We’ve been conditioned to dismiss federal budgets and fiscal updates as political documents. That, and a shaggy carpet under which to obscure things the government would rather avoid talking about. But the big-picture thinkers usually manage to add some seriousness to the process. There’s direction on how Ottawa intends to confront the forces that are shaping the world.

Skip to content

Commentary

Carmichael: Freeland eyes power of pension funds to lift Canadian economy

Proposal to get funds to invest more at home opens a door that others worked hard to close

Deputy Prime Minister Chrystia Freeland in Ottawa for the fall economic statement on Nov. 21. Photo: The Canadian Press/Justin Tang

We’ve been conditioned to dismiss federal budgets and fiscal updates as political documents. That, and a shaggy carpet under which to obscure things the government would rather avoid talking about. But the big-picture thinkers usually manage to add some seriousness to the process. There’s direction on how Ottawa intends to confront the forces that are shaping the world.

In this way, Finance Minister Chrystia Freeland’s fall economic statement was more interesting than she indicated it would be. She is considering a rethink of Canada’s approach to retirement by working “collaboratively” with Canadian pension funds to encourage them to invest more in Canada.

That could be a game-changer at a time when higher interest rates have changed how investors think about risk, making venture capital harder to come by. But it also opens a door to political influence over pension management that the designers of Canada’s current approach to retirement worked hard to close. Freeland’s proposal isn’t radical, but it’s more evidence of how disruption is shaking Canada’s trust in markets to solve most of our problems. Ottawa is setting up to build more at home.

Related Articles

It will be tempting to dismiss much of what Freeland has to say. Prime Minister Justin Trudeau’s poll numbers this fall have caused many to give up on his government. And yet, an election still is (probably) two years away. He’s not a lame duck. The world order that enabled Canada to grow rich over the last few decades is falling apart, and it will be Trudeau who starts work on a new policy consensus for this difficult moment in history.

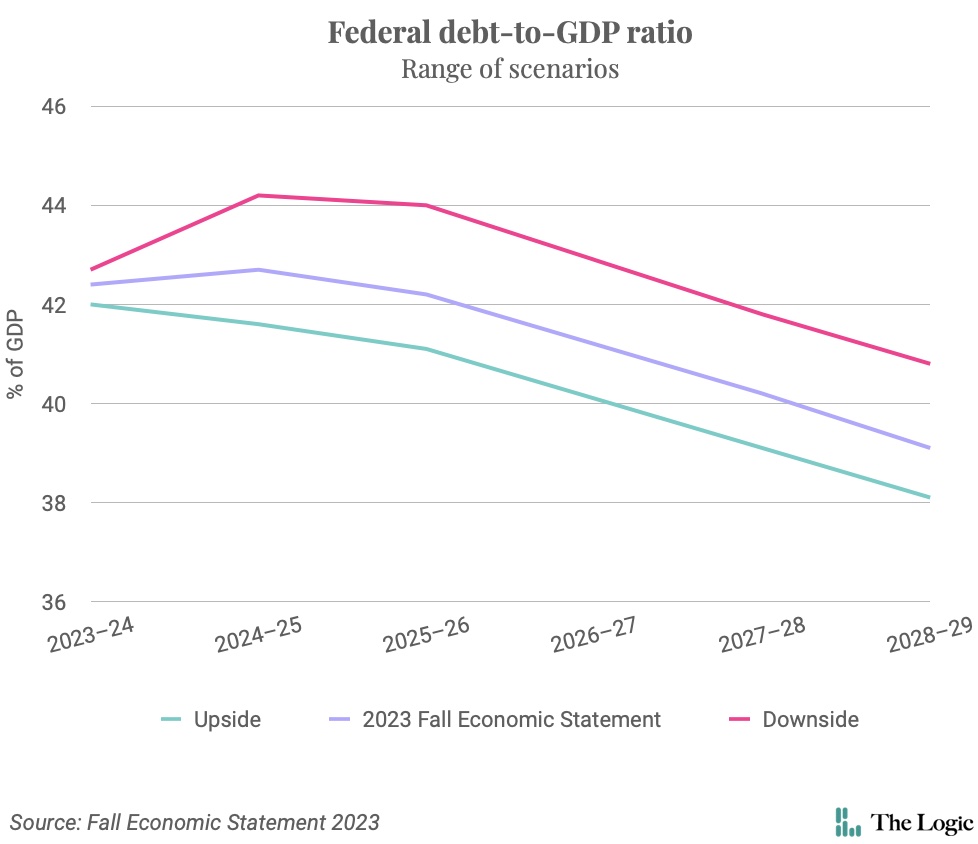

Freeland’s update represents a pivot from the runaway spending that started under the COVID-19 pandemic, while at the same time making clear this government thinks balanced budgets are a policy for another time. She promised to keep debt as a percentage of the economy on a downward track, but not before letting it creep up to about 42.7 per cent of gross domestic product next year, from 42.4 per cent the current fiscal year.

