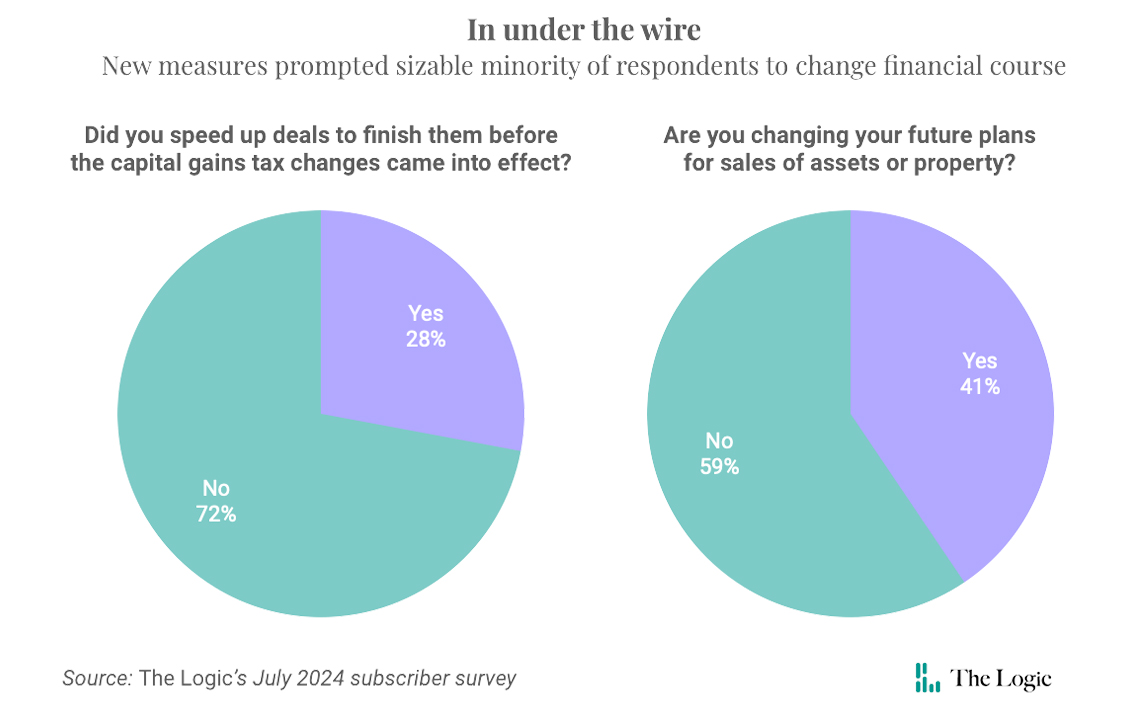

Over a quarter of respondents to the latest Logic subscriber survey said they pushed asset sales forward—from cottages to corporate shares—before the new inclusion rate for capital gains tax came into effect last month.

Skip to content

Subscriber Survey

28% of Logic survey respondents rushed to sell assets, close deals to avoid capital gains changes

Two-fifths say they will change plans for future investment

A Lake Muskoka cottage; vacation properties were among the assets respondents to our readers' survey said they made sure to sell before new tax rules came into effect. Photo: Toronto Star via Getty/Dick Loek

Over a quarter of respondents to the latest Logic subscriber survey said they pushed asset sales forward—from cottages to corporate shares—before the new inclusion rate for capital gains tax came into effect last month.

About 41 per cent said they’re changing their plans for transactions due to the new tax measures. Most expressed negative views of the tax changes, though a sizable minority defended the rules.

First proposed in the 2024 federal budget, changes to taxes on capital gains—meaning profits from sales of assets like property or stocks—came into force on June 25. For a person’s capital gains over $250,000 a year, two-thirds of that income is now taxable, up from 50 per cent. There are exceptions: sales of principal residences are exempt, and entrepreneurs selling a business will pay taxes on only one-third of capital gains, up to a lifetime maximum of $2 million. Corporations, meanwhile, will have all of their capital gains taxed at the higher two-thirds inclusion rate.

Related Articles

Many in Canada’s tech sector vehemently opposed the changes, arguing they will drive away investment and cause founders to relocate. The federal budget said the goal is to treat different kinds of income more equally, and Finance Minister Chrystia Freeland argued that such measures are the cost of maintaining a stable democracy.

Readers had a few weeks to make changes before the new inclusion rate took effect. Respondents described a range of hurried transactions as the June cutoff neared—businesses sold on short notice; ownership of cottages transferred; assets moved from corporate to personal accounts; and shares liquidated and options exercised sooner than intended.

Others couldn’t get deals done in time. “We tried (unsuccessfully) to speed through an acquisition so the founders would have a better exit,” one reader wrote. Another said they were hoping for a Pierre Poilievre victory in 2025: “[I’m] sitting on two family vacation properties and praying for a Conservative government to reverse the new capital gains tax.”

Some readers detailed intricate planning in response to the changes. Several intended to keep their capital gains below $250,000 each year, while others discussed relocating to different jurisdictions or sending money to their children earlier to avoid higher taxes on inheritance.

Most respondents, at 75 per cent, didn’t push any deals or assets sales forward, and most aren’t changing their future plans. Some said expected gains are protected by the principal residences exemption or tax-free savings accounts, or that they don’t make enough to think about the tax. As one subscriber put it: “As if I have property, haha!”

