In February 2010, Stephen Harper’s government hosted a meeting of G7 finance ministers and central bank governors in Iqaluit.

The financial crisis of 2008 and 2009 had morphed into a sovereign debt crisis in Europe. Folks were busy. Yet Canada had the audacity to use its turn as G7 chair to force people such as the U.S. treasury secretary and the managing director of the International Monetary Fund to gather in the Canadian Arctic—in February.

At least one European official thought the idea was “crazy,” The Guardian reported at the time. Somehow, the meeting ended without a vote to remove Canada from the group.

I remember wondering why the G7 was bothering to meet at all. Global powers had by then decided that the larger G20 was the better forum to seek cooperation on big cross-border problems. Wall Street, the City of London and their regulators had been humbled by their roles in causing the Great Recession. China had done as much as anyone in resolving that crisis by executing a fiscal stimulus program so large that it revived global economic growth and commodity prices.

Fast forward to the present: the G7 is getting its swagger back. Like Kate Bush, Bruce Springsteen and Judas Priest, this act that debuted in the 1970s has managed to remain relevant despite some lulls.

Last weekend in Italy, Finance Minister Chrystia Freeland and Bank of Canada governor Tiff Macklem backed a communiqué that the Financial Times interpreted as a pledge to use profits from the Russian assets those countries have seized to finance Ukraine’s attempt to repel Vladimir Putin’s invasion. All that’s left is for the leaders to stamp their approval when they meet in Italy later this summer.

The G20—which includes G7 antagonists China and Russia and frenemies Turkey and Saudi Arabia—has accomplished little of consequence for years. Meanwhile, Sweden and Finland have joined NATO, and the U.S. and its friends in Europe and Asia are coalescing around the idea of “friendshoring,” a mild version of de-globalization that uses sanctions, tariffs and massive spending on industrial policy to route supply chains away from China and to isolate countries such as Russia and Iran.

Prime Minister Justin Trudeau’s government has fully embraced this new/old order, deploying hundreds of millions of dollars to entice automobile and battery makers to set up in Ontario and Quebec, and using Ottawa’s foreign-investment screening process to repel Chinese investors from claiming Canadian resources.

Mark Carney, then Governor of the Bank of Canada, in Iqaluit in 2010 for a meeting of G7 finance ministers and central bank governors. Photo: The Canadian Press/Fred Chartrand

Some Canadian executives and investors will be relieved by this turn of geopolitical events. For a decade or so, it looked like anyone who wanted to surf the biggest waves would have to find a beach in Asia. Suddenly, the U.S. is back on top. Marc Gilbert, a managing director at Boston Consulting Group in Toronto, said “a lot” of clients are thinking like this: “My Lord, we are so fortunate to be next to the U.S. and their economy is very strong … Let’s live off that fortune and be more present in it. Let’s expand in it.”

Expand in it, we should. The U.S. government is spending heavily on clean technology and artificial intelligence, the country’s economy is experiencing a productivity boom, and its population is growing—and it’s all happening right next door.

Just because it feels like the 1970s doesn’t mean the Western powers have turned back the clock, however. Hans Rosling, author of the Factfulness, warned against dividing the world into halves and assuming there was a gap between the West and the rest. That’s never been more true.

China generates output of US$25,000 per person, when adjusted for purchasing power parity, according to the International Monetary Fund; Canada produces about US$60,500. Be wary of letting that gap create a sense of economic superiority, because averages obscure reality. China might still have a large number of relatively poor people, but it also has a lot of rich ones.

The point is to avoid the mental trap of thinking about the world in binary terms—in this case, the rich and powerful democracies and the autocracies that govern the “developing” world. Many of the countries that tend to get lumped into the latter group are no longer developing, they’ve arrived. As my colleague Anita Balakrishnan showed last week, countries such as Canada and the U.S. have little to teach China when it comes to creating clean technology.

