Listen Now

0:00

The best example of Canada’s fixed mindset is the conversation about trade. Everyone agrees that reducing our dependence on the U.S. market is a good idea, but you’ll struggle to find someone who thinks it’s possible. “Much like during the Cold War, countries such as Canada will ultimately be compelled to align with one of the major powers,” CIBC economists Benjamin Tal and Katherine Judge wrote in a recent report. “Despite recent developments, it is clear that Canada’s alignment will remain with the United States.”

I don’t know. Finland found itself trapped in the Soviet Union’s orbit after the Second World War and still found a way to resist the economic gravity of the behemoth next door. The trick is making yourself good at producing what the world wants, rather than being a purveyor of what the world needs. The former tends to fetch a premium, while the latter tends to be commoditized and vulnerable to tariffs. So a successful diversification strategy will require moving beyond commodities. That doesn’t sound so hard. In fact, it’s already happening.

Related Articles

Meet Thomas Fox, co-founder and CEO of Calgary-based Highwoods Emissions Management and the embodiment of a modern trader. “Our ambition, honestly, is global domination,” Fox said. “We want to work with every oil and gas company. We’re building a scalable platform that should be a no-brainer because we’ve taken a process that used to take 10 people six months that now takes a couple of days to do with way more rigour.”

I interviewed Fox in March at CERAWeek, S&P Global’s annual global energy conference in Houston. His confidence stood out among a Canadian delegation that was otherwise short on ambition. The oilsands producers who appeared on stage were obsessed with protecting their profit margins, while the pipeline companies complained about regulation. They showed little desire to seize the moment.

A venture-backed startup like Highwood has different incentives than mature companies like Cenovus and TC Energy, but Fox was dealing with his own headwinds. Highwood’s specialty is helping oil and gas companies get a handle on their methane emissions. When the firm raised US$3 million in 2023, “methane was pretty hot,” Fox said. But at CERAWeek, the only time climate entered the chat was when someone would observe how little attention climate change was getting. The priorities were energy security, data centres and artificial intelligence. “We’re having to reframe the value proposition,” he said.

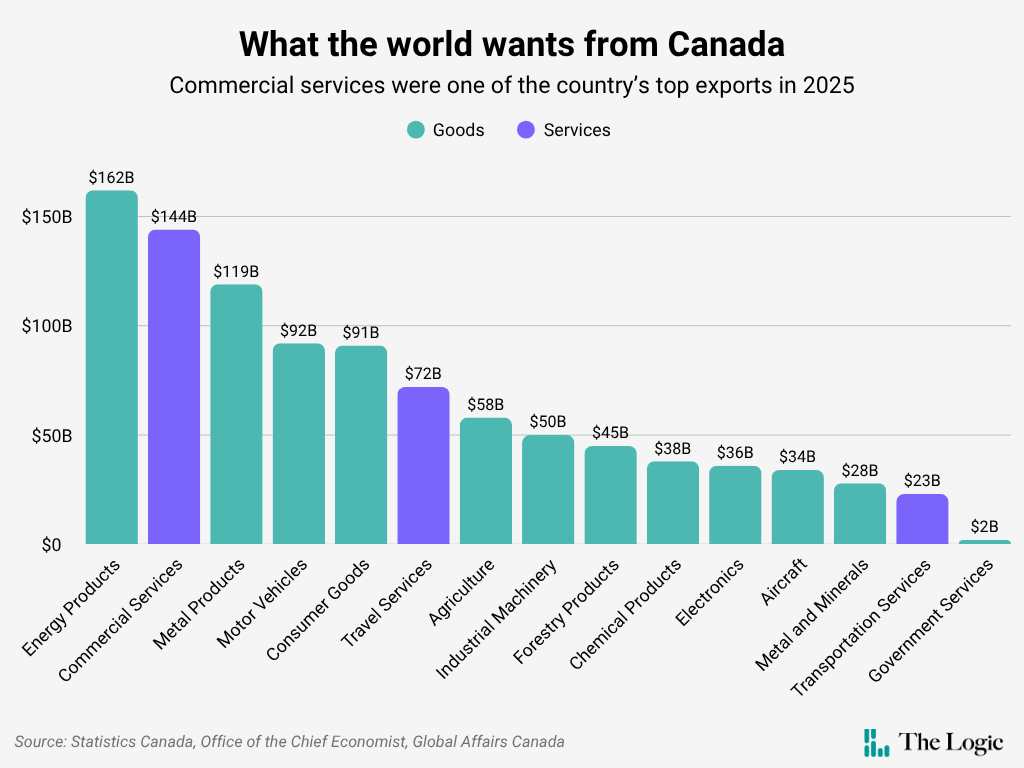

I think Canada has to reframe its value proposition when it comes to trade. We’ve been immersed in the digital economy for at least a decade, and service providers account for 75 per cent of the country’s gross domestic product. The $50-billion increase in export revenue between 2022 and 2025 was entirely the result of services, according to Global Affairs Canada’s latest State of Trade report, published this week by the department’s Office of the Chief Economist.

Yet almost everything you read about trade is based on goods. That’s because it’s easier to imagine stuff that we can touch, taste and feel. It’s also much easier to measure such things. Our biases skew the narrative, creating the impression that the national economy is heavily dependent on selling automobiles to the U.S. (for example), rather than just moderately so.

The downbeat assessment of trade diversification by CIBC’s Tal and Judge was based entirely on merchandise exports. They observe that 15 separate trade agreements have done nothing to offset the gravitational pull of the U.S. market. It was probably always naive to think that they would. Tangible exports are heavy, so shipping costs will always be a determining factor in where such things are sold. Canada’s goods exports are tied to the U.S. because we didn’t develop enough manufacturers that make things the world wants to buy, whatever the cost. Canada has a trade deficit with South Korea because we have no Samsungs, Hyundais and SK Hynixs.

But in a digital economy, you don’t need to make popular smartphones, quality cars and memory chips. According to the State of Trade report, Canada’s exported commercial services, such as those provided by Highwood, were worth $144 billion in 2025. That’s second only to the $162 billion the world (mostly the U.S.) paid for Canadian energy products. Travel services were more valuable than agriculture exports; lots of countries sell wheat, but there is only one where you can visit Banff National Park, eat at a Montreal restaurant or stay at the Fogo Island Inn. In all, services now account for about a quarter of Canada’s exports, which suggests it’s past time to update how we talk and think about trade.

The weightlessness of intangibles also lets them defy economic gravity. Distance and familiarity matters, which is why the U.S. remains the biggest market for Canadian services—but only accounts for about 53 per cent of the value. You know what that means. A country determined to make itself less reliant on trade with the menacing behemoth next door will lean into the things that the rest of the world wants from it. “The services sector has quietly become a critical driver of Canadian business expansion abroad,” the State of Trade report observes, “encompassing digital innovation, professional expertise, intellectual property, tourism and other intangible activity.”

A narrative shift will mean moving beyond the origins of automobile parts and the U.S. administration’s opinion of supply management. In Houston, the rule-setting body that most mattered to Fox was the International Organization for Standards, because whatever it decides on measuring methane emissions will matter more to Highwood than the North American trade agreement.

It will also mean focusing on people rather than things. Export competitiveness will be determined by education, immigration and creating communities in which talented people want to live. Again, that shouldn’t be hard. An emphasis on services means good trade policy and good domestic policy are the same.

Kevin Carmichael is The Logic’s economics columnist and editor-at-large. He has spent more than two decades covering economics, business and finance for outlets including Bloomberg News, The Globe and Mail and the Financial Post, where he also served as editor-in-chief.