The panic level over Canada’s ability to innovate and maximize its resources has gone from zero to eleven in a matter of months.

“A friendlier business environment is urgently needed in this country if we are to close our productivity gap,” National Bank chief economist Stéfane Marion wrote this week. “In particular, large institutional investors must be offered attractive opportunities for long-term domestic investment across various asset classes. That’s the only way to avoid further erosion of our standard of living.”

Canada definitely has a productivity problem. The opportunity cost of ignoring it has increased because our traditional growth strategy—immigration-led population growth—appears to have reached its limits. Still, it might be time to pump the brakes on all this catastrophizing, if only a little. The neighbours are starting to talk.

“While there is genuine room for concern, the bad news is much overstated,” Tyler Cowen, an economics professor at George Mason University in Virginia and co-author of the widely read Marginal Revolution blog, wrote in his Bloomberg column. “Yes, Canadian performance could be better, but there’s no reason to be pressing the panic button.”

The argument to let the hysteria rip is that contemporary democracies appear to need crises to get things done. Justin Trudeau’s government has a reputation for putting all of its attention on the headlines and too little on the fine print. “They’re good at announcing programs; the strength has not been in the execution, or the clarity around it,” TMX Group chief executive John McKenzie said recently in an interview.

There are lots of examples. Trudeau has created a menu of clean energy tax credits, but hasn’t yet implemented any of them. The Canada Infrastructure Bank has been such a disappointment that Opposition Leader Pierre Poiliviere says he will close it if he wins the next election. The government excited tech companies with a 2022 promise to create the Canada Innovation Corporation to better focus innovation policy, then frustrated them a year later by delaying its launch.

Trudeau’s government is at least talking about economic policy more seriously than it has in the past. An extended period of negative productivity growth, weak business investment and a stagnant economy are “an urgent challenge for Canada, if not the most urgent challenge,” Finance Minister Chrystia Freeland said earlier this year.

