The Logic’s latest subscriber survey suggests readers are hesitant to shift their finances from big banks to relatively new players—and that one fintech firm, Wealthsimple, stands far ahead of the pack.

Skip to content

Wealthsimple’s smartphone app in June 2024. The fintech’s products were used by 46 per cent of respondents to The Logic's latest subscriber survey.. Photo: The Canadian Press/Giordano Ciampini

Wealthsimple’s smartphone app in June 2024. The fintech’s products were used by 46 per cent of respondents to The Logic's latest subscriber survey.. Photo: The Canadian Press/Giordano Ciampini

Subscriber Survey

Do The Logic’s readers trust fintechs? Not as much as banks, two-fifths say in survey

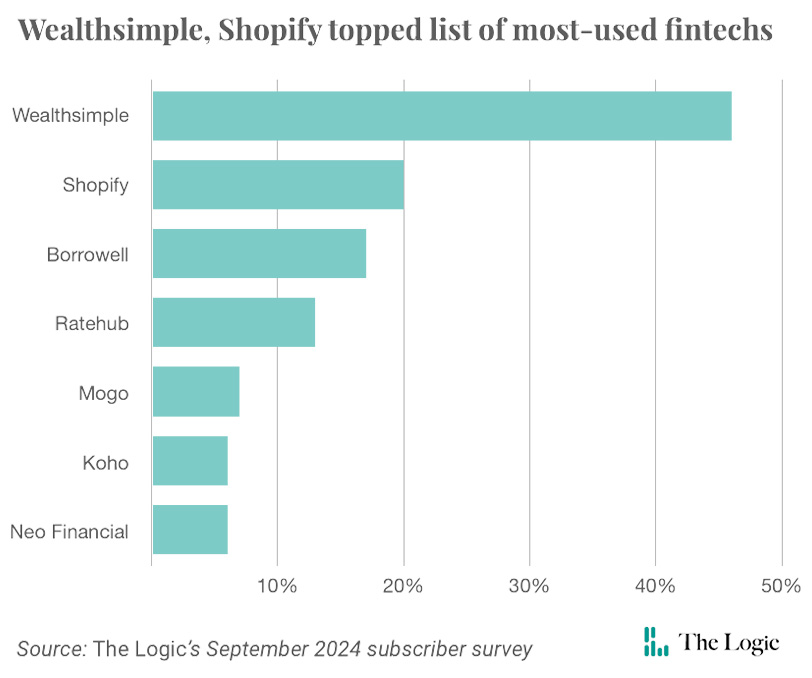

Almost half of respondents used Wealthsimple, more than double other fintechs

Wealthsimple’s smartphone app in June 2024. The fintech’s products were used by 46 per cent of respondents to The Logic's latest subscriber survey.. Photo: The Canadian Press/Giordano Ciampini

The Logic’s latest subscriber survey suggests readers are hesitant to shift their finances from big banks to relatively new players—and that one fintech firm, Wealthsimple, stands far ahead of the pack.

Eighty per cent of respondents said they use some type of fintech product, but despite that, 42 per cent said they think fintechs are less trustworthy than traditional banks.

Close to half use Wealthsimple, at 46 per cent, more than twice as much as any other major Canadian fintech: Shopify came in second at 20 per cent.

One reader wrote that fintechs “would need to have superior services, while also proving that they have excellent data security and that they will protect my privacy—i.e., that I would not be the product.”

Related Articles

Another reader who said they trust fintechs less than banks gave a succinct explanation: “I worked at one.”

Canada’s financial system has historically been dominated by the “Big Five” banks—BMO, Scotiabank, TD Bank, CIBC and RBC—a situation many argue is an oligopoly. (The Bank of Canada disagrees, but they took the issue seriously enough to study it in depth.) Fintechs have rushed into the sphere to offer Canadians more options, often with fewer fees, and offering everything from buy-now, pay-later services to small-business loans and savings accounts, challenging the big banks.

