The 1990s are having a moment. The “60 Songs That Explain the ’90s” podcast is a runaway hit. Earlier this month, it covered its 109th song, Puff Daddy’s “I’ll Be Missing You.” Host Rob Harvilla’s book went on sale this month. It might pair well with Chuck Klosterman’s The Nineties, if you’re looking for gift ideas for that nostalgic gen-Xer in your life.

There are four economic policies that explain the ’90s in Canada: an inflation target of two per cent, free trade, balanced budgets and active management of mandatory government pension contributions. These policies formed a consensus that was impervious to partisan attack and set up the country for a nice run of wealth creation. Following Finance Minister Chrystia Freeland’s fall economic statement this week, however, all of them are on the table for reconsideration.

First, a recap for readers who discovered The Police through the artist currently known as Diddy. The ’70s and ’80s were marked by inflation, budget deficits, trade wars and weak economic growth, creating the conditions for a global economic rethink that favoured markets over government intervention.

In 1991, Brian Mulroney’s Progressive Conservative government and the Bank of Canada agreed that monetary policy would be guided by an inflation target. Canada was a founding member of the World Trade Organization in 1995, a natural progression from its decision to join the original North American free-trade agreement, enacted in 1994. Liberals Jean Chrétien and Paul Martin ended a generation of budget deficits in 1997 and made balanced budgets an unassailable feature of Canadian politics for the generation that followed. Martin and the provinces also overhauled the Canada Pension Plan in 1997, doubling contributions and creating the Canada Pension Plan Investment Board to manage the fund’s assets actively.

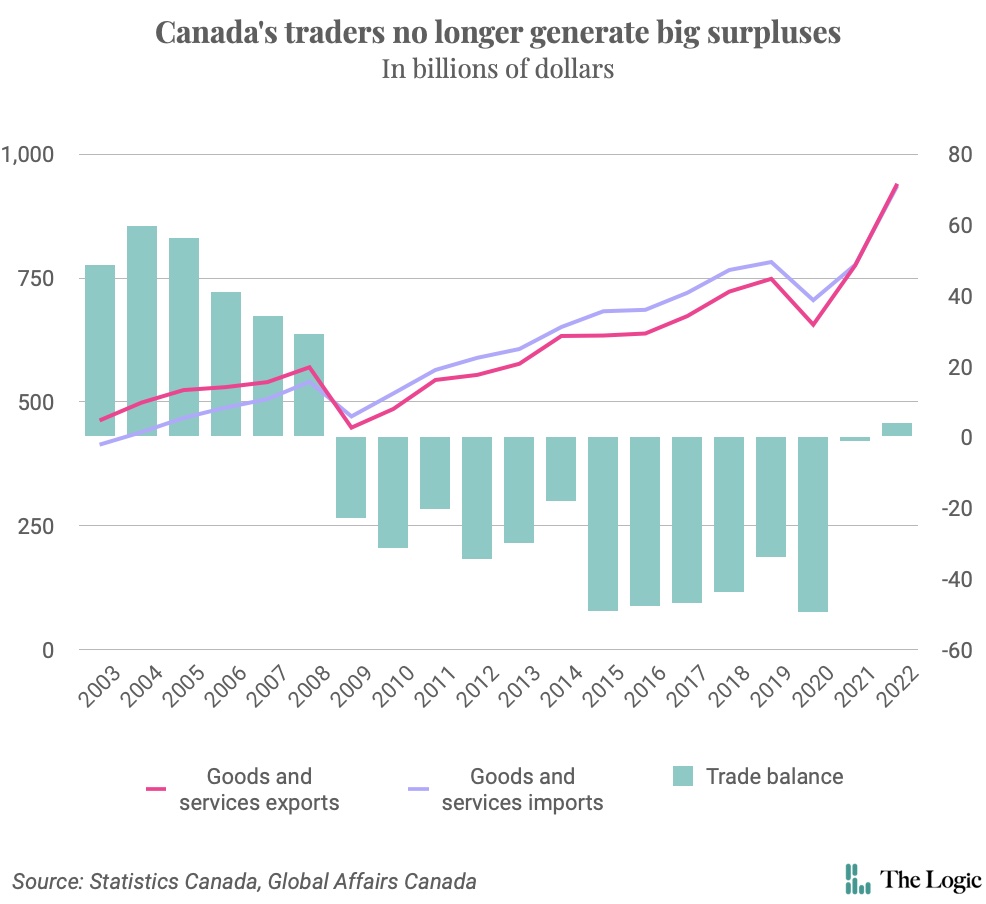

Canada’s economy grew 5.2 per cent in both 1999 and 2000, the most since 1984, when the country was recovering from a deep recession, according to International Monetary Fund data. (Growth hasn’t come near that mark since.) Inflation averaged 1.9 per cent between 1995 and early 2020. The CPPIB redefined financial risk, showing that it was to earn a safe return by taking measured bets on equities and infrastructure, making it easier for a declining population of active workers to make good on the country’s pension obligations.

Today, that consensus is breaking down.

Opposition Leader Pierre Poilievre said if he becomes prime minister he will fire Bank of Canada governor Tiff Macklem, violating the convention of central-bank independence, a tenet of inflation targeting. What’s more, the Conservative and New Democratic members of the “Curse of Politics” podcast—a must-listen for Canada’s politicos and a bellwether for partisan political thought—regularly argue that the two per cent target should be reconsidered.