The deficit will be 1.3 per cent in the fiscal year that ended March 31, and 1.4 per cent in the current fiscal year. That’s no one’s definition of austerity, but it won’t cost Canada its AAA credit rating. Trudeau appears to have acknowledged that there are limits to what Canada can borrow.

Some—perhaps even many—will say that will leave Canada open to attacks from bond vigilantes. Interest rates already have climbed higher than anyone foresaw a few years ago. If bond traders lose faith in Canada’s ability and/or willingness to make good on its debts, those rates will rise even more. A deficit closer to one per cent of GDP might have been a more convincing sign that Trudeau and Freeland are truly committed to protecting Canada’s reputation safe credit risk.

But resiliency has become more complex than generating a clean balance sheet. Hedge fund billionaire Ray Dalio says the world is being reshaped by five forces: the “debt, money and economic” force; internal political instability; geopolitical instability and war; environmental changes driven by climate change; and technology, especially AI. That’s as good a sketch of what’s going on as any, and legacies will now be defined by how well leaders respond to those forces.

A country (or a company or an individual) could reasonably choose to cower in front of the forces that Dalio describes. But there would be an opportunity cost to that approach. Disruption of the sort that is taking place represents a rare opportunity to build resiliency through growth, too.

Read more on 2023 fall economic statement

In the ‘90s, manufacturing represented about 14 per cent of GDP in both Canada and Australia. It would decline in both countries, but more so in Australia, where manufacturing now represents about six per cent of GDP, compared with about nine per cent in Canada. Along the way, the Australian government decided to stop subsidizing automobile production; the country’s last automotive factory closed in 2017. Australia’s decision made sense in a world where China was a trusted trade partner and globalization was taken as a given. It’s fair to wonder if Australia would do things differently today.

Trudeau and the governments of Ontario and Quebec have deployed hundreds of billions to stay in the great game of competing with U.S. subsidies for green technology. Freeland’s update details “clean economy industrial supports” of about $8.5 billion through 2029. Canada is back in the business of picking winners.

Canada isn’t the U.S. and it can’t match the Inflation Reduction Act dollar for dollar. Freeland’s update suggests the federal treasury has committed all it can.

But Canada is a wealthy country, and it has $3 trillion in assets under management at its world-renowned pension funds, according to the fall economic statement. Freeland appears to think that it’s in the national interest to tap some of that money to help build houses and infrastructure and invest in the companies that stand to gain from technological disruption. She said the government will work with pension funds to “create an environment that encourages and identifies more opportunities for investments in Canada.”

That’s fuzzy. Less abstract was an announcement that the government will explore modifying a rule that blocks Canadian pension funds from owning more than 30 per cent of voting shares of Canadian corporations. She also said the government intends to require large federally regulated funds to disclose their investments to the federal banking regulator, a measure that would reveal the extent to which pension funds are exposed to places that have ended up on the opposite side of the new geopolitical divide.

The policy changes that allowed pension funds to pile up foreign assets were controversial, as they invited more risk. Now, the bigger risk could be that we’re sending too much of our wealth overseas, jeopardizing the country’s ability to generate economic growth over the longer term.

Forget what you thought you knew. Everything’s up for discussion.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Correction: The budget deficit in the current fiscal year is 1.3 per cent of GDP. The government will explore changing a rule that blocks Canadian pension funds from owning more than 30 per cent of voting shares of Canadian corporations. This column has been updated.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Justin Tang

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

News

Nasdaq’s crackdown tests Canada’s bet on small public companies

Briefing

Enbridge pauses pipeline expansion while producers hammer out growth plans

Weston-linked Wittington Ventures is building a company to reduce wildfire risk

Telesat and MDA Space shares soar on award of $2.3B military communications contract

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.