Venture capital in Canada has flourished in the era of low interest rates, allowing startups and scale-ups to raise record amounts of money. But with the Bank of Canada expected to raise rates on Wednesday to stem inflation, now at a 30-year high, investors say the hikes could have a ripple effect on venture-backed companies, making it harder for them to close fundraising deals at the size and pace to which they’ve become accustomed.

Skip to content

News

How interest-rate hikes could temper Canada’s hot venture-capital market

Governor of the Bank of Canada Tiff Macklem participates in a media availability at the Bank of Canada in Ottawa, in December 2021. Photo: Justin Tang/The Canadian Press

Venture capital in Canada has flourished in the era of low interest rates, allowing startups and scale-ups to raise record amounts of money. But with the Bank of Canada expected to raise rates on Wednesday to stem inflation, now at a 30-year high, investors say the hikes could have a ripple effect on venture-backed companies, making it harder for them to close fundraising deals at the size and pace to which they’ve become accustomed.

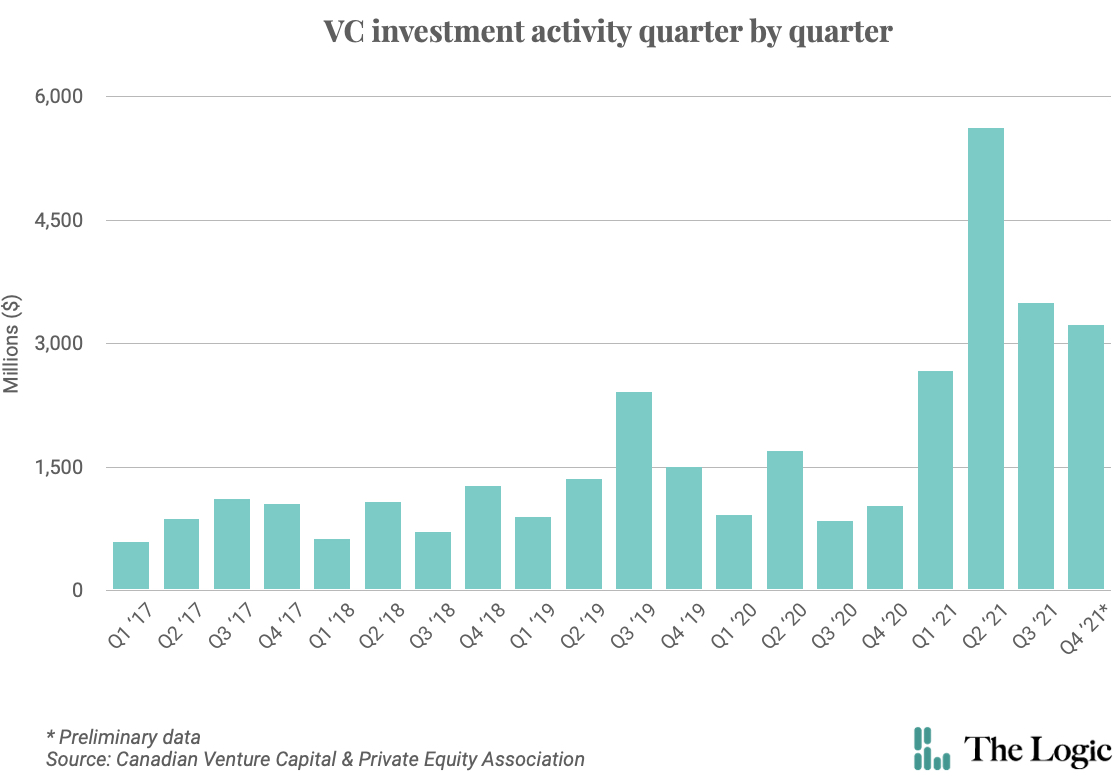

In the four years since the central bank last raised its key rate, the annual value of venture capital deals in Canada has grown from $3.7 billion in 2018 to about $15 billion in 2021, based on estimates from the Canadian Venture Capital & Private Equity Association (CVCA).

