When Bank of Canada governor Tiff Macklem last spoke—on Sept. 24 at a gathering of bankers in Toronto—he adjusted the central bank’s framing of the economy ever so slightly.

Skip to content

Commentary

Carmichael: Will Macklem maintain his gentle approach to cuts?

An increasingly bleak economic outlook suggests the Bank of Canada may pick up the pace

Bank of Canada governor Tiff Macklem and senior deputy governor Carolyn Rogers at an interest rate announcement in Ottawa on Sept. 4, 2024. Photo: The Canadian Press/Justin Tang

When Bank of Canada governor Tiff Macklem last spoke—on Sept. 24 at a gathering of bankers in Toronto—he adjusted the central bank’s framing of the economy ever so slightly.

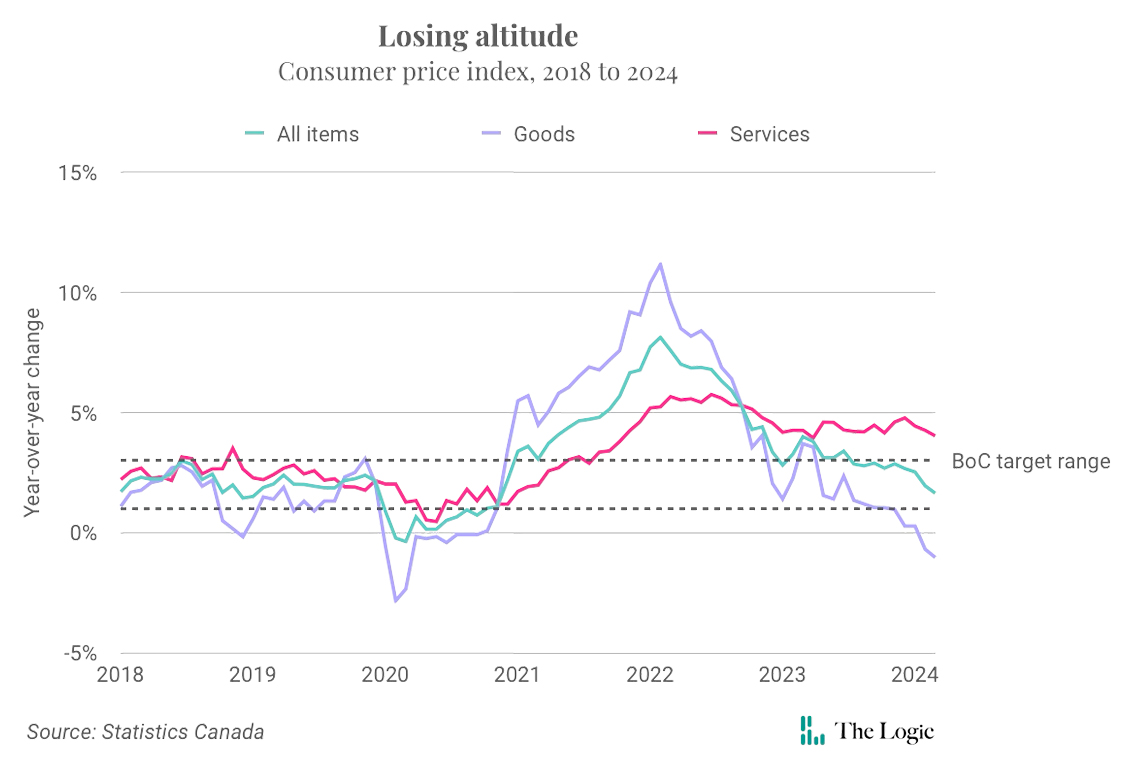

Gone was any suggestion that inflation might reignite. A week earlier, Macklem’s top deputy, Carolyn Rogers, had told another Toronto audience that there was “still work to do,” even though Statistics Canada had just reported that the consumer price index increased two per cent in August from a year earlier—exactly what the Bank of Canada aims to achieve by raising and lowering the benchmark interest rate.

