One of the research papers that Finance Minister Chrystia Freeland said convinced her that higher capital gains taxes wouldn’t kill entrepreneurship was co-written by Lawrence Summers, the Harvard economist who served as Bill Clinton’s treasury secretary and led Barack Obama’s national economic council. The paper included this line:

Skip to content

Facebook founder Mark Zuckerberg in his Harvard days, before he had to worry about capital gains taxes. Photo: Tumblr

Facebook founder Mark Zuckerberg in his Harvard days, before he had to worry about capital gains taxes. Photo: Tumblr

Commentary

Carmichael: Whatever became of the Canadian entrepreneur?

There’s an obvious scapegoat for Canada’s lack of enterprise, but the truth is more complicated

Shopify CEO Tobi Lütke in June 2021. Photo: Screenshot

One of the research papers that Finance Minister Chrystia Freeland said convinced her that higher capital gains taxes wouldn’t kill entrepreneurship was co-written by Lawrence Summers, the Harvard economist who served as Bill Clinton’s treasury secretary and led Barack Obama’s national economic council. The paper included this line:

… it is hard to imagine entrepreneurs making decisions about investment and risk on the basis of the capital gains tax regime: Mark Zuckerberg was not focusing on the capital gains tax when he was in his dorm room coding up Facebook.

I think the macroeconomists, policymakers and politicians who have never started a company should be careful about presuming they understand the motivations of those who have.

The Summers line implies Zuckerberg would have created his company no matter what. Maybe so. But surely context matters. By 2004, Zuckerberg was so sure he was about to make it big that he showed up for a pitch meeting at Sequoia, one of Silicon Valley’s preeminent venture firms, in pajama bottoms and a t-shirt.

Google had just gone public, proving that youth and antisocial behaviour needn’t get in the way of a massive payday. The power law had taken over venture finance. If Zuckerberg wasn’t thinking about capital gains taxes, it might have been because capital came easy at the start of the millennium.

Put Zuckerberg in another place, or another time, and maybe TheFacebook never becomes Facebook and Facebook never becomes Meta. That’s why another of Freeland’s rationalizations for raising the capital gains taxes—that the inclusion rate was higher in the 1990s—doesn’t stand up. Too much has changed since then to assume that raising the cost of capital will have no effect on entrepreneurship today. The GST was higher in the 1990s, too. Why not raise that tax, as the IMF staffers who grade Canada’s economic performance suggest in their annual report card?

Governments need to think carefully about how their policies could affect entrepreneurship because the data suggest Canada is losing its verve for creating new companies. BDC observed last year in a report that the “entrepreneurial spirit burns bright,” as 14 per cent of Canadians say they’d like to start a business. Yet only 1.3 out of every 1,000 Canadians actually started a company in 2022, the report said.

Tobias Lütke, the co-founder and CEO of Shopify, is among those who have expressed concern over the steep drop in self-employment amid a corresponding surge in public sector employment since the end of the pandemic. “We need to reverse this, Canada,” he tweeted in June. “Ideally all of it.”

Related Articles

Lütke’s tweet contained a chart from The Globe and Mail that used Statistics Canada data to calculate the growth rate of public, private and self-employment since 2014. The graphic creates the impression that the government is in the process of swallowing the labour market whole.

Growth rates don’t always provide the full picture. Those lines could be marking a correction of some kind; maybe public sector employment was on a downward trend and is now catching up with growing demand for government services from an aging society.

It’s better to put numbers in their proper context. Public sector employment represented about 21.6 per cent of total employment in June, compared with an average of 20.7 per cent since 1976, the starting point for data from Statistics Canada’s labour force survey.

Private sector employment accounted for 65.5 per cent of all employment, compared with a historical average of 64.6 per cent. Employers such as Shopify are absorbing as many potential entrepreneurs as governments, explaining why average wages have increased some 16 per cent since the end of 2019.

There’s a war for talent. Why take the risk of starting a company when you can make around $60 per hour in the oilpatch or close to $40 per hour as a software engineer, according to Statistics Canada’s monthly payroll survey. Self employment now accounts for 12.9 per cent of the total population of employed workers, compared with an average since 1976 of 14.7 per cent.