Talking Point

Venture capital investors anticipate mounting inflation and rising interest rates to dampen record-high valuations in Canada’s startup sector, and could make it harder for later-stage companies to raise rounds at the size and rate they’ve become used to during the pandemic.

The jump in deal activity last year coincided with billions of dollars in government stimulus to help safeguard against COVID-19 pandemic-related hits to business and the economy. But with employment and GDP now back around pre-pandemic levels—and inflation more than five per cent above where it was a year ago—Bank of Canada governor Tiff Macklem said this month the economy no longer needs government stimulus. Rather, “the economy will need higher interest rates to moderate growth in spending and bring demand in line with supply,” he said in a speech at the Canadian Chamber of Commerce.

Increasing interest rates is meant to cool prices by making it more expensive to borrow. Investors who spoke to The Logic said the impact on venture capital and startups will be indirect and affect companies differently, depending on their maturity and the size of the funding rounds they’re after.

Wittington Ventures managing partner Jim Orlando said the most direct way rate hikes might hit a company is if it’s in the business of selling non-essential goods. “There’s less discretionary income in people’s pockets, so expenses that are discretionary will naturally reduce,” he said.

He also predicted that rising interest rates will have the biggest impact on later-stage private companies, whatever sector they’re in, as the deep-pocketed investors those companies need to back big late-stage fundraising rounds look instead for less risky investments.

The stock market isn’t immune to the impacts of rising interest rates—they’re already being felt to some extent—but Orlando said stocks, being liquid, give investors more control over how and when they move their money. “A lot of the new entrants into venture during 2021 were of the hedge fund ilk,” he said, “and they have opportunities to put their money elsewhere that’s better on a risk-reward basis. If there are better valuations in public markets, I think they’ll go back to the public markets.”

Damien Steel, global managing partner at OMERS Ventures, expects limited partners—the firms that put their money into venture capital funds—to be impacted most by rate hikes. “My guess is that most large investors have shifted almost completely out of fixed income and into equity over the past five years,” he said. “A reversion back to a more normal asset mix could take some dollars away from private equity and therefore venture. My guess is this will lead to a very difficult fundraising environment for GPs [general partners] over the next year and possibly longer.” However, he expects the fallout for VCs and startups to be minor. While some venture investors—many of which built up ample dry powder while interest rates were low—may wait out the difficult environment, “I would argue they won’t,” said Steel. “GPs aren’t good at standing still.”

A preliminary report from CVCA on 2021 venture capital activity shows that deal-making has already slowed somewhat. Investments dropped from about $5.6 billion in the second quarter to $3.5 billion and $3.2 billion in the third and fourth quarters, respectively.

Investors who spoke to The Logic agreed that VCs and the firms they back should expect valuations to come down over the next year or so. “We’re already seeing valuations starting to get more reasonable,” said Panache Ventures managing partner Patrick Lor. He said a major factor is the drop in the public market amid inflation and anticipation of interest-rate hikes, as well as ongoing instability in the world. “The public markets were a massive path to exit for a lot of companies. In the past year or so, you saw these kinds of not-quite-ready-for-IPO kind of companies go public early because the market was so frothy,” he said. “When you see that taken away, there’s a waterfall effect that essentially brings valuations more in line with traditional multiples.”

That could create particular difficulty for later-stage companies planning to go public. “It could affect how much they’re able to raise and the time to IPO,” said Janet Bannister, managing partner at Real Ventures. “If markets are soft because interest rates are going up, it may also mean that banks put off plans for an IPO.”

Early-stage companies, though, may find some investors eager to participate in more deals this year as valuations come down. Wittington Ventures made just two new investments in 2021 compared to five the year before, said Orlando. “Frankly, there were certain companies that we would have loved to be invested in, but they were done at prices that we didn’t feel would stand the test of time,” he said. “I anticipate that as valuations start to correct, we’ll be more active in 2022.”

