The gap between money entering Canada and leaving to invest and buy stuff elsewhere widened to a record $21.2 billion in the second quarter, Statistics Canada reported Thursday. That kind of news is usually bad for the dollar. It shows there’s muted demand for the goods, services and investments we’re trying to sell, and therefore there’s likely muted demand for the currency required to purchase them.

Skip to content

Commentary

Carmichael: There’s upside for Canada in Trump’s attack on the Fed

The U.S. president’s penchant for self-harm offers opportunity for stable democracies—if their leaders don’t waste it

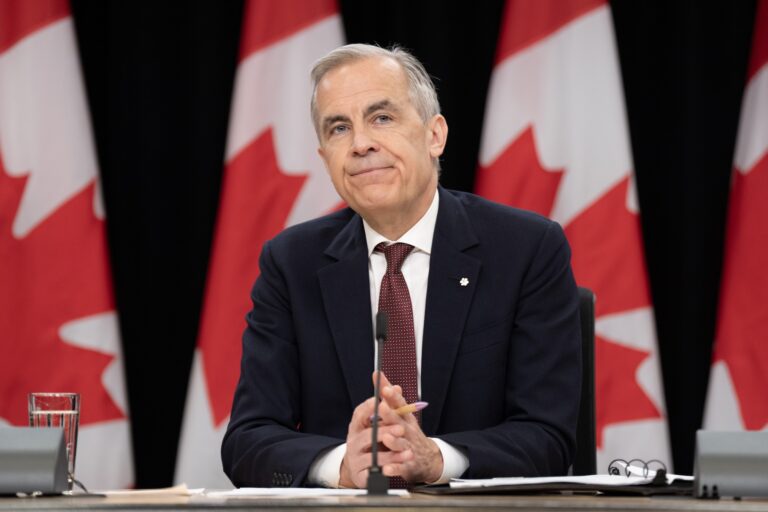

U.S. Federal Reserve chair Jerome Powell swearing in Lisa Cook as a member of the central bank's board in June 2023. Photo: Getty Images/Drew Angerer

The gap between money entering Canada and leaving to invest and buy stuff elsewhere widened to a record $21.2 billion in the second quarter, Statistics Canada reported Thursday. That kind of news is usually bad for the dollar. It shows there’s muted demand for the goods, services and investments we’re trying to sell, and therefore there’s likely muted demand for the currency required to purchase them.

Yet the loonie was trading about a cent higher this week. The reason: U.S. President Donald Trump. He’s a menace to the Canadian economy, but he’s helping a little bit too.

Remember the “sell America” trade? Investors responded to the spectacle of Trump trying to fire a key member of the Federal Reserve by adding to the risk premium they require to lend the U.S. government money for 30 years.

The value of the U.S. dollar fell, which is what helped Canada’s currency. When your preferred haven turns violent, you seek refuge elsewhere. Canada’s economy is under siege, so it’s an imperfect shelter. But its triple-A status for creditworthiness still counts for something, as does the fact that it recently conducted an election that transferred power to a new prime minister without violence or upset. That now counts for something too.

Related Articles

Money needs an anchor. For five decades, the anchor that most liberal democracies have used is an independent central bank. Gold had been the other option, but one of the lessons of the Great Depression was that clinging to a non-fungible asset is an unnecessary—and potentially damaging—constraint on societies’ impulse to grow.

Paper money issued by governments was flexible enough to allow for growth, but history was riddled with destructive inflationary episodes caused by kings abusing monetary policy to get themselves out of debt trouble. It required sifting through countless revolutions, insurrections and financial calamities, but the world’s best financial minds eventually landed on the idea of leaving a central bank alone to regulate the supply of money by adjusting interest rates to meet targets approved by the government. The result was the Great Moderation, a long period of steady growth and minimal inflation.