Freeland has defended the central bank’s independence, although calling the central bank’s September decision to leave interest rates unchanged “welcome relief for Canadians” could be interpreted as applying subtle pressure.

Less subtle was this week’s fall economic statement, which showed the other three pillars of Canada’s economic policy consensus are either up for debate or no longer apply. Freeland said she will shrink the deficit to below one per cent of gross domestic product by 2027, but stopped short of pledging a return to surpluses. She also said the government “will work collaboratively” with Canadian pension funds to invest more in Canada, an encroachment on the understanding that active management of our mandatory retirement savings should be based on maximizing returns, not political considerations.

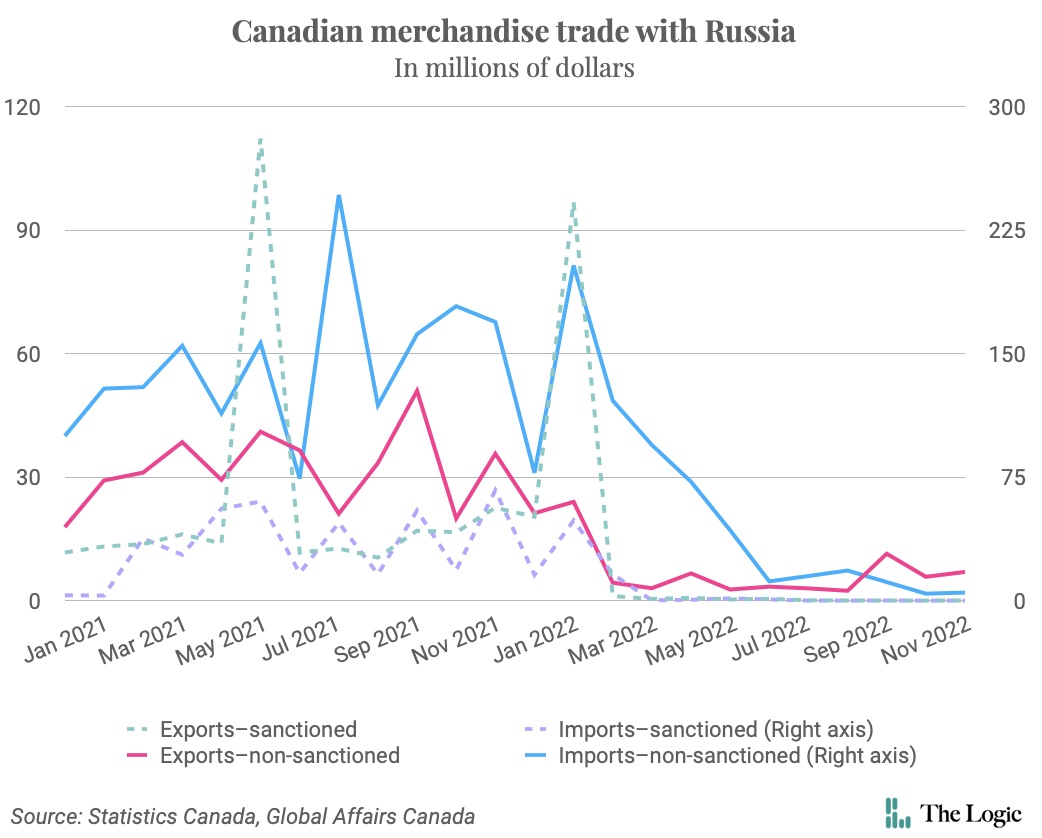

The Logic’s coverage of the fall economic statement highlighted Prime Minister Justin Trudeau’s re-interpretation of fiscal responsibility and his government’s sudden interest in the $3 trillion in assets under management at Canadian pension funds. Time and space kept us from getting to a companion piece the government released alongside Freeland’s update, called “Policy Statement on Ensuring Reciprocal Treatment for Canadian Businesses Abroad.” There’s an inverse relationship between trade policy’s importance to Canadians’ livelihoods and their interest in it, so on Tuesday we set it aside. Let’s give it some attention now.

The statement frees negotiators and policymakers from any lingering commitment to virtue when it comes to international trade. Canada won’t throw the first punch, but it is burying its Boy Scout image and will now hit back when it feels mistreated. The federal government’s new “reciprocity-based approach” will involve designing trade, investment and procurement rules that match those faced by Canadian companies in other countries; working with the provinces to ensure “sub-federal” rules also are tit-for-tat; and implementing incentives that encourage businesses to source from “trusted, reliable partners.”

Trudeau will continue to support the WTO, and reciprocal policies will include exceptions and waivers for the “limited circumstances” where it is too difficult to source supply from a friendly country or “regional considerations” need to be taken into account. But effectively, Canada has codified the turn from liberalized trade that started with Donald Trump’s presidency, and that has accelerated under Joe Biden. We’re managed traders now.

It’s unclear whether Canada is built for a tit-for-tat world. The overall market is relatively small, and many industries are controlled by oligopolies with significant homefield advantages. That makes it easy to ignore Canadian counterattacks, and the resulting trade wars end up hurting innocents—including Canadian importers and consumers.

But here we are. The previous policy consensus was rooted in a belief that market-oriented policies were the answer to high unemployment, inflation and geopolitical conflict. It worked for a while, but the last few years show that it was probably naive to have assumed everything was sorted. If there are things you liked about the ’90s, you should call your member of Parliament and tell them not to sabotage a good thing, because all those ideas are under review.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.