The C.D. Howe Institute keeps a team of recession watchers ready to spot economic downturns. That group assembled this week and determined that the second-quarter drop in economic growth was “significant,” but not enough on its own to justify use of the word. The Business Cycle Council “stands ready to meet if conditions deteriorate,” the Toronto-based think tank said in a press release.

Skip to content

Commentary

Carmichael: Tiff Macklem is trying to wake Canada up

The Bank of Canada governor knows talk won’t be enough to shake the country out of its economic stupor

Tiff Macklem, governor of the Bank of Canada, at the Bonaventure Hotel in Montreal in February, 2024. Photo: Nasuna Stuart-Ulin for The Logic

The C.D. Howe Institute keeps a team of recession watchers ready to spot economic downturns. That group assembled this week and determined that the second-quarter drop in economic growth was “significant,” but not enough on its own to justify use of the word. The Business Cycle Council “stands ready to meet if conditions deteriorate,” the Toronto-based think tank said in a press release.

Conditions might not deteriorate. Canada’s policymakers have become pretty good at forestalling the worst. The problem is, conditions might not improve much either. We’re facing a different kind of crisis, one that will require changes we’ve been unwilling to make for a long time.

I’ve typed the word “crisis” pretty much weekly since 2008. Yet in Canada, the Great Recession was just a recession, lasting the equivalent of a couple of quarters thanks to a powerful combination of monetary and fiscal stimulus. The COVID-19 pandemic triggered an epic economic collapse, but one that lasted only a few months. Compare that to the early 1980s, when the recession that central banks incited to crush inflation went on for more than a year.

Related Articles

As dangerous as the Great Recession and the pandemic were, the battle plans were relatively straightforward. You reverse a crisis of confidence in the banking system by flooding the system with money and promising to keep banks from collapsing. You offset a collapse in demand by making money so cheap that borrowing becomes irresistible, and by replacing private spending with public stimulus. The Great Depression informed the response to the Great Recession, although it took some time for policymakers to read up on those lessons. The COVID-19 recession was short because the Great Recession playbook was still fresh.

It helped that those crises were the sort for which central banks were created. Bank of Canada governor Tiff Macklem uses almost every public appearance these days to stress that he can’t do much about what Canada is facing now.

Inflation is contained, but too hot to cut interest rates to zero even if the central bank thought that was wise. The bigger issue is that a massive structural shock from tariffs, and the costs associated with adjusting to tariffs, is beyond the power of monetary policy to fix. CERB-style checks, tax holidays and arena-and-gazebo infrastructure programs won’t help either. Stoking demand would only exacerbate the inflation risk.