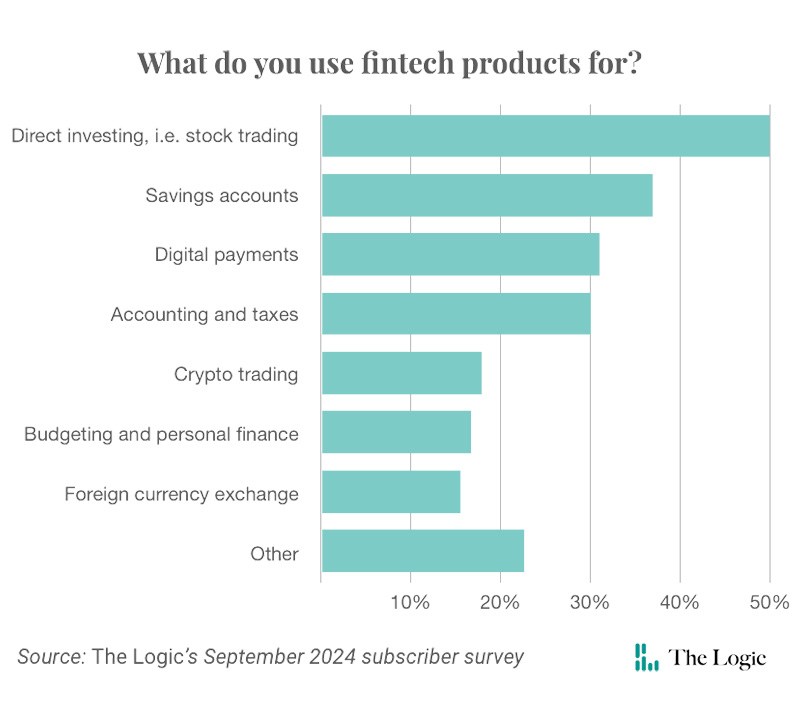

Exactly half of respondents use fintechs for direct investing; 37 per cent use them for savings accounts, and more than 25 per cent use them for either digital payments or accounting and taxes. Most of them, at 70 per cent, said they use fintech products for personal finance, while 11 per cent use them for business reasons.

“I appreciate the free-market drive for fintechs to provide differentiated services compared to the big banks,” wrote one reader. Another said, “The [fintech] fees are lower and I have always had great service, whereas I have quit big banks over shady practices—like charging me credit-line protection I had declined.”

“I worked at a big bank,” wrote another reader, “and know that staff there are entirely judged on the products they sell. This leads to bank employees not doing what’s best for their customers to make their KPIs [key performance indicators].” With fintechs, they argue, “Individuals have more autonomy to make their own decisions.”

After Wealthsimple and Shopify, Borrowell and Ratehub.ca were the only other two major fintech firms with products used by more than 10 per cent of respondents (17 and 13, respectively).

What do potential customers want in a fintech? “Compliance with regulation, number of users, lack of lawsuits,” wrote one. “A business strategy that tells me they will still be here in two years,” said another, while a third said: “Length of time in market, leadership of fintech firm with experience in [the] domain their product serves, large list of integration partners.”

More than half (56 per cent) of respondents wanted to see more regulation in the fintech industry. “While big banks are weighed down by regulations, the lack of regulatory oversight on fintechs is concerning,” wrote one reader who worked in the sector, adding, “The mindset around customer data privacy, recordkeeping, etc., makes me wonder about a day when things go wrong.”

Other readers thought regulatory scrutiny might stifle fintech innovation—and wouldn’t guarantee any more security than banks. One reader noted that TD Bank has been accused of facilitating money laundering and that the major credit agencies, Equifax and TransUnion, have had major data breaches. If that’s still happening at banks, the reader wrote, “I don’t see why fintechs in Canada should be regulated more than now.”

Methodology

The Logic emailed subscribers a private link to an online survey on Sept. 23 and the survey closed Sept. 25. Respondents’ identities were kept anonymous. Subscribers were first asked, “Do you use products from any of these fintech companies?” They were invited to select all that apply from this list: “Wealthsimple,” “Koho,” “Borrowell,” “Mogo,” “Nuvei,” “Shopify,” “Neo Financial,” “League, “FreshBooks,” “Benevity,” “Clearco,” “Coinsquare,” “Ratehub.ca,” or “None of the above.”

They were then asked what they use fintech products for, and to select all that apply from this list: “Savings accounts,” “Direct investing,” “Buy-now, pay-later services,” “Small-business loans or financing,” “Personal loans and mortgages,” “Digital payments,” “Budgeting and personal finance,” “Accounting and tax software,” “Cryptocurrency trading” and “Foreign currency exchange”; if they selected “Other” they were asked to specify.

They were asked if they used fintech products mostly for personal or business finances, or neither, and to elaborate on their answer. They were asked how much they trust fintech companies compared to traditional banks: “More than banks,” “About the same,” or “Less than banks”; if they selected “Other,” they were asked to elaborate. They were asked “Do you believe there needs to be more regulation of fintech products?” with the options “Yes” and “No,” and to elaborate on areas where they would want more or less oversight. Finally, they were asked an open-ended question where they could write their own answers about what their main reasons would be for trusting one fintech company over others.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Giordano Ciampini

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Commentary

Carmichael: Canada’s culture of risk aversion has created an economic doom loop

Briefing

TC Energy says North American natural gas demand is growing much faster than previously expected

Mississauga imposes data centre pause, as Toronto councillors scrutinize local projects

A third of Canadian workers are using generative AI, but not for everything

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.