What if Canada’s economy is more resilient than we thought?

Skip to content

Commentary

Carmichael: Canada’s economy is doing way better than you think

An influential economist breaks from the pack, predicting the country won’t need a rate cut for the rest of the year

RBC’s cardholders increased their spending through the spring, contrary to surveys showing low consumer confidence. Photo: Getty Images/Gary Hershorn

What if Canada’s economy is more resilient than we thought?

That question is at the heart of RBC chief economist Frances Donald’s latest economic outlook, a rare upward revision amid a plethora of assessments finding that the Canadian economy will do well to avoid a recession this year.

“It’s easy to see the downside risks and, rightfully, they have taken over the Canadian economic narrative for months,” Donald wrote in a short essay published alongside the new outlook. “But, while Canada’s economic path forward remains challenging, it appears considerably less treacherous than it did just a few months ago—a narrative that has yet to permeate the Canadian psyche.”

Donald commands attention. She made noise after joining Canada’s biggest bank last summer with a bet that the Bank of Canada was on the verge of making an outsized half-point rate cut. It was a bold call, as central banks prefer to make quarter-point changes. But it also was correct. Governor Tiff Macklem opted to pick up the pace, dropping the benchmark rate by a half point in both October and December.

Related Articles

Now, Donald has broken from the pack again, but in a different direction. Her team at RBC said this week that it thinks the Bank of Canada will leave interest rates unchanged for the rest of the year, in part because the economy is doing better than many expected at the onset of President Donald Trump’s economic warfare.

RBC now predicts that gross domestic product will grow 1.5 per cent, the same as in 2024. That isn’t great, but it would be better than many were expecting at the start of the year, as it became clear that Trump’s second presidency would be much different than his first.

For whatever reason, Trump went after his country’s closest trading partners first, imposing a 25-per-cent tariff on the pretext of the fentanyl epidemic. There was widespread panic. Former prime minister Justin Trudeau and some of the provinces retaliated, and some employers fired workers preemptively. University of Calgary economist Trevor Tombe declared in the aftermath of Trump’s initial tariff threats that a recession was coming. The tone was set.

Professional forecasters have been dropping quarterly and mid-year updates for the past couple of weeks. Most are bleak. Law firm Bennett Jones, where the team of policy advisers includes former Bank of Canada deputy governor Paul Beaudry, reckons we’re headed for at least a shallow recession. Tu Nguyen, an economist at consultancy RSM’s Toronto office, said it’s a “coin flip” whether Canada’s economy can grow amid a full year of tariffs and extreme uncertainty.

Nguyen forecasts essentially no growth in 2025. Bennett Jones predicts growth of 0.3 per cent this year. That kind of advice does little to improve the mood on the ground. “We’ll probably see another couple of rate cuts,” said Michael Waters, chief executive of Minto Group, an Ottawa-based real estate developer. “We may be in a recession by Q2 and Q3.”

Time for some Tolstoy, who wrote in War and Peace that “all we can know is that we know nothing.” None of the forecasts incorporate the potential fallout from a war between Israel and Iran, the latest geopolitical grenade to drop on anyone’s finely tuned model of where the North American economy might be headed. The Bank of Canada opted against even attempting a forecast in April, deciding the best it could offer was some scenarios based on different tariff levels.

The unusual level of uncertainty might demand extra effort in resisting our impulse to assume the worst. Donald’s relatively optimistic take is based on five things: Canada’s tariff burden is more manageable than we’ve come to think; surveys of anxious individuals and companies are discordant with their actual spending; the Bank of Canada has room to cut rates if things truly take a turn for the worse; there’s a tremendous amount of government spending in the works; and the U.S. economy is doing pretty well.

The first and second items on that list are the most interesting. As far as Donald can tell, the fear and loathing of the past seven months have done little to slow Canadians’ propensity to spend.

RBC economists compared the bank’s credit and debit card data with the Conference Board of Canada’s consumer confidence index. Confidence plunged to a record low in March and has remained weak ever since. Yet spending by RBC cardholders actually increased steadily through the spring, raising doubts about the reliability of “soft” sentiment data as a leading indicator amid a moment of profound, historic change. Statistics Canada reported this week that households’ net worth increased 0.8 per cent in the first quarter, the sixth consecutive quarterly increase. That’s an extra cushion to absorb the blow from the trade war.

