The Bank of Canada’s leaders want more evidence before they concede that the foundation of the global financial system is irreparably cracked.

Skip to content

Commentary

Carmichael: The ‘Liberation Day’ fallout has seized the Bank of Canada’s attention

If the U.S. dollar stops being the world’s reserve currency, the ripples will be felt everywhere

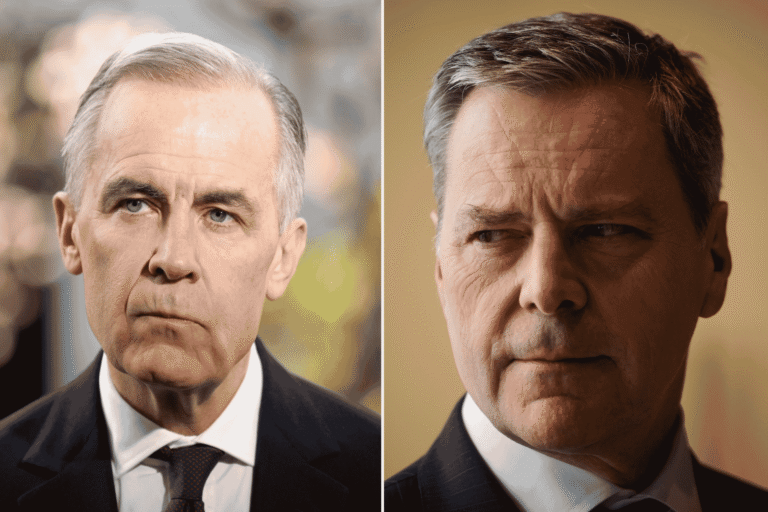

Governor of the Bank of Canada Tiff Macklem, right, and Senior Deputy Governor Carolyn Rogers at a news conference on the Bank's interest rate announcement and the quarterly Monetary Policy Report (MPR), in Ottawa, on Wednesday, April 16, 2025 Photo: The Canadian Press/Justin Tang

The Bank of Canada’s leaders want more evidence before they concede that the foundation of the global financial system is irreparably cracked.

“It’s pretty premature to make those kinds of declarations,” senior deputy governor Carolyn Rogers said at a press conference Wednesday. “I’ll just add that next week that I’m on my way to New York and then Washington for the spring [International Monetary Fund] meetings,” said governor Tiff Macklem. “I expect there’s going to be a lot of discussion on these issues.”

Whatever might be happening to the world financial order, the Great Repricing that followed U.S. President Donald Trump’s “Liberation Day” tariffs certainly got the central bank’s attention.

Macklem described the market’s reaction to the April 2 announcement, and then the reprieve that followed a week later, as violent.

Related Articles

Equity markets collapsed, then bounced back, creating anxiety among savers who already have enough to worry about. The central bank added “financial stress” to its watchlist of things that could introduce deflationary pressures, warning in its latest monetary policy report that “businesses and households, especially those directly impacted by tariffs, might experience a larger-than-expected deterioration in their financial health.” That could create a surge of bankruptcies that might “spread to lenders and lead to tighter credit conditions,” the report said. “Should this occur, economic growth would be slower and inflation would be weaker.”

So would the financial system generally, as lenders would have to deplete their rainy day reserves, introducing vulnerability at a time when it feels like Trump’s next utterance could cause everything to come crashing down. The most troubling part of the recent chaos was that their dollar fell, as did U.S. bond prices. That shouldn’t happen, because the Treasury market is the de facto global haven from financial storms. This time, some investors felt safer in places such as the Swiss franc and German bunds.

Those shifts have caused some discomfort. The Bank of Canada’s monetary policy report observed that since April 2, there have been “periods” where traders have struggled to make markets in longer-dated U.S. bonds because big players were having to get out of leveraged positions. The Treasury market earned its status as a haven because investors could buy safety whenever they wanted. The market is massive and the risk of default is thought to be minimal. The only time that rule doesn’t apply is during financial crises, when no one wants to buy anything. That’s when the cost of credit spikes, and bad things happen.

For now, the financial system appears to have survived the Great Repricing. “Despite the decline in liquidity, there has been no sign of dysfunction in major financial markets,” the monetary policy report said. Asked if financial stability risks had risen, Rogers said the central bank is “watching closely,” but added that “financial institutions are well capitalized. They have some room to absorb this kind of volatility.”

There is no reason to think the Bank of Canada is in denial about anything.

Macklem was the top diplomat at the Finance Department during the global financial crisis in 2008 and 2009, which put him on the front lines of the events that led to the Great Recession. He kept a photo from one of the crucial meetings of G7 officials in his office at the University of Toronto when he was running the Rotman School of Management. When I interviewed him there on the 10th anniversary of the collapse of Lehman Brothers, the bankruptcy that started a chain reaction through Wall Street and other financial centres, it still caused him obvious discomfort to recall the “enormous knot in our stomachs” during that time. He said the hardest part was knowing that something could break at any moment, but not being able to say anything about it.

“We have a tendency to see the world the way we would like it to be rather than the way it is,” Macklem said then. “We can be slow to recognize the problems are deeper than perhaps we initially thought. What does that mean? It means we have to find ways for ourselves to imagine what could go wrong and we have to force ourselves to think, ‘If this breaks, what would we do?’”

Those of us who think Trump’s tariff shock has caused the financial system to begin to mutate could be wrong. Avery Shenfeld wrote this week that there were no “end of the world as we know it” commentaries while U.S. Treasury 10-year yields plunged almost 40 basis points ahead of “Liberation Day.” The “simplest” explanation for the spike in borrowing costs was simply a correction, Shenfeld said.

Financial calamities tend to be preceded by long periods of complacency. Even if global markets managed to absorb the latest tumult, it would be folly to assume that everything is normal. In a social media post Thursday, Trump said that U.S. Federal Reserve chair Jerome Powell should be cutting rates and that his “termination cannot come fast enough!”—giving investors another reason to wonder whether U.S. debt is the stable investment it once was.

All of this matters. Macklem isn’t on pleasure trips when he jets to places such as New York and Washington. If the U.S. dollar is unmoored as the primary reserve currency, the ripples will be felt everywhere. The Bank of Canada based this week’s decision to leave interest rates unchanged on two illustrative scenarios of how the economic war could unfold. The gentler of the two assumed an exchange rate of about 70 U.S. cents, while the severe thought experiment assumed an exchange rate of 67 U.S. cents.

Currency adjustments are important shock absorbers for Canada. A weaker exchange rate will help exporters fight for market share despite Trump’s border taxes.

But what if the currency doesn’t adjust this time because investors have decided they want to punish the dollar? The loonie was trading at 72 U.S. cents Thursday, compared with 69 U.S. cents at the end of March—something else that doesn’t make sense.

It’s safe to assume that Macklem has booked lots of meetings next week. He and his counterparts have plenty to discuss.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Justin Tang

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Commentary

Carmichael: Tiff Macklem can’t save you

Briefing

Canada to publish list of imports at risk of being made with forced labour

TMX Group acquires RAFI Indices for $683M

Ikea invests in Toronto food startup NS/TX Industries’ US$10.5M fundraise

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.