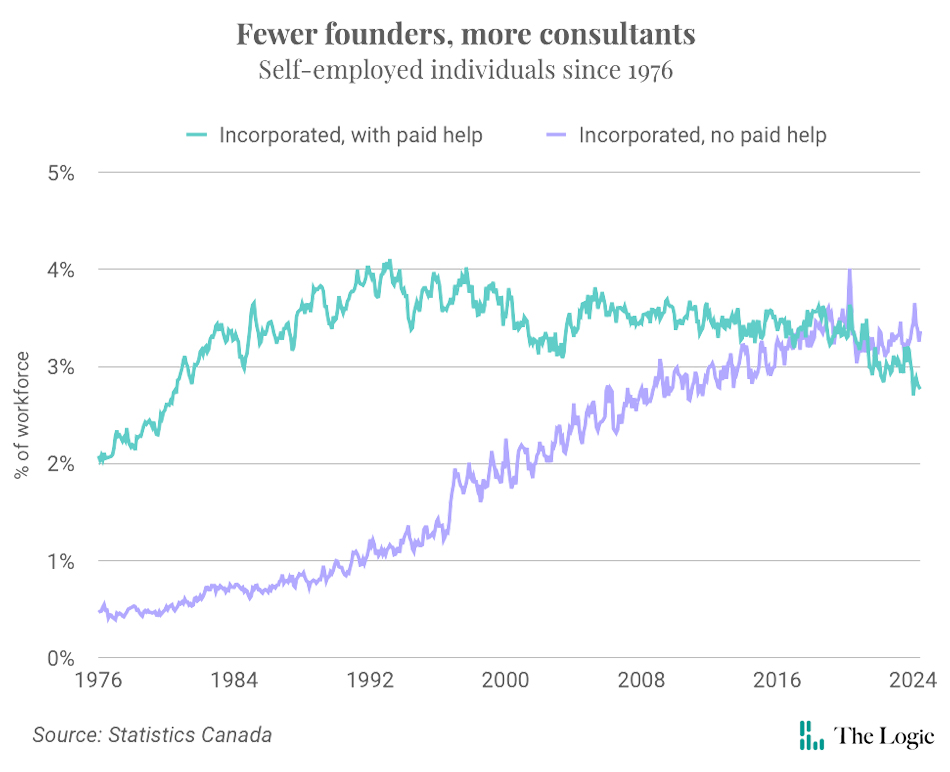

But even that number obscures the extent to which Canada’s entrepreneurial drive has diminished in recent years. There are four kinds of self-employed people, per Statistics Canada: incorporated self-employed who hire people; incorporated self-employed who hire no one; unincorporated self-employed people who take on staff; and unincorporated freelancers and consultants who work alone.

An entrepreneur who incorporates and then hires people is probably a good proxy for someone who will move the needle, while an incorporated individual who doesn’t hire anyone is probably an accountant, lawyer or freelancer seeking to maximize their tax advantages.

The former now represent about 2.8 per cent of all employment, the lowest since the early 1980s. The latter group now accounts for 3.4 per cent of the employment, compared to an historical average of 1.9 per cent, a reminder that simplistic small business tallies aren’t a good proxy for entrepreneurship.

What’s going on? In this highly polarized environment, some will want to blame Prime Minister Justin Trudeau and the capital gains tax. Policies of that sort send a bad signal, but the explanation is more complex than that.

The most important factor could be an aging society, a trend that Canada was trying to reverse with record levels of immigration until rapid population growth ran up against our capacity to provide shelter and basic services. That 2023 BDC report said most companies are started by people in their late 20s to early 40s—a demographic that’s shrinking, while the number of people 55 and older is growing.

Freeland partially offset the higher inclusion on capital gains by lowering the inclusion rate for entrepreneurs, although up to a maximum of $2 million over a decade. It’s the right idea, but is it enough? The forces smothering entrepreneurship won’t be reversed by fiddling with the tax code.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: Screenshot

Facebook founder Mark Zuckerberg in his Harvard days, before he had to worry about capital gains taxes.

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

News

Alberta wants to be a model for government AI and power Canada-wide adoption

Briefing

Constellation Software’s Harris acquires TouchBistro

Aritzia doubles its first quarter profits on strong sales

Carney confirms Saudi Arabia’s Public Investment Fund to attend his investment summit

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.