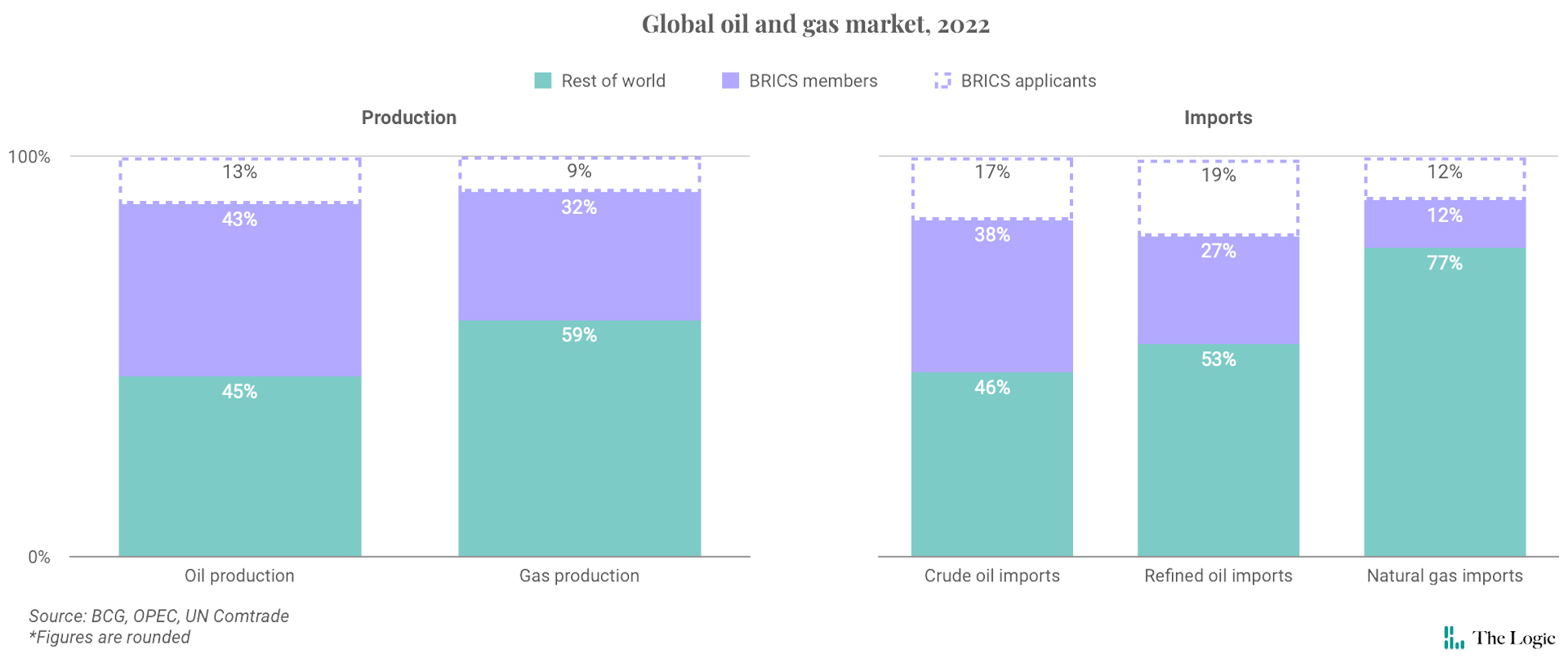

In April, Gilbert and some of his Boston Consulting colleagues published a report on how the BRICS countries—Brazil, Russia, India, China and South Africa—are stitching together a network that already rivals that of the G7. This year the group expanded to include Egypt, Ethiopia, Iran, Saudi Arabia and the United Arab Emirates. Another dozen countries have asked to join. If they are accepted, the group would represent a third of global GDP, more than half of all oil production and a lot of economic opportunity.

That opportunity won’t be restricted to the members of the newly expanded BRICS group. Gilbert is advising his clients to look for opportunities to trade and invest within the group, or in a BRICS-adjacent country. In other words, set up shop in one of those places, rather than give up because geopolitics makes it too difficult to conduct business by remote control.

For Canada, that will require more geopolitical savvy than doing business in the U.S., but the rewards could be worth it. The G7’s leaders might be trying to replay the 1970s, but don’t expect the rest of the world to follow.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.