But as we’ve come to learn, Trump doesn’t do stability. His constant verbal badgering of Fed chair Jerome Powell was bad enough. When the person with appointment power declares his or her unhappiness with the way things are being done, it’s fair to wonder how that might change management’s objectives. Christopher Waller, a Trump appointee at the Fed, said this week that he anticipates rate cuts this fall, and didn’t rule out the need for an outsized half-point cut as soon as next month. Is that assessment based on objective analysis? Or on Waller’s place on Trump’s shortlist to replace Powell? That’s why leaders are encouraged to stay quiet about the day-to-day conduct of monetary policy. It’s become impossible to assess Fed policy without asking what’s behind it.

Still, there was little evidence Trump was getting to Powell. The Fed has left interest rates unchanged, despite the president insisting they should be lower. So Trump went after a weaker target. On Monday, he attempted to fire Lisa Cook, one of Powell’s deputies, on the basis of an accusation that she had committed mortgage fraud. An accusation of wrongdoing is different than having committed a crime, and therefore questionable grounds for automatic dismissal. Cook refused to leave and has taken the Trump administration to court. It’s hard to overstate how much is riding on the outcome. Trump loyalists would fill four of seven seats on the Fed’s Washington-based board of governors, creating a faction on the larger 11-person committee that sets the interest rate.

History is echoing loudly. The French Revolution was financed by an early form of paper money, and the Reign of Terror was then fed by the inflation created by the inability of the revolution’s leaders to stop printing money.

Amid the stagflationary 1970s, former U.S. president Richard Nixon infamously bullied Fed chair Arthur Burns to cut interest rates, making things worse. More recently, Turkey’s autocratic president, Recep Tayyip Erdoğan, fired a succession of central bank leaders to implement his idiosyncratic view that higher interest rates cause inflation, not the other way around. Erdoğan relented after inflation surged to 85 per cent. He appointed an orthodox central bank governor, who raised the benchmark interest rate to 50 per cent to get price increases under control.

The Trump administration’s penchant for self-harm offers an opportunity for stable democracies to create advantages. Canada’s long-term borrowing rate is around 3.9 per cent, a full point lower than comparable U.S. rates.

For Canada, it’s also a teachable moment. We nearly elected a party leader who promised to fire Bank of Canada governor Tiff Macklem for becoming “the ATM machine” of previous prime minister Justin Trudeau’s government. Pierre Poilievre said during the Conservative leadership debate in 2022 that he would find a governor that would “reinstate our low-inflation mandate.”

A leader who was openly toying with a strongman assault on the country’s most important economic institution nearly won the last election. Poilievre wouldn’t have had to fire Macklem to change monetary policy. All he would have needed to do was have his finance minister send Macklem a new directive. The central bank works for the government that commands support in Parliament, not the other way around.

It didn’t take a new governor to get inflation under control. It took patience, and faith that an approach developed over centuries of trial and error still works as intended. Canada’s brush with Trump- and Erdoğan-style monetary policy is something to keep in mind. Stability is an advantage right now, but we’re more than capable of wasting it.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.

Loading...

Thanks for sharing!

You have shared 5 articles this month and reached the maximum amount of shares available.

CloseThis account has reached its share limit.

If you would like to purchase a sharing license please contact The Logic support at [email protected].

CloseGift the full article!

You have gifted 0 article(s) this month and have 5 remaining.

Recipients will be able to read the full text of the article after submitting their email address. They will not have access to other articles or subscriber benefits.

Photo: Getty Images/Drew Angerer

Most Popular This Week

In-depth, agenda-setting reporting

Great journalism delivered straight to your inbox.

Commentary

Carmichael: The rise of AI-powered solopreneurs could upend how the economy works

Briefing

Celestica completes US$3.45B share sale to meet demand for data-centre equipment

Sun Life pitches itself on Wall Street as an alternative to Blackstone, Apollo

MDA revenue jumps 34% in Q2, raises full-year outlook

Best business newsletter in Canada

Get up to speed in minutes with insights and analysis on the most important stories of the day, every weekday.

Exclusive events

See the bigger picture with reporters and industry experts in subscriber-exclusive events.

Membership in The Logic Council

Membership provides access to our popular Slack channel, participation in subscriber surveys and invitations to exclusive events with our journalists and special guests.