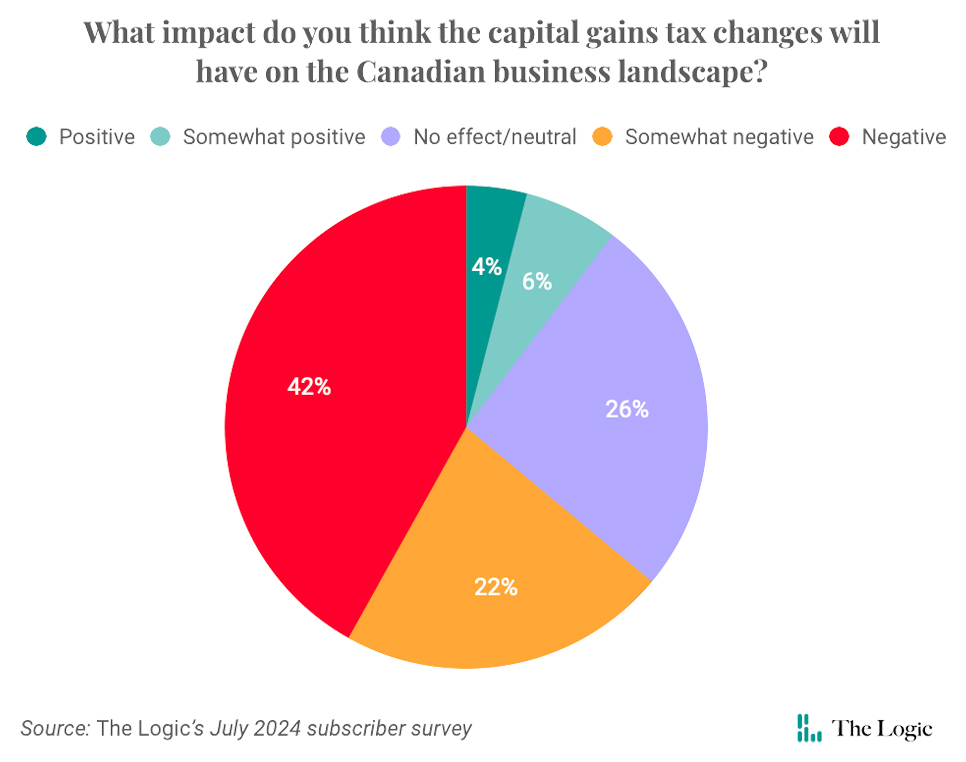

A clear majority of respondents took a dim view of the tax changes, with 63 per cent saying it would be negative or somewhat negative for the Canadian business landscape. Around a quarter expected no effect, and only a tenth viewed it as either positive or somewhat positive.

One reader said there are many other factors that influence innovation and entrepreneurship. “If I build a $100-million business in Silicon Valley and sell it, my combined tax rate is 36 per cent, higher than what Canada’s new rate will be. Yet Silicon Valley is still the engine for startups, because tax is low down the list.”

A few readers described drastic changes at their organizations, such as relocating executives and headquarters to the U.S. or revising a family trust to spread out capital gains. “We have a tax lawyer looking at how we have to restructure stock options—and the advice so far has been that there are other places (outside of Canada) to enable us to minimize liabilities,” a subscriber said.

Readers were split on whether it affected their motivation to start their own business. “Between this and the anticipated reforms [to the Scientific Research and Experimental Development tax credit program], there are very, very few reasons to incorporate in Canada versus in Delaware. I expect my future businesses will be incorporated in the States, even if I choose to hire Canadian employees,” one subscriber wrote.

Others said the changes had more of an emotional impact than a practical one, because they came at a difficult time for startups. “In terms of getting capital, it’s much harder and I would attribute that to COVID-19, inflation and interest rates,” a reader said. “We are in a cycle when it’s hard, and blaming it on one thing is not rational.”

One entrepreneur said they are not yet at a threshold to be affected and that it would be a sign of their company’s success. “I find that the negativity towards the new tax rules is dominated by a vocal minority of very successful businesspeople—good on them—whose success is atypical.”

Methodology

The Logic emailed subscribers a private link to an online survey on July 18 and the survey closed July 22. Respondents’ identities were kept anonymous.

Subscribers were first asked, “Did you speed up deals, either at your organization or personally, to finish them before the capital gains tax changes came into effect?” and could answer “Yes” or “No.” Next, they were asked, “Are you changing your future plans for sales of assets or property due to the new capital gains measures?” They could answer “Yes” or “No.” The third question was “What kind of impact do you think the capital gains tax changes will have on the Canadian business landscape?” with the options to answer “Positive,” “Somewhat positive,” “No effect/neutral,” “Somewhat negative” or “Negative.”

Readers were then asked two open-ended questions and invited to provide written answers. The questions were: “If you’re an entrepreneur or have aspirations to build a business, have the changes to capital gains taxes affected your plans?” and “Is your organization making notable changes due to the new capital gains tax rules, such as altering executive compensation (e.g. stock options) or planned investments? If so, what is changing?”

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: Toronto Star via Getty/Dick Loek

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Exclusive

What the Maple 8’s first chief AI officer is up to

Briefing

Canada unlikely to double non-U.S. exports by 2035 without big investments: Report

Trucking giant TFI to start using driverless big rigs in the U.S.

U.S. fintech Ramp opens Toronto office, expands Canadian offerings

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.