist Lawrence Summers, a former treasury secretary and one of then-president Barack Obama’s main economic advisers during the 2008-2009 financial crisis. “The only way to mitigate these risks is for [Trump] to back off his current path. This is the first U.S. bout of U.S. financial instability caused by the U.S. government.”

Summers posted those thoughts early Wednesday morning. He was hardly alone in predicting disaster. By the afternoon, Trump had relented. The S&P 500 index surged almost 10 per cent. The relief spread through Asia and Europe on Thursday. Investors bought the dip—like Trump said on Truth Social a few hours before his tariff pause, it was a “great time to buy,” assuming you were a day trader or a professional investor with free cash and an appetite for risk.

It’s worth noting that anyone holding U.S. stocks purchased around the time of Trump’s inauguration was still out a significant amount of money. It’s also worth noting that euphoria tends to blur reality.

Think clearly about what happened yesterday. Trump paused most of the arbitrary increases and replaced them with a blanket tariff of 10 per cent. He left duties in place on Canadian and Mexican imports, and said he would raise tariffs on China to 125 per cent from 104 per cent—punishment for Beijing’s decision to apply border taxes of 84 per cent on U.S. imports.

Xi Jinping’s government held fire Thursday, but maintained that it has the wherewithal to “fight until the end” and that the U.S. will “reap what it sows.” The destruction of the commercial relationship that has created most of the world’s wealth over the past few decades wouldn’t inspire a historic stock rally on a normal day. That might explain why stocks fell when markets opened in New York on Thursday.

The world adjusted to the Nixon shock and it will adjust to Trump, eventually. But don’t let relief rallies fool you. This adjustment will hurt. Summers returned to social media after Trump’s reversal, but he wasn’t triumphant. “Much credibility has been lost,” he said. “Be afraid.”

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Pool via AP

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

News

Carney says trade talks to heat up after Trump’s latest tariff threats

Briefing

Sleep Country plots U.S. expansion after winning bid to buy hundreds of Sleep Number stores

Horizon Aircraft sells 5 vertical takeoff planes to Australia’s V-Star, with more on order

Bombardier shares hit highest level in 24 years after deal with Saudi firm

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.