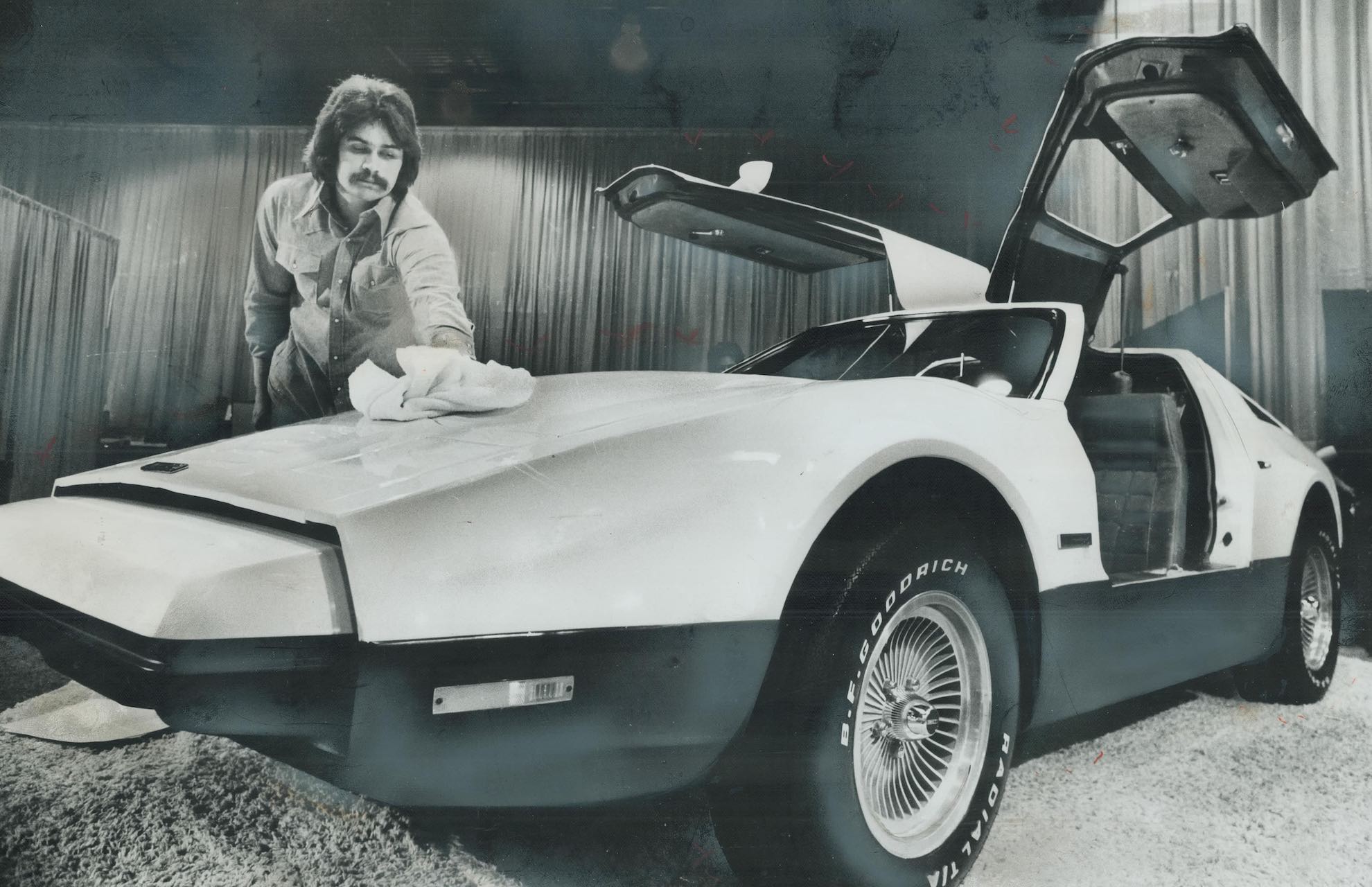

A Bricklin at the Auto Show ‘75 in Mississauga, Ont., in February 1975. Photo: Toronto Star via Getty Images/Doug Griffin

But we probably should be wary of stoking the fires to a point that elected officials feel compelled to do something rash. Industrial policy in North America got a bad name during the 1970s, a moment of high anxiety fueled by high inflation, stagnant economic growth and intense geopolitical tension.

Sound familiar? Maybe we ought to keep our heads, lest we commit millions in public funds to build a modern version of the Bricklin, that gull-winged and star-crossed reminder of how industrial development can go wrong. Finance ministers are considering directing pension funds to invest more of our retirement contributions at home. Such a consequential decision should be made after due consideration, not in a state of panic.

Less noticed here in the fishbowl is that the rest of the world still sees Canada as a relatively good place to be. According to the OECD, flows of foreign direct investment into Canada were US$42 billion in the first nine months of 2023, more than any other rich country with the exception of the United States. The pace was a 17 per cent increase from 2022 and a nine per cent increase from the same period in 2019.

Cowen took note of the way many economists and commentators are writing off Canada as a serious economy based on output per person. In recent years immigration has increased the population, but gross domestic product hasn’t grown at nearly the same pace, so per capita GDP has slumped. The numbers look especially bad when marked against the U.S., where a surprise jump in productivity and a strong labour market is powering America through higher interest rates and elevated inflation unlike any place in the world.

Economists often use per capita GDP as the benchmark for “standard of living.” The idea is the more goods and services a country makes per person, the richer it is. Cowen offered another way to think about standard of living, one more rooted in how people actually live. When statistics agencies measure GDP, they adjust for inflation. The Canadian GDP numbers most quoted are adjusted using producer prices—what the makers of goods and providers of services pay for inputs and receive for their output. Cowen said economists generally agree that when considering living standards, GDP should be adjusted for consumer prices. Measured that way, Canada’s per-capita GDP mostly has been rising steadily.

“It is fair to wonder why the Canadian economy, in relative terms, seems to be slipping behind the U.S.,” Cowen wrote. “As a general observation, this is true of most developed economies, and perhaps it says more about American virtues than Canadian defects.”

Canada’s jobless rate is hovering around historical lows, inflation is coming down, and the middle class is wealthier than it was before the pandemic. Like most other rich countries, we’re muddling through the aftermath of one of the most extraordinary events in history. The debate should be over whether we can do better than muddle through.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.