Rogers left the impression the central bank was still playing defense. Macklem’s remarks tilted towards offense. He pledged to keep inflation “close” to the centre of the target range of one to three per cent, which implied the central bank would now focus on keeping the disinflationary trend from turning into outright deflation.

“We’ve been pleased to see inflation come all the way back to the two per cent target,” Macklem said in prepared remarks. “We need to stick the landing.”

Related Articles

Landing analogies are imperfect descriptions of what central banks are trying to do. Pilots and gymnasts aim to come to a complete stop, while Macklem and his peers are attempting to achieve something closer to a glide. Still, enough of us have flown to know a “soft landing” is preferable to a “hard” one. Interest rate spikes of the kind we endured between 2021 and 2023 tend to result in the latter.

Maybe not this time. Statistics Canada reported Tuesday that the consumer price index increased 1.6 per cent in September from a year earlier—below the Bank of Canada’s target of two percent for the first time since February 2021. Meanwhile, the jobless rate was 6.5 per cent, higher than its pre-pandemic level of around five per cent, but still decent by historical standards.

A soft landing was always going to be difficult. EntireFlight, a website for pilots and aviation enthusiasts, says it is “important for the pilot to maintain a certain speed during landing to ensure a safe touchdown.” In other words, you have to pull back on the throttle, but not so much that you lose all momentum. Otherwise, gravity will take over.

So far, Macklem has opted for a gentle approach. He cut borrowing costs sooner than most of his peers, dropping the benchmark rate a quarter point in June. The Bank of Canada followed with quarter-point cuts in July and September. It looked like the course was set, as most Bay Street economists predicted a series of incremental cuts into next year.

But as inflation drifted closer to target, visibility worsened. The central bank’s policymakers discarded their detailed checklist of indicators and said they would make decisions about rate cuts on a meeting-to-meeting basis. The ground was closer than they realized. All relevant measures of inflation are now hovering around the central bank’s target of two per cent—something the Bank of Canada’s most recent economic forecast said would take until 2025 to achieve.

The Federal Reserve’s decision to cut rates by a half point last month stoked a debate about whether the Bank of Canada, which so far this year has made only quarter-point cuts, should do the same. Initially, there was resistance to the idea. The Fed was playing catch-up, as stronger growth and stickier inflation caused it to wait to cut rates even as other central banks started to move. There is also an incorrect notion in financial markets that Canada is fated to follow the Fed wherever it goes. Early bets that the Bank of Canada would accelerate the pace of rate cuts looked a little knee-jerk, maybe in part because Macklem was so reluctant to declare victory over inflation.

But with each piece of new data, the near-term outlook for the economy became more bleak.

Productivity growth remained negative, gross domestic product figures disappointed, and hiring plateaued over the summer. As Bay Street economists updated their forecasts for the rest of the year, more predicted the Bank of Canada would pick up the pace. RBC’s pivot was the sharpest, as it advised its clients last week to anticipate half-point cuts next week and again in December. “There is little evidence that the economy is close to turning a corner,” economist Claire Fan wrote.

Inflation has eased, but households will continue to suffer sticker shock—rent and groceries were about 21 per cent higher last month than in September 2021, compared with average hourly wage growth of roughly 15 per cent over that same period, according to Statistics Canada data. That doesn’t bode well for consumer demand, which wouldn’t be so troubling if other engines weren’t also sputtering. The central bank’s latest quarterly survey of businesses showed last week that executives were planning little investment because sales were too weak and the cost of capital too high.

The new inflation numbers caused three holdouts—Scotiabank, BMO and CIBC—to join the bandwagon for a half-point cut, leaving TD alone on the fence among the big banks. Since the Bank of Canada’s goal is a soft landing, it’s possible to understand why they got on board. The strategy for landing a plane is determined by the length of the runway, and Macklem’s just got a lot shorter.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: The Canadian Press/Justin Tang

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

News

Nasdaq’s crackdown tests Canada’s bet on small public companies

Briefing

TC Energy says North American natural gas demand is growing much faster than previously expected

Mississauga imposes data centre pause, as Toronto councillors scrutinize local projects

A third of Canadian workers are using generative AI, but not for everything

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.