Listen Now

0:00

Mark Carney isn’t known for modesty. He proved it Monday, foreshadowing a narrower deficit and lighter debt burden that he attributed to the talent that he’s assembled in his government.

“We’re good fiscal managers,” the prime minister said at an event in Ottawa.

It was a legitimate boast. Finance Minister François-Philippe Champagne’s spring economic update suggests that he and the prime minister are indeed decent fiscal managers. They are also extremely lucky ones.

Related Articles

Federal revenue is now projected to be $7 billion higher in the fiscal year that ended March 31, and $9 billion higher in the current fiscal year, thanks in large part to “higher revenues from the financial sector and resilience in the labour market.”

The former would have had much to do with soaring financial markets, which in Canada were driven higher by an incredible rally in gold prices. The labour market was saved by whatever caused U.S. President Donald Trump to spare the North American trade agreement from his assault on global trading norms. Carney and Champagne can’t claim credit for either of those things.

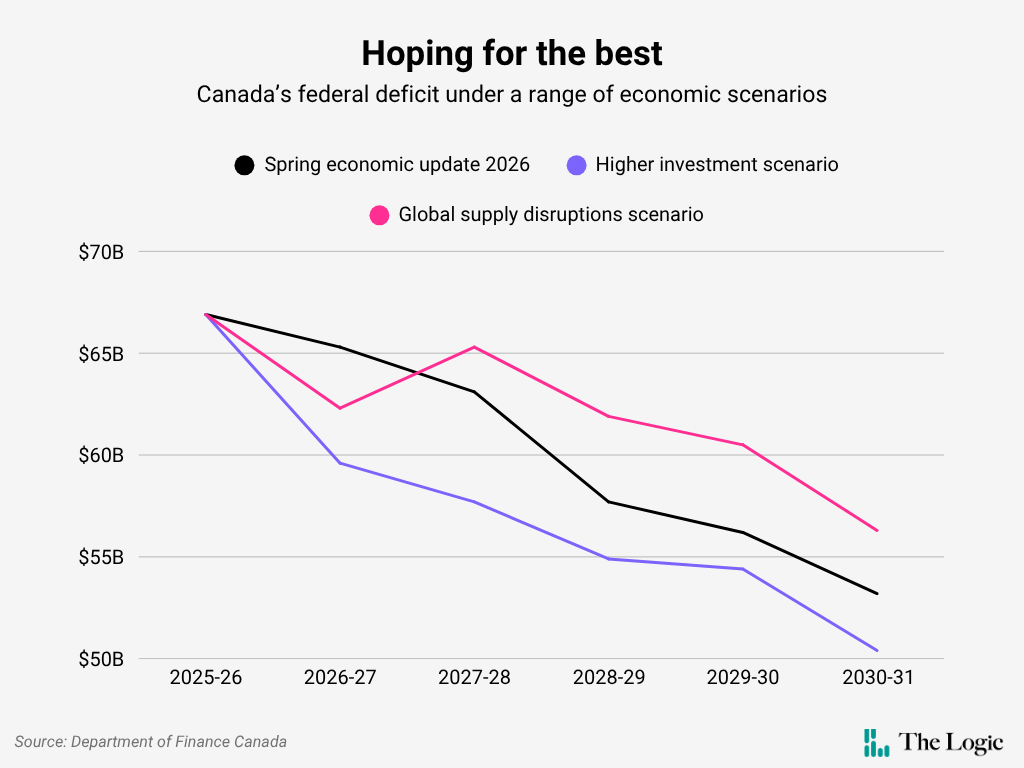

Still, bad fiscal managers might have used that unexpected bounty to buy some goodwill ahead of a future election. Conversely, they might have used it to record an even narrower deficit simply for the sake of recording a narrower deficit. Champagne found himself with an extra $60.3 billion with which to play between the fiscal year just ended and 2029-30, and he allocated $54.5 billion. That keeps the deficit at about two per cent of gross domestic product, and on track to shrink to 1.4 per cent of GDP by 2031.

Some would prefer a balanced budget, but hitting that target would mean ignoring people’s anguish over higher living costs and the opportunity cost of foregone investment in security and trade infrastructure. Carney and Champagne might have done more to restrain spending. The federal fuel tax holiday could have been more targeted, for example. But they did enough to keep creditors from insisting on a higher risk premium to lend the government of Canada money. They did no harm.

In fact, the constraint of sticking to the fiscal trajectory they set out in November might actually have forced them to get creative. The update contained a few new ideas to resolve problems that have plagued Canada’s economy for years, if not decades, but none come at an onerous cost.

The $25 billion with which Carney intends to seed the new Canada Strong Fund is eye-catching. It’s an extension of the prime minister’s thesis that he can use the federal government’s ability to borrow relatively cheaply to leverage investment that outweighs whatever it ends up paying in additional interest. That strategy has limits, but Carney hasn’t hit them yet. The federal government can borrow for 10 years at about 3.5 per cent, compared with the U.S. 10-year yield of about 4.4 per cent.

A pledge to create a start-to-finish training program for new trades workers is an acknowledgement that the existing labour pool lacks the talent to execute Carney’s vision—and that whatever disparate attempts that provinces and employers have made to inspire younger Canadians to join the trades have essentially failed, so it was time to try something new.

Champagne said the government intends to conduct “comprehensive mandate reviews” of all the Crown lenders and investment funds to ensure their financial firepower is having “maximum impact.” Champagne also said that he will present a strategy to ensure that most everything the government does promotes competition by “removing inefficient government policies that impede competition arising from regulation, procurement and industrial support.”

These might seem like small things, but they show the government is focused on economic growth. That’s positive, because the Finance Department’s scenario analysis of what might unfold over the next few years suggests that growth could come hard.

Finance’s baseline estimate for inflation-adjusted GDP growth—based on the consensus forecast of Bay Street analysts—is 1.1 per cent in 2026 and 1.9 per cent in 2027. That’s not a great outlook. Spain’s economy, for example, will grow 2.1 per cent this year, after growth of 2.8 per cent in 2025, according to the International Monetary Fund.

To help prepare for better or worse outcomes, Finance constructed scenarios based on a world where the Iran war leads to higher oil prices and increased investment by Canadian oil and gas producers, and a world where the war causes severe supply disruptions like those that followed the COVID-19 pandemic.

The positive scenario would result in smaller deficits because the government would benefit from higher corporate income taxes. But inflation-adjusted economic growth would be about the same as the baseline because inflation pressure would push interest rates higher. The negative scenario—a protracted war in the Middle East that constrains the supply of fundamental inputs such as oil, gas and fertilizer—could result in growth of only 0.8 per cent this year and 1 per cent in 2027.

Growth that slow would create a headwind that would challenge Carney’s efforts to ignite an investment boom. So far so good, but there’s still a lot of hard road to travel.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.