When Chrystia Freeland proposed tapping the $3 trillion in assets at the country’s pension funds to offset weak business investment, the pushback came quickly.

Evan Siddall, chief executive of Alberta Investment Management Corp., published a response in The Globe and Mail on Nov. 23, two days after Finance Minister Freeland used last week’s fall economic statement to say she will work “collaboratively” with pension funds to identify more opportunities for investment at home. Such a “dual mandate” would dilute fund managers’ fiduciary responsibility to deliver “safe, secure and growing” pension investments, Siddall wrote. “Inherently, it asks pensioners to foot the bill for Ottawa’s failure to promote Canadian economic growth and productivity.”

Siddall’s previous job was as head of Canada Mortgage and Housing Corp., where he distinguished himself by fighting attempts by the real estate industry and its sympathizers in politics to weaken mortgage restrictions. His commentary was a sign that he still is willing to show up the heads of public agencies who voluntarily attach muzzles when they take their jobs.

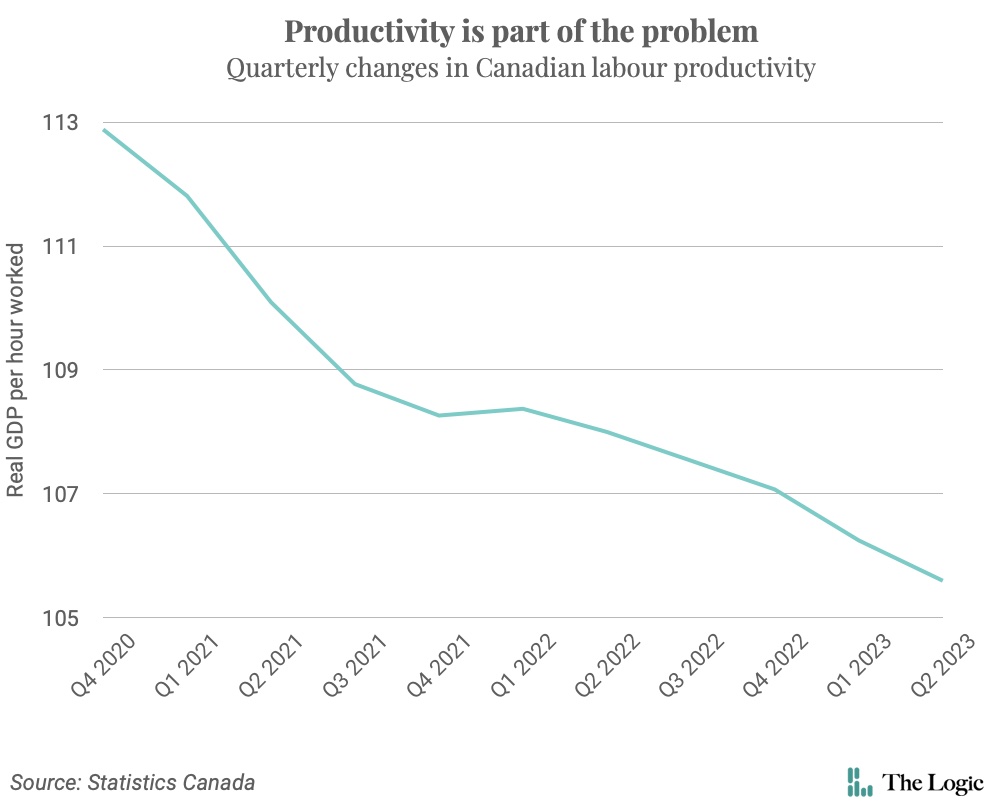

Siddall’s dig at Ottawa’s failure to find an answer to Canada’s embarrassing productivity numbers, despite decades of trying various tax incentives and spending plans, will have stung. Never good, labour productivity declined in 10 of 11 quarters through the second quarter of this year—and it was little changed in the quarter that it didn’t drop. By comparison, the amount of output generated per hour in the United States surged 4.7 per cent in the third quarter. Canada and the U.S. are different economies, but the disparity in productivity rates suggests that we’re doing something terribly wrong.

Productivity is an important part of the retirement story, so much so that it’s reasonable for policymakers to include pension funds in an urgent discussion over what to do about it. Politicizing investment decisions could harm returns, but there might be ways to minimize political influence while at the same time enlisting pension funds to help Canada ready for what promises to be an extended period of high volatility.

An economy that generates more wealth per worker will be less vulnerable to a shrinking workforce. To become more productive, workers need to upgrade their skills, and need their employers to give them better tools. But Canadian companies are notoriously stingy when it comes to investment, despite a competitive tax structure.

Jean-François Perrault, chief economist at Scotiabank and a former senior official at the Finance Department, said on a recent episode of the podcast “The Herle Burly” that it’s fair to conclude that governments have done enough to bring businesses “to the water.” He said the one big difference between the U.S. and Canada is the availability of capital— partly the result of our more conservative banking system, which avoids riskier investments.

That’s a problem, because Canada desperately needs financiers who aren’t beholden to a strict regulator—the Office of the Superintendent of Financial Institutions forces banks to keep enough cash in reserve to weather a wave of insolvencies. It also needs short-term investors who reward sturdy profit margins and upward sloping dividend payments.

The energy transition will require trillions of dollars, Siddall’s former employer estimates that by 2030 Canada will need 3.5 million housing units in addition to what’s already being built to balance supply and demand, and the country’s most innovative and ambitious companies will need money to exploit once-in-a-lifetime advances in digital technology and life sciences. If we don’t find the money, the societal issues related to housing affordability will continue, and we’ll miss a chance to take advantage of the opportunities presented by mass disruption.

“You’ve got to think outside the box,” said Perrault, who observed that Canadian pension funds’ share of domestic investments has been falling over time. So, he said, “Maybe what you do is you mandate a minimum threshold of Canadian investment in pension plans.” Do that, he continued, and “you would be adding massive amounts of financing to the Canadian economy—and maybe that’s the solution.”

Considering the stakes, and given the country seems to value a banking system that emphasizes stability and dividend payments, maybe a domestic investment requirement for pension funds would be the surest way to address Canada’s investment shortfall, albeit a less than perfect one.

Ideally, Canada’s cash-rich corporations would fill the capital void that Perrault identified. But if former Bank of Canada governor Stephen Poloz is right, companies will soon be shouldering a bigger share of the retirement burden.

In a paper published this month by the Healthcare of Ontario Pension Plan, Poloz makes the case for a “renaissance” in defined-benefit pension plans, which would offer people a certain amount of comfort amid the volatility we face from climate and technological change, political upheaval, geopolitical clashes and our aging society. He submits that employers will have to offer defined-benefit plans to attract scarce talent, or leave jobs unfilled.

Deputy Prime Minister and Finance Minister Chrystia Freeland speaks during a news conference in Ottawa in November 2023. Photo: The Canadian Press/Justin Tang

The goal is a secure retirement for as many people as possible. If more of us have defined-benefit plans, it matters less if pension funds settle for something less than maximum returns in a trade-off for contributing to nation building.

Companies moved away from defined-benefit pension plans because their owners decided it was too expensive to fund them. Poloz advised governments to make it easier for employers—especially smaller businesses—to pool pension contributions, which would distribute the risk and make it easier to guarantee a payout. It’s something Freeland should consider as she prepares her next budget. It would make her plans to work “collaboratively” with the pension funds look less like a raid on their assets.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.