The Bank of Canada left the benchmark interest rate unchanged at 2.75 per cent, ending a string of seven consecutive cuts. Governor Tiff Macklem acknowledged that U.S. President Donald Trump’s economic war could cause a recession, and said the central bank is prepared to act “decisively” if incoming information shows that tariffs are having an outsized effect on either inflation or economic growth.

Skip to content

News

Bank of Canada holds key interest rate steady at 2.75%

Trump’s aggressive trade moves could cause recession, Macklem warns

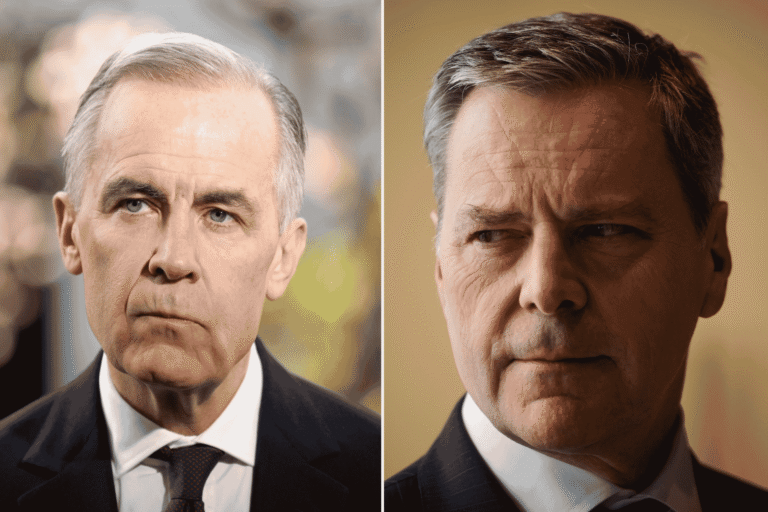

Bank of Canada governor Tiff Macklem in Ottawa, in January 2025. Photo: The Canadian Press/Justin Tang

The Bank of Canada left the benchmark interest rate unchanged at 2.75 per cent, ending a string of seven consecutive cuts. Governor Tiff Macklem acknowledged that U.S. President Donald Trump’s economic war could cause a recession, and said the central bank is prepared to act “decisively” if incoming information shows that tariffs are having an outsized effect on either inflation or economic growth.

Pervasive uncertainty: The Bank of Canada said the “major” shift in U.S. trade policy has both diminished prospects for economic growth and raised inflation expectations. That’s a nightmare scenario for Macklem and his deputies, as monetary policy is geared to stoke growth when inflation slows, or take the punch bowl away when the party starts to get out of hand. They don’t have a lot of experience fighting on two fronts at once.

Trump’s erraticism makes forecasting impossible, so the central bank decided to avoid delivering false precision by way of typical quarterly outlook. Policymakers used a couple of illustrative scenarios to frame how economic conditions could evolve. But even within those, the degree of uncertainty is unusually high, given the “magnitude and speed of the shift in U.S. trade policy are unprecedented,” the central bank said.

Related Articles

Scenario planning: The Bank of Canada has a sense of what happened between the start of the year and the start of Trump’s presidency. The economy grew at an annual rate of 2.6 per cent in the fourth quarter, driven by strong residential and business investment and household consumption, according to its monetary policy report. That momentum slowed amid all the uncertainty and new tariffs. Policymakers reckon growth dropped to 1.8 per cent in the first quarter, weaker than they predicted in January. They observed that a weaker currency appears to have made some imports more expensive, reversing a cooling trend in the cost of goods. Short-term inflation expectations have increased, indicating additional upward pressure.

The trajectory of the trade war will dictate what happens next. The central bank’s “Scenario 1,” which assumes a mix of high uncertainty and relatively constrained tit-for-tat tariffs, would result in weaker growth and inflation around the two per cent target. “Scenario 2” assumes an escalation that includes U.S. tariffs on all imports of 25 per cent and retaliatory Canadian duties of 12 per cent on $115 billion of U.S. goods imports. That thought exercise produces a recession that would spill into 2026, when inflation spikes to 2.7 per cent.

But these are merely rough guides. The actual outcome could be much better or much worse. “A lot has happened since our March decision five weeks ago,” Macklem said. “But the future is no clearer.”

Precautionary pause: There is lots of evidence of worry in the Bank of Canada’s latest assessment, so much so that it could have made a convincing case for a cut. However, with inflation getting warmer and the future so cloudy, Macklem opted to avoid a mistake and buy some time. He emphasized that he’s prepared to “act decisively” if incoming information argues for rate cuts to fight deflation—or increases to contain an upward surge in price pressures.

“Monetary policy will ensure inflation remains well controlled and support economic growth as Canada confronts this unwanted trade war,” Macklem said in a statement.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Justin Tang

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Commentary

Carmichael: Tiff Macklem can’t save you

Briefing

Canada to publish list of imports at risk of being made with forced labour

TMX Group acquires RAFI Indices for $683M

Ikea invests in Toronto food startup NS/TX Industries’ US$10.5M fundraise

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.