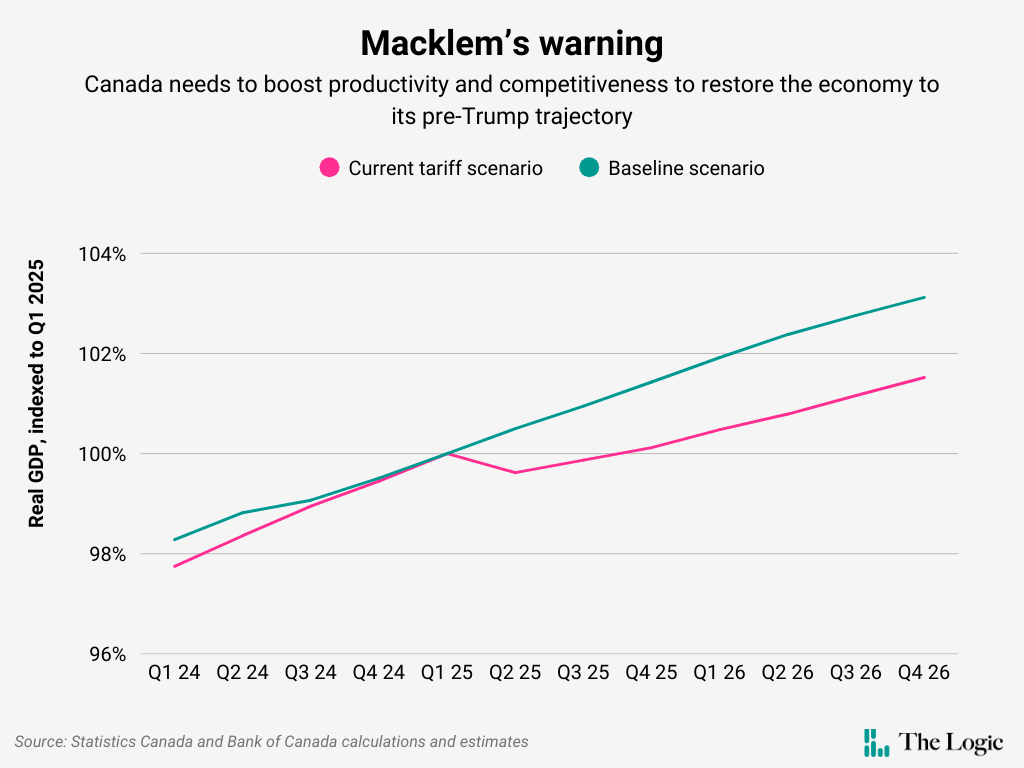

The only way out of the hole the Trump shock has created is to climb. In a speech Monday, Macklem re-upped a version of the chart I wrote about earlier this month. Two lines are headed in roughly the same direction. Then in early 2025, one plunges. That line shows Canada’s new economic trajectory and it stays permanently below the other one, showing Canada’s path pre-Trump.

“Canada has a choice,” Macklem told an audience in Saskatoon. “We can live with the structural impact of a more protectionist United States—the lower path.” Or, he said, “we can improve our productivity and competitiveness” and bend our trajectory “back up to, or even above” what it was pre-Trump.

According to C.D. Howe’s Business Cycle Council, the worst recession Canada has suffered since the Great Depression was a 26-month downturn between the springs of 1990 and 1992. The early 1990s are analogous to what we’re going through now in that it was another period of extreme disruption—the beginning of what now is ending. Manufacturing employment declined by 340,000 positions, or 16 per cent, between December 1988 and December 1993. Canada was adjusting to its new free-trade agreement with the U.S., and China had just begun its ascent as a manufacturing powerhouse. The Berlin Wall fell in 1989 and the Soviet Union disbanded in 1991. The tailwinds from globalization would eventually send Canada on a pretty good run, but it was rough at first.

Macklem’s ability to cut interest rates might be constrained, but he still has a bully pulpit. His Saskatoon speech was a lecture from the country’s unofficial chief economist on how a handful of “megatrends” have changed the world. Some of them have their roots in the 1990s.

As tariffs fell in the era of globalization, trade grew faster than the global economy. Real life mirrored the world described in economics textbooks. Import competition replaced competition between great powers. Stuff got cheaper, incomes rose and global poverty fell. But it was too much change, too fast. For the last decade, trade growth has stagnated under the growing weight of duties, sanctions and other politically motivated friction. “Workers who lost their jobs lost more than they gained,” Macklem said. “This has eroded public and political support for globalization, resulting in a pullback from open trade.”

That’s hindsight analysis. Democratic capitalism was triumphant in the early 1990s and no one was talking about autocracy making a comeback. Maybe that euphoria made those of us who were there a little stupid. We got excited about growth rates, trade surpluses and balanced budgets without paying enough attention to what was going on underneath. There was always talk of being more deliberate about helping communities adjust, but I don’t know that anyone took it especially seriously. There was a deep conviction that free trade would make everyone richer. Canada did a better job of distributing that wealth than many. The mistake was assuming we could rely on others to underwrite our quality of life indefinitely.

If lessons from the Great Depression and the 1980s helped fight some of our more recent crises, what do the early 1990s tell us about what we should do now? One thing: recognize that adjusting to shocks of this magnitude can take a long time. Another might be to avoid ideological blindness and prosecute every assumption about how things are supposed to work. A third, surely, is to avoid letting ourselves again be so exposed to events beyond our control.

Macklem reminded his audience this week that it’s easy to talk about doing hard things in the aftermath of a crisis. “The recession in 2009 highlighted how vulnerable we are to a drop in U.S. demand, and everyone talked about diversification then, too,” he said. “But not much happened. This time we need to follow through.”

On trade diversification, and on so much more. We know what to do. The faster we do it, the easier this will be. But make no mistake—nothing about it will be easy. Adjustment is always varying degrees of hard.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: Nasuna Stuart-Ulin for The Logic

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Analysis

These AI startups are making millions with tiny teams

Briefing

Supply-chain management vendor Kinaxis reports revenue jump and higher profit

Flush with cash, Suncor Energy boosts share buybacks—but doesn’t rule out production growth

Goodfood seeks creditor protection as it tries to sell itself

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.