Tiff Macklem spent the first part of his career preparing the ground for inflation targeting. He probably will spend the rest of his time as governor of the Bank of Canada trying to restore confidence in a policy he helped create.

Skip to content

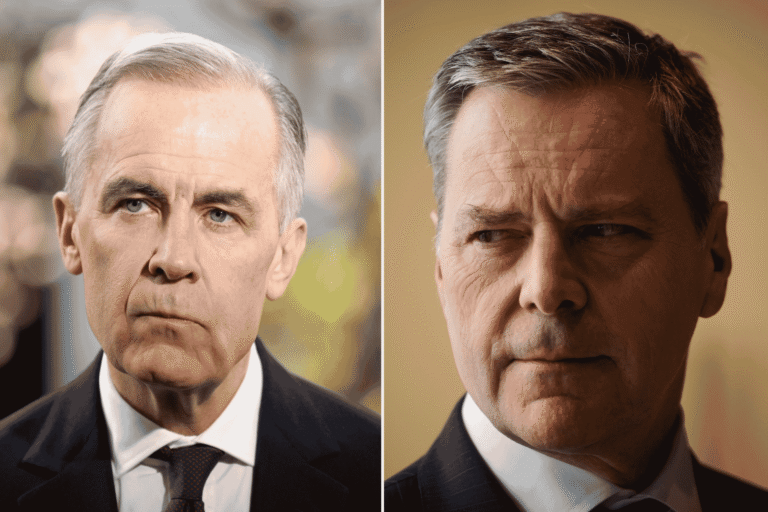

Bank of Canada governor Tiff Macklem in an interview with The Logic’s Kevin Carmichael in Montreal last month. Photo: Nasuna Stuart-Ulin for The Logic

Bank of Canada governor Tiff Macklem in an interview with The Logic’s Kevin Carmichael in Montreal last month. Photo: Nasuna Stuart-Ulin for The Logic

Commentary

Carmichael: Like interest, doubt compounds over time. For the Bank of Canada, that’s a problem

Tiff Macklem may spend the rest of his tenure trying to restore confidence in a policy that he helped create decades ago

Bank of Canada governor Tiff Macklem at the Bonaventure Hotel in Montreal in February 2024. Photo: Nasuna Stuart-Ulin for The Logic

Tiff Macklem spent the first part of his career preparing the ground for inflation targeting. He probably will spend the rest of his time as governor of the Bank of Canada trying to restore confidence in a policy he helped create.

As an up-and-comer at the central bank in the 1980s, Macklem contributed to the research that would make Canada the second country, after New Zealand, to bet that inflation could be tamed by using consumer prices to guide the interest-rate setting. The policy change would coincide with a few decades of relative price stability, causing central bankers to think they had finally cracked the code. Inflation targeting is now the go-to method for setting interest rates in every major economy.

But just as a period of high inflation and societal unrest gave economists reason to seek better ways to conduct monetary policy in the early 1980s, current conditions demand a thorough analysis of what works and what doesn’t.

There are questions about the extent to which quantitative easing—when central banks use their unique powers to create government-sanctioned money, and lower interest rates by purchasing financial assets—contributed to the post-pandemic surge in inflation.

Related Articles

Those questions might be easier to dismiss if the country’s most popular political party weren’t the ones raising them.

“There were a number of people [in the] early months after [COVID-19] that said, ‘Look, if you increase the M2 money supply like you’re purporting to do, it will lead to inflation,’” Conservative MP Adam Chambers said at a Canadian Club event in Toronto last month. “Pierre [Poilievre] was the only Canadian politician talking about it, and one of the very few Canadian economists or those who follow the markets that were on this issue early. That’s given him significant credibility as leader of the party to talk about, ‘OK, now how do you deal with inflation?’”

Some economists wonder whether the inflation target is too low, thus forcing central banks to leave interest rates too high. The groundswell of support for a higher target grew so strong that the Bank of Canada grudgingly decided it had little choice but to study the idea as part of its next mandate review. “We need to have an open mind, but I have to say, I’m not convinced,” Macklem said in an interview with The Logic last month.

Like interest, doubt compounds over time. That’s a problem for the Bank of Canada because credibility is a key component of monetary policy: it’s harder to keep a lid on inflation when the public doubts the authorities are up to the task. Yet the critiques keep coming. The latest is the argument that the central bank has been relying on faulty gauges.

Economists at TD, CIBC and Desjardins have all published reports in recent weeks that pick apart the Bank of Canada’s preferred measures of “core” inflation, which shrink the hundreds of items that constitute the consumer price index to 55 components: CPI-trim, which removes 20 per cent of the most inflationary items and 20 per cent of the least inflationary items each month; and CPI-median, which measures the price change at the 50th percentile of the distribution of all changes in a given month.

The Desjardins report—co-authored by Royce Mendes, a former Bank of Canada researcher—drew praise on LinkedIn from Sen. Clément Gignac, a former chief economist at National Bank, suggesting the analysis has reached at least the outer circles of policymaking in Ottawa.

Mendes, head of macro strategy at Desjardins, and Tiago Figueiredo, a macro strategist, argue that the Bank of Canada’s fancy measures of inflation might work well in normal times, but have been thrown off by all the volatility stirred up by the COVID-19 pandemic and its aftermath.

For example, CPI-trim might be underestimating the extent to which inflation is slowing because it automatically disregards a fixed amount of inflationary and deflationary outliers. Because the current distribution is skewed towards a group of items that continue to experience price pressure, CPI-trim is “biased” towards a higher number, failing to account for a fat tail of costs that suggest inflation no longer is a threat.

Mendes and Figueiredo said the average of “unbiased” CP-trim and CPI-median measures would have shown three per cent inflation in January, materially lower than the 3.4 per cent average of the official readings that month. “If the Bank of Canada ignores our findings, officials risk leaving monetary policy restrictive for too long, inflicting unnecessary pain on households and businesses,” Mendes and Figueiredo wrote, arguing the bank should cut interest rates as soon as June.

We’ll see if the Desjardins research penetrates deeper than senators who are active on LinkedIn, but the Bank of Canada knows its core measures are unreliable. In that February interview, Macklem also said the central bank’s next mandate review would include a reassessment of how it predicts where inflation is headed. The comment seemed too wonky to bother reporting at the time, but given the sudden level of interest on Bay Street, maybe that was a mistake.

“I think we do need to do a review of how we measure underlying inflation, core inflation, and make sure we’ve got the best available measures, particularly in a world where we could have more volatility,” Macklem said. “Getting the best available measures of underlying inflation, core inflation, is going to be, I think, important going forward.”

In the meantime, it looks like the Bank of Canada is adjusting on the fly. The summary of deliberations that led to the decision to leave its interest rate unchanged on March 6 revealed that policymakers had a “detailed” discussion over inflation indicators, agreeing that “underlying inflation is not measured by a single statistic but rather by a collection of indicators.”

Macklem doesn’t need Bay Street to tell him he’s got some work to do. He knows.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: Nasuna Stuart-Ulin for The Logic

Bank of Canada governor Tiff Macklem in an interview with The Logic’s Kevin Carmichael in Montreal last month.

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Commentary

Carmichael: Tiff Macklem can’t save you

Briefing

Canada to publish list of imports at risk of being made with forced labour

TMX Group acquires RAFI Indices for $683M

Ikea invests in Toronto food startup NS/TX Industries’ US$10.5M fundraise

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.