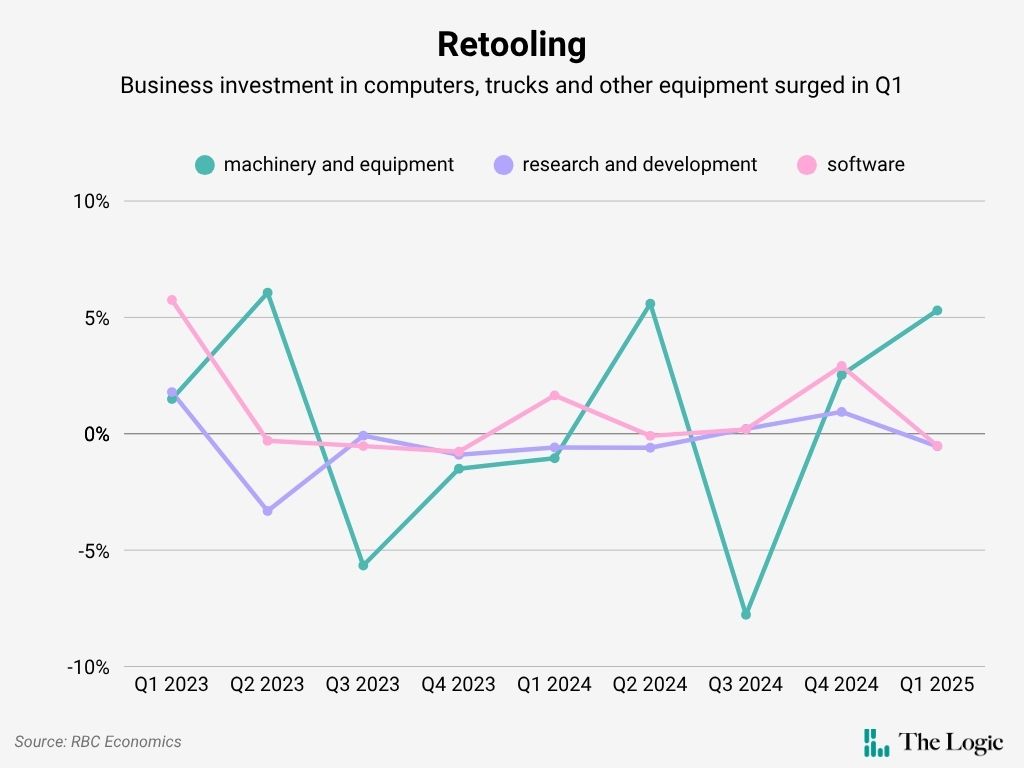

Another glitch in the doom narrative is the 5.3-per-cent increase in business spending on machinery and equipment in the first quarter, the most since the second quarter of 2024. Some of that might be companies trying to get ahead of Canada’s retaliatory tariffs: business investment in computers surged by 5.2 per cent, while spending on software and research and development was little changed.

But even if that’s true, those companies now have productivity-enhancing gear that they previously lacked. And if Donald is right, those businesses might soon discover that they don’t have it so bad. RBC calculates that Canada’s trade agreement with the U.S. and Mexico shields almost 90 per cent of exports from Trump’s tariffs, and that Canada’s average effective tariff rate was 2.3 per cent in April—up from effectively zero before Trump’s inauguration, but the lowest of all major U.S. trading partners.

A relatively positive outlook is different from a rosy one. The jobless rate is at seven per cent—the highest in nine years, excluding the COVID-19 pandemic—and it will take more than one good quarter of business investment to end the productivity crisis. Canada is in a tough spot. But maybe not quite as tough as we keep telling ourselves.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: Getty Images/Gary Hershorn

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

News

Nasdaq’s crackdown tests Canada’s bet on small public companies

Briefing

TC Energy says North American natural gas demand is growing much faster than previously expected

Mississauga imposes data centre pause, as Toronto councillors scrutinize local projects

A third of Canadian workers are using generative AI, but not for everything

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.