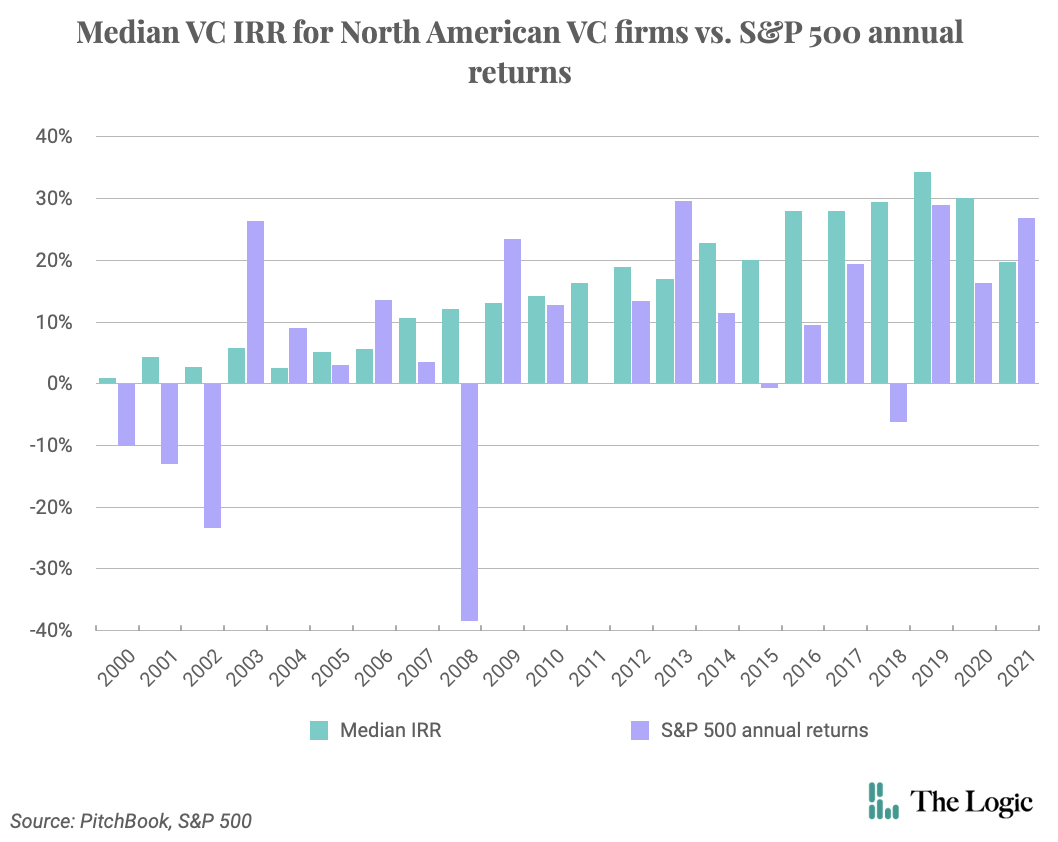

Bannister emphasized that it’s hard to predict how the venture market will respond. “It’s not just math; it’s emotion. How are people going to respond?” She pointed to data from funds that raised and invested during the 2008–09 recession, which, on average, far outperformed the stock market.

“Investors who do invest when the markets go down, when everybody else is worried, those investments tend to produce the highest returns,” she said. “One reason is there’s lower valuations, but the other thing is that tough times produce more resilient founders. If investors pull back a little bit, maybe that’s not all bad after all, because those great companies will survive and thrive.

Correction: This story has been updated to correct the spelling of Damien Steel’s name.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: Justin Tang/The Canadian Press

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

News

Canada’s oil majors eye the next production boom

Briefing

Celestica completes US$3.45B share sale to meet demand for data-centre equipment

Sun Life pitches itself on Wall Street as an alternative to Blackstone, Apollo

MDA revenue jumps 34% in Q2, raises full-year outlook

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.